Owner income$4.8M

Owner income$4.8MHow Much Can A Purchase Order Financing Owner Make On $65M Funded?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$4.8M  Net margin85% to 71%

Net margin85% to 71% Revenue for target pay$41.1M

Revenue for target pay$41.1M Business difficultyHard

Business difficultyHard

Key Takeaways

- Funded volume is the main revenue engine.

- Fee rate changes quickly move gross income.

- Losses and capital cost can erase spread.

- Reserves should come before owner payouts.

Owner income$4.8MNet margin85% to 71%Revenue for target pay$41.1MBusiness difficultyHardWant to calculate PO financing owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the purchase order financing model?

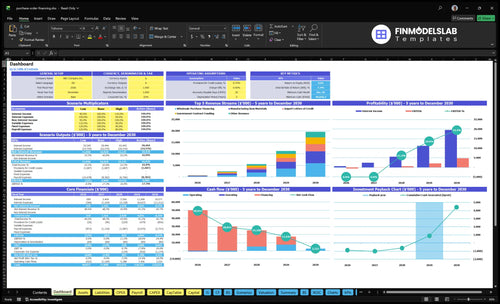

The screenshot in the Purchase Order Financing Service Financial Model Template ties funded volume, pricing, capital costs, reserves, and owner pay together; charts run from $65M to $1,405M funded volume, $1,226M to $23,538M loan interest revenue, and $149k to $101M operating profit before owner pay. Open the model.

Owner-income model highlights

- Dashboard and revenue assumptions

- Loan interest, liabilities, costs

- Scenarios and income outputs

What is the purchase order financing profit margin?

For Purchase Order Financing Service, profit margin is the fee spread after capital cost, losses, and overhead, and the key metrics sit behind What Are The 5 Core KPIs For Purchase Order Financing Service?. In Year 1, weighted customer yield is about 189% on $1,226M revenue from $65M funded volume, and after the $675k capital cost the net spread is about 85% before overhead and losses. By Year 5, yield falls to about 168% and the net spread after capital cost is about 71%, so the real margin gets squeezed as the book grows.

Year 1 margin

- 189% weighted customer yield

- $1,226M revenue on $65M funded

- $675k capital cost included

- 85% net spread before overhead

What cuts margin

- Year 5 yield drops to 168%

- Year 5 net spread is 71%

- 1-point loss costs $65k, $411k, $1405M

- 1-point funding cost rise costs $75k, $500k, $165M

How much can you make owning a purchase order financing business?

A Purchase Order Financing Service can make about $149k in Year 1 operating profit before owner pay, taxes, losses, payroll not supplied, and reserves; for the plan setup, see How To Write A Business Plan For Purchase Order Financing Service?. At scale, the researched model reaches $27M by Year 3 on $411M funded volume, or $101M by Year 5 on $1.405B funded volume.

Profit Snapshot

- $149k Year 1 operating profit

- Before owner pay and taxes

- Before losses and reserves

- Payroll not supplied in model

Key Drivers

- Funded volume and fee spread

- Funding cost and loss experience

- Compliance load and reserve policy

- Broker model: lower risk, lower economics

How much funded volume is needed to pay the owner?

For the Purchase Order Financing Service, use: required funded volume = (fixed overhead + target owner pay + reserve requirement) / net fee margin after capital cost. With $4.404M of Year 1 fixed overhead and about 85% net spread, overhead break-even is roughly $52M in funded volume before losses, reserves, payroll, and owner pay. If the owner draws too much, liquidity tightens, so keep cash buffers for delayed buyer payments, canceled orders, and lender covenants.

Break-even math

- $4.404M fixed overhead

- 85% net spread after capital cost

- ~$52M break-even funded volume

- Owner pay is extra

Liquidity watchouts

- Keep reserves for late buyer payments

- Cover canceled orders and disputes

- Stay within lender covenants

- Too much owner draw tightens cash

Want to see the main income drivers?

1

$6.5M-$140.5MFunded Volume

More funded purchase orders lift interest income fast, and the model scales from $6.5M in Year 1 to $140.5M in Year 5.

2

1pt=$65K-$1.4MFee Rate

A 1-point fee move on the same funded volume adds about $65K in Year 1 and $1.4M in Year 5.

3

$675K-$13.6MCapital Cost

Borrowing cost is a direct drag on take-home, rising from about $675K in Year 1 to $13.6M in Year 5.

4

1pt=$65K-$1.4MLoss Rate

Every point of credit loss or write-off cuts income by roughly the same $65K in Year 1 and $1.4M in Year 5.

5

$4.404MOverhead Load

Fixed payroll and operating spend set the breakeven bar, so tighter overhead matters until scale catches up.

6

$49.1MReserve Policy

Holding more cash and reserves lowers ROE, and minimum cash bottoms at $49.1M in Month 12.

