Owner income$71k to $5.1M

Owner income$71k to $5.1MHow Much Project Management Business Owners Make: $150K Salary Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$71k to $5.1M  Net margin-18% to 63%

Net margin-18% to 63% Revenue for target pay$434k

Revenue for target pay$434k Business difficultyHard

Business difficultyHard

You’re pricing owner pay before the firm has steady utilization, so the key number is not employee salary data This five-year model shows $150,000 in annual founder salary, EBITDA moving from -$79,000 in Year 1 to $4907 million in Year 5, and excludes personal taxes, payroll tax treatment, debt service, and guaranteed distributions

Owner income$71k to $5.1MNet margin-18% to 63%Revenue for target pay$434kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full Project Management forecast?

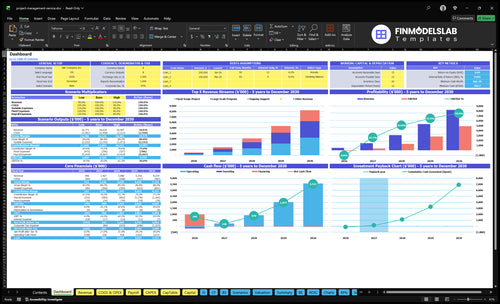

This dashboard shows revenue, gross margin, EBITDA, cash, payback, and owner income, with assumptions tabs for pricing, hours, client mix, and costs. Open the Project Management Financial Model Template.

Key model highlights

- Month 9 breakeven

- $785k minimum cash

- 22-month payback

- EBITDA from -$79k to $4.907M

- Early, growth, mature cases

How does scaling a project management business affect owner income?

At the start, owner-as-project-manager protects margin, but income caps at personal billable capacity. As owner-as-salesperson, the pipeline can grow faster, but delivery risk rises if hiring lags. In this Project Management model, breakeven lands in Month 9, minimum cash needed is $785k in Month 9, and payback takes 22 months; the first project manager starts in Month 13 and the junior project manager in Month 25.

Owner income path

- PM first protects early margin.

- Billable hours cap income fast.

- Sales first grows pipeline faster.

- Quality risk rises if hiring lags.

Scale and cash timing

- Breakeven hits in Month 9.

- $785k minimum cash is needed.

- First PM starts in Month 13.

- Junior PM starts in Month 25.

How much revenue does a project management business need to pay the owner?

A Project Management business needs about $544k/year, or $45k/month, to pay a $150k Year 1 owner salary; see How Is The Overall Success Of Your Project Management Service Measured? for the operating KPIs behind that target. At a 72% contribution margin, the same model needs about $475k/year for a $100k owner salary.

Revenue target

- $137.5k non-founder payroll

- $79.2k fixed expenses

- $25k marketing spend

- $150k owner pay

Quick math

- $391.7k costs before margin

- $391.7k / 72% = $544k

- Modeled revenue is $434k

- EBITDA shows -$79k

What affects profit margin in a project management business?

Project Management margins are driven by delivery COGS, then by sales, tools, payroll, marketing, and fixed overhead; gross margin is after delivery COGS, while operating margin is after the full cost stack. In Year 1, gross margin is 83%, contribution after COGS and variable costs is 72%, and EBITDA margin is about -18%; by Year 5, those improve to 88%, 79%, and about 63%. If you’re sizing launch spend, start with How Much Does It Cost To Open, Start, Launch Your Project Management Business? because every 1-point cost change moves profit by about $43k at Year 1 revenue and $78k at Year 5 revenue.

Year 1 drivers

- 83% gross margin after delivery COGS

- 72% contribution after variable costs

- -18% EBITDA margin

- $43k impact per 1-point cost change

Year 5 drivers

- 88% gross margin after delivery COGS

- 79% contribution after variable costs

- 63% EBITDA margin

- $78k impact per 1-point cost change

Want the six main income drivers?

1

$120-$165/hrContract Value

Higher rates and larger scopes lift revenue fast because every hour sold is worth more.

2

15-100 hrsBillable Utilization

More billable hours per client and per manager spread payroll across more revenue, so take-home rises.

3

1-4 FTELabor Mix

A leaner mix of senior and junior project staff keeps delivery cost down as work scales.

4

83%-88%Gross Margin

Tighter scope control protects gross margin and keeps unplanned work from eating profit.

5

60%-75%Client Retention

More ongoing support work steadies cash flow and cuts the cost of chasing new clients.

6

$792KOverhead Control

Keeping fixed overhead near this level protects EBITDA and reduces the cash needed to stay open.

