Purchase Order Financing Startup Costs With $75M Year 1 Capacity

The cost to start a purchase order financing company depends less on desks and laptops and more on compliance, underwriting systems, staffing readiness, and the capital used to fund customer purchase orders In the researched model, disclosed monthly launch costs include $4,500 for cloud fintech infrastructure, $3,200 for credit data and KYC services, $6,000 for legal and compliance retainer, and $12,000 for marketing and lead generation That is $25,700 per month before payroll, insurance, office costs, and one-time setup work Separately, Year 1 financing volume is modeled at $65 million, supported by $75 million in debt capacity, so the client funding pool should not be blended into ordinary startup expenses

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates one-time capitalized startup assets only for a purchase order financing service before launch.

What this excludes This calculator excludes working capital, payroll runway, client funding capital, loan reserves, debt service, deposits, inventory runway, and recurring monthly costs like $4,500 cloud infrastructure and $3,200 credit data and KYC services. It only covers one-time startup CAPEX plus contingency.

What belongs on the CAPEX tab?

The Purchase Order Financing Service Financial Model Template CAPEX tab should show startup expenses, payroll ramp, launch timing, and depreciation or amortization. It should also test whether $25,700/month overhead, $65M Year 1 volume, and $75M debt capacity can cover fees, losses, and runway.

Key screenshot checks

- Startup expense categories

- Launch timing and period

- 7.5%-12% debt cost

- Fee and reserve assumptions

Why does a purchase order financing business need a financial model?

A Purchase Order Financing Service needs a financial model because it pays suppliers now and collects later, so timing can create a cash gap fast. The model has to show startup costs, operating runway, deal volume, advance rates, fee or interest yields, facility costs, defaults, cash conversion timing, and reserve requirements. That matters as volume scales from $65M in Year 1 to $1,405M in Year 5, with Year 1 pricing from 150% government contract funding to 240% supply chain bridging and debt cost spread from 750% institutional term loan to 1,200% mezzanine debt.

Model must show

- Startup costs and runway

- Deal volume by year

- Advance rates per transaction

- Fee or interest yields vs cost

Timing drives cash risk

- Pay suppliers before customer cash

- Track cash conversion timing

- Reserve for defaults and delays

- Scale from $65M to $1,405M

How much capital do you need to start a purchase order financing business?

You need capital in three buckets to start a Purchase Order Financing Service: setup costs, operating runway, and a separate client funding pool. Based on the model, disclosed non-payroll overhead is $25,700/month, or $308,400 for Year 1 before payroll, office, insurance, and one-time setup; client funding capacity is much larger at $75M against $65M in Year 1 financing volume.

Startup Capital Buckets

- Cover legal, systems, compliance setup

- Fund $25,700/month disclosed overhead

- Plan $308,400 Year 1 runway

- Add payroll, office, insurance separately

Client Funding Pool

- Support $65M Year 1 volume

- Secure $75M debt capacity

- Use warehouse and private credit

- Remember: funding cycles, but costs interest

What affects the cost to start a PO financing business?

The biggest startup costs in a Purchase Order Financing Service are legal review, Uniform Commercial Code (UCC) setup, underwriting tech, fraud controls, and the capital you need to fund each deal. If you self-fund advances, the main cost is tied-up cash; if you borrow, year-one debt can get expensive fast: 850% on a warehouse credit line, 1000% on a private credit facility, 750% on an institutional term loan, or 1200% on mezzanine debt. Supply chain bridging at 240% Year 1 interest needs tighter buyer and supplier checks plus bigger reserves.

Setup costs

- Review state lending and broker laws

- Price contract complexity up front

- Build UCC filing workflows

- Pay for underwriting and credit data

Capital costs

- Verify buyers and suppliers early

- Fund fraud controls and reserves

- Cover staffing and insurance

- Watch 750% to 1200% debt costs

Calculate Fuding Needs

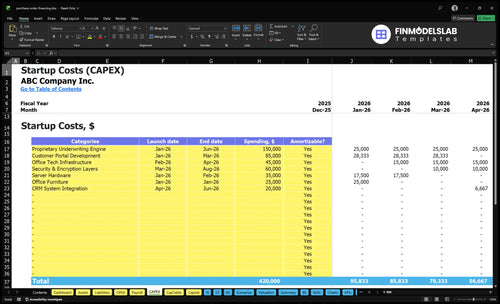

Startup cost summary table

This table breaks out startup CAPEX and excluded launch cash for a purchase order financing service.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Underwriting engine and servicing software | $150,000 | Build scope, automation depth, and model complexity | Yes |

| Customer portal and CRM integration | $105,000 | Portal features, onboarding flow, and sales workflow buildout | Yes |

| Security, encryption, and access controls | $60,000 | Data protection, encryption scope, and compliance hardening | Yes |

| Office tech infrastructure and servers | $80,000 | Workstations, server hardware, and office setup needs | Yes |

| Office furniture and equipment | $25,000 | Basic fit-out, desks, and essential equipment | Yes |

| Operating reserve and client advance pool | $49,057,000 | Launch overhead, funding timing, and reserve policy for Year 1 volume | No |

Purchase Order Financing Service Core Five Startup Costs

Legal And Compliance Setup Startup Expense

Legal Stack

Launching a purchase order financing service usually means entity formation, operating agreements, state lending or broker-law review, customer agreements, supplier verification terms, UCC process setup, privacy policies, AML, KYB, and data handling policies. Plan a $6,000/month legal and compliance retainer, then add attorney review for facility docs and state-specific gaps. There is no single US license rule.