Purchase Order Financing Service Core Six Income Drivers

Annual Funded Purchase Order Volume

Annual Funded Purchase Order Volume

Funded volume is the purchase order dollars that actually get financed and shipped, not the applications, quotes, or declined deals. Here’s the quick math: funded volume grows from $65M in Year 1 to $181M in Year 2, $411M in Year 3, $832M in Year 4, and $1,405M in Year 5, so fee revenue can scale fast if pricing and losses stay controlled.

That only helps owner pay if the book stays clean. One weak $1M order can wipe out a lot of fee income if the buyer disputes delivery or the supplier misses terms, so underwriting quality has to rise with volume. If losses, capital cost, and overhead outrun fee income, the owner gets less cash to draw.

Measure funded volume, not pipeline

Track funded dollars by month, buyer, and supplier, then compare them to fee revenue and loss rate. The core check is simple: funded volume × fee rate must stay ahead of capital cost, loss rate, and fixed overhead, which is about $367k monthly or $4.404M yearly.

When volume rises, tighten controls at the same time. Approve only orders with clear delivery proof, strong buyer credit, and a supplier with a solid track record, because growth without that discipline turns gross fee income into chargebacks, delays, and thinner owner distributions.

1

Effective Fee Rate

Effective Fee Rate

Fee rate is the price you charge on each funded purchase order. In this model, weighted loan yield is about 189% in Year 1, 177% in Year 3, and 168% in Year 5. Pricing should reflect risk, transaction duration, supplier terms, client controls, and buyer credit profile. This is a model assumption, not a compliance claim.

Here’s the quick math: on $411M of funded volume, a 1-point fee increase adds $411k before capital cost, losses, and overhead. That makes fee discipline a direct driver of owner pay. What this estimate hides is the drag from disputes, supplier misses, and slow collections, which can erase fee gains fast.

Track realized fee yield by deal

Measure the fee rate you actually collect, not just the quote. Break it out by deal length, supplier terms, buyer credit profile, and client control quality. If long, messy deals price like clean short ones, gross margin slips and less cash reaches the owner after funding cost and losses.

Test small pricing steps on similar orders and watch funded volume, margin, and cash conversion. Higher risk, longer duration, or weaker controls should earn a higher fee. That keeps the spread wide enough to cover capital cost, overhead, reserves, and owner distributions.

2

Cost Of Capital

Funding Cost

Cost of capital is what the business pays to fund purchase orders before the customer pays. It sits between fee income and everything else, so it directly changes gross profit and owner draw. In the model, $675k of Year 1 interest on $75M of liabilities is a very different burden than Year 5 interest expense of $13,603M on $165M.

This cost stays separate from payroll, software, legal, and default losses. One clean rule: if funding gets more expensive, the spread shrinks. The spread is the gap between customer fees and capital cost, and a 1-point move on $165M of liabilities changes annual profit by about $1.65M.

Track the Spread

Measure funding cost as a percent of average liabilities, then compare it to the fee charged on the same deals. You need funded balance, payment timing, and pricing by risk tier. If the fee rate does not clear the capital cost with room for losses and overhead, volume growth only makes the owner’s take-home thinner.

Watch tenor, supplier terms, and buyer credit quality every month. Faster customer payment and tighter supplier terms lower the amount outstanding, which cuts interest expense. If higher-risk orders need pricier capital, raise the fee or pass on the deal; otherwise the business is growing revenue with weak profit.

3

Underwriting Quality And Loss Rate

Underwriting Quality And Loss Rate

This driver is the share of funded volume lost to canceled orders, supplier nonperformance, buyer disputes, weak documents, or poor client controls. In purchase order financing, a 1-point loss on funded volume can equal $65k in Year 1, $411k in Year 3, and $1405M in Year 5, so higher loss rates cut fee income and owner distributions fast.

Use buyer concentration, supplier track record, purchase order validity, proof of delivery, and collections timing to estimate risk. A $1M order can wipe out a lot of fee income if the buyer disputes delivery or the supplier misses terms. Funded volume looks good on paper; loss rate decides what reaches the owner.

Cut losses before you scale

Track loss rate by buyer, supplier, and deal type, not just portfolio total. Require a confirmed purchase order, signed terms, delivery proof, and a clear pay date before funding. If one buyer or supplier starts driving claims, shrink exposure or reprice the deal.

Watch collections timing every week. Slow payment ties up cash and raises dispute risk, which hurts profit and the owner’s draw. Fund only what you can document end to end. If onboarding takes too long or files are weak, loss risk rises before revenue does.

4

Operating Expense Structure

Fixed Overhead

$367k per month or $4.404M per year in fixed overhead has to be covered before the owner sees real profit. This bucket includes cloud infrastructure, credit data and KYC services, legal and compliance, marketing, office rent and utilities, and professional liability insurance. It is the cost base that sits under every funded deal, so weak fee spread or soft volume can wipe out owner pay fast.