Project Management Core Six Income Drivers

Client Contract Value And Pricing Model

Contract Value

Your income here depends on contract size and pricing quality, not just booked sales. In Year 1, the modeled deals are $1,800 for 15 support hours at $120, $5,200 for 40 fixed-scope hours at $130, and $12,000 for 80 program hours at $150. Weak pricing fills the calendar but leaves owner pay thin.

Price for Scope

Track contract type, hours sold, scope changes, and cash collected up front. Hourly work protects scope, retainers help cash flow, and fixed fees need change-order rules before work starts. If a 40-hour fixed-fee job turns into 50 hours, that’s a 25% overrun that cuts take-home unless the extra work is billed.

- 15 support hours: $1,800

- 40 fixed-scope hours: $5,200

- 80 program hours: $12,000

- Track approved change orders

1

Billable Utilization

Billable Utilization

Billable utilization is the share of available time spent on paid client work. For this project management business, it drives owner pay because the same team can look busy while admin, sales, reporting, and internal coordination still eat margin. The key split is owner hours versus employee and subcontractor hours, since each one hits profit differently.

Here’s the quick math: if capacity only reaches 15 support hours early on and scales to 100 large-program hours by Year 5, small misses in utilization compound fast through payroll, commissions, and fixed overhead. That cuts cash available for owner draw even when revenue is growing.

Track Billable Hours First

Measure billable hours / available hours every week, then split it by owner, employee, and subcontractor. Also track nonbillable time in sales, reporting, and internal coordination, because that is the hidden drag on take-home income. One clean rule: if it is not tied to a paid client task, it should be visible in the forecast.

Use a simple capacity plan with these inputs: available hours, paid hours, staff mix, payroll, commission costs, and fixed overhead. If utilization slips, protect margin by cutting nonbillable meetings first, then rebalancing work between owner-led delivery and lower-cost support. Busy calendars do not pay the owner unless enough of those hours are billable.

- Billable hours by role

- Nonbillable hours by category

- Payroll tied to capacity

- Overhead covered by billed work

- Owner hours versus team hours

2

Delivery Labor Mix

Delivery Labor Mix

This driver is the split between owner-delivered work, employees, and subcontractors. It affects margin fast: owner delivery usually keeps more gross profit early, employees add capacity, and subcontractors add flexibility but usually lift labor cost. In the model, project manager contract fees fall from 14% of revenue in Year 1 to 10% in Year 5, so the mix gets more efficient only if payroll and contractor hours stay tied to booked work.

The cash risk is timing. Staffed payroll rises from $2,875k in Year 1 to $105M in Year 5, so hiring before revenue lands can crush owner pay. But cutting labor too far creates missed deadlines, weak quality checks, and slow client communication, which can hurt renewals and force the owner back into firefighting.

Staff to Revenue, Not Hope

Track three inputs every month: owner billable hours, employee utilization, and subcontractor share of delivery. Here’s the quick math: if labor is the main variable cost, every extra point of contractor mix can pull gross margin down unless pricing covers it. Keep fixed-scope and retainer work on staff, and use subcontractors for spikes, niche skills, or overflow only.

Set a hiring trigger from booked work, not pipeline stories. If the team is thin, you’ll miss deadlines and client updates; if it’s too fat, owner draw gets squeezed. A simple rule: add payroll only when signed work can support it for the next cycle, and review contractor spend against the 14% to 10% fee path so margin doesn’t drift.

3

Gross Margin And Scope Control

Gross Margin And Scope Control

Gross margin is the share left after direct delivery costs. Here it moves from 83% to 88% when contract fees and project-specific software shrink as a share of revenue. On $100,000 of revenue, that 5-point gain adds $5,000 to gross profit, which is the money that can pay overhead and the owner draw.

Scope creep cuts that margin fast. Unpaid meetings, vague status reports, and loose change requests push direct costs up, so fixed-fee work needs clear included hours, approval gates, and priced change orders. The owner keeps more take-home income when every extra meeting has a budget owner, a scope reason, and a billing path.

Track Scope Before It Eats Margin

Measure included hours, extra meetings, change requests, contract fees, and project-specific software costs on every job. Compare planned hours to actual hours each week, then flag any project that starts to drift before the margin loss shows up in cash flow.

- 83% to 88% gross margin target

- Unpaid meetings by client

- Approved change orders and fees

- Software costs per project

Price the first scope tightly, then bill for anything outside it. If a meeting has no budget owner, no scope reason, and no billing path, it should not happen for free. That rule protects gross profit, and it protects the owner’s pay.