Here’s the key point: this is fixed overhead, not variable transaction servicing cost. That means it does not fall just because deal flow slows. Payroll data was not supplied, so owner income should be read before any additional staffing cost. If transaction margin does not clear this base, distributable profit stays thin or negative.

Watch the Cost Base

Track fixed overhead separately from deal-level servicing costs so you can see true spread. The clean test is simple: monthly gross fee income minus capital cost, losses, variable servicing, and $367k of fixed overhead. If the leftover cash does not support owner draw, the issue is either pricing, volume, or cost control.

Measure these lines every month: cloud, KYC and credit data, legal and compliance, marketing, rent, and insurance. Keep one control chart for fixed cost per funded deal and another for overhead as a share of fee revenue. If volume rises but overhead does not, owner income improves; if overhead climbs faster than funded volume, profit disappears.

- Separate fixed and variable costs

- Review overhead monthly

- Test fee revenue against overhead

- Delay staffing until margin is proven

5

Reserves And Reinvestment Policy

Reserve Fund And Reinvestment

Profitable does not mean fully distributable. In this model, reserve deposits rise from $150k in Year 1 to $32M in Year 5, so a growing share of cash stays parked as interest-earning assets instead of owner draw. That protects liquidity when collections slip, covenants tighten, or funded volume jumps.

Owner take-home is operating profit minus owner salary choices, retained capital, taxes, losses, and reinvestment. Here’s the quick math: more reserve build means less cash available now, even if fee revenue looks strong. Cash held back is not lost income; it is working capital for the next deal cycle.

Protect Cash Before Payouts

Track funded volume, expected collections timing, loss coverage, and covenant needs before setting distributions. Use a reserve rule that grows with volume, not a fixed monthly draw, so the firm can absorb delayed payments and still fund new orders. If reserves lag growth, owner pay becomes unstable fast.

- Set a minimum reserve floor.

- Reinvest before paying draws.

- Review cash weekly, not monthly.

- Link payouts to retained earnings.

What this estimate hides: reinvestment needs can spike when funded volume grows faster than collections. If the book scales without enough reserve build, the business may show profit on paper but still need to slow owner distributions to protect liquidity and keep funding capacity open.

6

Compare low, base, and high purchase order financing income scenarios

Owner income scenarios

Owner income moves with funded volume, loan spread, and overhead. Higher volume lifts profit fast because the service earns on financing fees and treasury income.

| Scenario | Low CaseDownside | Base CaseBase | High CaseUpside |

|---|---|---|---|

| Launch model | This is the lower-income path with Year 1 funded volume at $65M and about $149k operating profit before owner pay and reserves. | This is the modeled middle path with Year 3 volume at $411M and about $2.7M operating profit before owner pay and reserves. | This is the stronger earnings path with Year 5 funded volume at $1.405B and about $10.1M operating profit before owner pay and reserves. |

| Typical setup | The book is smaller, loan revenue is $1.226M, other interest income is $387k, and fixed overhead stays near $4.404M. | Loan revenue reaches $7.286M, other interest income adds $199k, and capital cost stays around $4.348M. | Loan revenue reaches $23.538M, other interest income adds $5.653M, and capital cost is about $13.603M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $149kLow run rate | $2.7MBase run rate | $10.1MUpside run rate |

| Best fit | Use this to test survival if volume starts slow and overhead stays fixed. | Use this as the most likely planning case for staffing and capital needs. | Use this to test upside if volume scales fast and the model keeps spreads healthy. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Purchase Order Financing Service Porter's Five Forces Analysis

- Purchase Order Financing Service BCG Matrix

- Purchase Order Financing Service Business Model Canvas

- What Are The 5 Core KPIs For Purchase Order Financing Service?

- Purchase Order Financing Business Plan Template in Pre-Written Word

- How Increase Profits In Purchase Order Financing Service?

- How Increase Purchase Order Financing Service Profitability?

- Purchase Order Financing Startup Costs With $75M Year 1 Capacity

- Purchase Order Financing Service Financial Model Template in Excel

- How To Open A Purchase Order Financing Service In 60 To 120 Days

- How To Write A Business Plan For Purchase Order Financing Service?

- Purchase Order Financing Service Marketing Mix

- Purchase Order Financing Service Marketing Plan

- Purchase Order Financing Service Business Proposal

- Purchase Order Financing Service PESTEL Analysis

- Purchase Order Financing Pitch Deck Example Editable PPTX

- Purchase Order Financing Service Business SWOT Analysis

- Purchase Order Financing Service Value Proposition Canvas

Frequently Asked Questions

The researched model shows about $149k in Year 1 operating profit before owner pay, taxes, losses, payroll not supplied, and reserves By Year 5, the same model shows about $101M before those exclusions Actual take-home depends on reserve policy, staffing, capital cost, and loss experience