4

Client Retention And Pipeline Stability

Client Retention And Pipeline Stability

Recurring support keeps the bench full and the owner’s pay steadier. In this model, ongoing project management allocation rises from 60% in Year 1 to 75% in Year 5, so fewer hours depend on new sales every month. That lowers churn risk, smooths cash flow, and makes payroll coverage easier when demand shifts.

Here’s the tradeoff: marketing spend climbs from $25k to $150k, while CAC improves from $1,500 to $1,000. Retained clients help margins, but concentration risk grows if one large program fills too much capacity. One client can look great and still pressure the owner’s draw if it crowds out pipeline.

Keep Retention From Hiding Risk

Track retained revenue, pipeline coverage, and the share of capacity tied to the largest client. The useful inputs are recurring support hours, active client count, close rate, CAC, a nd how much staff time sits on one account. If retention rises but pipeline weakens, payroll gets exposed fast.

- Watch recurring hours by client

- Cap one-client capacity share

- Review pipeline monthly

- Measure CAC by channel

- Forecast payroll coverage weekly

Push renewals before expiry, price support for steady delivery, and keep backup leads in motion. If one program starts soaking up most staff time, slow new commitments until the next quarter’s coverage is secure. That protects cash flow and keeps owner income from swinging with one account.

5

Overhead And Operating Discipline

Fixed Overhead Control

Fixed overhead sits at $6,600 per month, or $79,200 per year, before payroll and marketing. That covers rent, insurance, core software, CRM, legal, accounting, internet, training, and supplies. If this base grows before billable work does, owner pay gets squeezed first, because there’s less margin left to draw.

Marketing rises from $25k to $150k, so the owner needs to watch CAC and close rate together. Here’s the risk: if leads don’t convert fast enough, cash burn climbs while profit lags. Reserve planning matters because minimum cash need reaches $785k in Month 9.

Spend Only When Demand Supports It

Keep discretionary spend on hold until utilization and pipeline can support it. Test each new tool, lease, or vendor against booked work, not hoped-for work. If a cost does not improve delivery or sales this month, it should wait.

Track monthly burn, CAC, and close rate in one view. That shows whether higher marketing spend is buying revenue or just adding noise. If overhead drifts up, reset the reserve target before owner draws or payroll feel the squeeze.

6

Compare owner income across low, base, and high project management scenarios

Owner income scenarios

Owner income moves with utilization, hiring, reserves, and client mix. Early losses can flip to strong profit by Year 3 and Year 5 if billable work scales as planned.

| Scenario | Low CaseUtilization risk | Base CaseHiring watch | High CaseClient concentration |

|---|---|---|---|

| Launch model | This is the Year 1 ramp case, where owner pay stays under pressure. | This is the Year 3 model, where the core salary is well covered. | This is the Year 5 scale case, where profit can support extra owner income. |

| Typical setup | About $434k revenue, 83% gross margin, 72% contribution margin, $287.5k payroll, and $25k marketing still end at -$79k EBITDA. | About $2.88M revenue, about 85% gross margin, $695k payroll, and $85k marketing support $1.314M EBITDA. | About $7.83M revenue, about 88% gross margin, $1.05M payroll, and $150k marketing support $4.907M EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyCash tight | $150k salarySalary covered | $150k salary + drawScale upside |

| Best fit | Use this to stress-test the first year and protect cash. | Use this as the main plan if hiring and utilization track to model. | Use this to test fast growth, but keep hiring pace and client mix in check. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Project Management Porter's Five Forces Analysis

- Project Management BCG Matrix

- Project Management Business Model Canvas

- 7 Essential KPIs for Project Management Services

- Project Management Business Plan Template in Pre-Written Word

- Increase Project Management Profitability: 7 Strategies for Founders

- How Much Does It Cost To Run A Project Management Firm Monthly?

- Project Management Service Startup Costs: $765K Setup, $785K Cash Need

- Project Management Financial Model Template in Excel

- How To Start A Project Management Business In 4 To 10 Weeks

- How to Write a Project Management Business Plan: 7 Actionable Steps

- Project Management Marketing Mix

- Project Management Marketing Plan

- Project Management Business Proposal

- Project Management PESTEL Analysis

- Project Management Pitch Deck Example Editable PPTX

- Project Management Business SWOT Analysis

- Project Management Value Proposition Canvas

Frequently Asked Questions

The model carries a $150,000 annual founder salary Potential upside comes from distributions, but only after reserves, taxes, debt service, and reinvestment are covered EBITDA moves from -$79,000 in Year 1 to $368,000 in Year 2 and $4907 million in Year 5, so timing matters