Budget Inputs

Build the budget from filing fees, attorney hours, and document count. Price facility documents, supplier terms, and UCC setup separately, then add monthly review for new states or changes in broker or lender role. If the company funds directly, the legal scope is wider than when it only arranges financing.

Trim Risk

Start narrow to cut cost without cutting control. Use one borrower type and one assignment structure first, then template the customer agreement and compliance pack. Keep AML, KYB, privacy, and data rules in place from day one; those are cheaper to build than to fix after a funding error.

Answer First

Answer these before you spend on counsel.

- States served

- Borrower type

- Broker or lender

- Facility documents

- Direct funding or arranging

- Assignment structure

Underwriting And Servicing Technology Startup Expense

Workflow stack

The core stack is a one-time setup plus a recurring software run-rate. Build for confirmed purchase orders, supplier invoices, buyer approvals, shipping documents, and payment confirmations. The minimum system covers underwriting workflow, document upload, CRM, servicing tools, e-signature, cloud storage, reporting dashboards, access controls, audit logs, and secure file retention.

Budget inputs

Model recurring software at $4,500/month for cloud fintech infrastructure, then keep implementation separate as a one-time cost. Size the setup by user count, integration scope, and how many systems must sync before go-live. This is the base layer, not the full startup budget.

- Setup: one-time implementation quote

- Run-rate: $4,500/month

- Users: underwriters, ops, compliance

Keep it lean

Start with one workflow, one document list, and one dashboard. Delay custom builds until the process is stable, and avoid paying for seats no one uses. The big risk is weak access control or missing audit logs; the big waste is overbuilding integrations before launch.

Launch integrations

Plan integrations for CRM, e-signature, cloud storage, and servicing records before launch. The system should keep files secure and searchable, with audit trails tied to each deal. It is ready only when staff can move a transaction from intake to funding without chasing missing documents.

Credit Data And Fraud Verification Startup Expense

Risk Checks

Credit data and fraud verification are core risk-control costs in purchase order financing, not optional software. Plan on $3,200/month for business credit reports, KYB, sanctions checks, bank account verification, lien searches, transaction monitoring, and ongoing account reviews before any deal is funded.

Per-File Stack

Each file needs its own check stack: buyer verification, supplier diligence, fraud database hits, and any manual review triggered by a mismatch. Budget this as a monthly minimum plus per-file checks; the real cost rises with deal count and how deep you screen before wiring supplier funds.

- Business credit reports

- Buyer and supplier checks

- Bank and lien verification

- Ongoing account monitoring

Volume Pressure

Higher-risk growth lines need deeper screening. If Year 1 volume reaches 220% for import letters of credit and 240% for supply chain bridging, expect more monitoring, more exception handling, and more manual review. That makes the $3,200/month base a floor, not a ceiling.

Budget Inputs

Ask for the vendor’s monthly minimum, per-file fee, ongoing monitoring charge, and any escalation fee for adverse hits or manual review. Then map those fees to funded deals, because the right budget depends on how many files you underwrite and how often reviews turn up a red flag.

Staffing Readiness And Pre-Launch Payroll Startup Expense

Pre-Launch Team

Before launch, staff for underwriting, operations, compliance support, sales/origination, finance admin, contractor support, recruiting, onboarding, and training. The payroll amount is a required input; the source gives no dollar figure, so don’t invent one. Keep this pre-opening payroll separate from ongoing operating expense and working-capital runway.

Right-Size Hires

Use the lightest team that can still review files, move deals, and stay compliant. If the founder can lead underwriting early, outsource compliance and contractor support first, then add hires only when volume and turnaround demand it. One clean rule: don’t let payroll outrun process.

- Founder-led underwriting can cut early headcount.

- Outsource compliance before hiring full-time.

- Set deal-review timing before staffing up.

Sizing Questions

Staffing should map to $65M in Year 1 financing volume across five deal categories. The key inputs are who handles underwriting, whether compliance is outsourced, broker channel support, deal-review turnaround, and who manages facility reporting. Those answers tell you how much pre-launch payroll you really need.

- Who signs off on underwriting?

- Who owns facility reporting?

- What turnaround is required?

Launch Timing

Hire against the launch calendar, not hope. If recruiting, onboarding, and training start before deal flow is ready, payroll becomes a drag fast. Tie each role to a clear workload, then keep pre-launch spend inside the runway set aside for the first funded deals.

Originations Insurance And Launch Readiness Startup Expense

Launch budget

Your launch spend has two parts: $12,000/month for marketing and lead generation, plus insurance to support lender trust and fraud-sensitive intake. Cover the website, CRM setup, broker outreach, referral onboarding, industry directories, and launch campaigns. Track every lead by source so you can see which channels convert, not just which ones fill the pipeline.

Acquisition spend

Estimate this cost as months of launch × $12,000, then add setup work for the website, CRM lead routing, and partner outreach. This budget supports broker calls, referral partner onboarding, and industry directory listings. Use source tags in the CRM for broker, referral, outbound, and directory leads so you can measure conversion by channel.

- Tag every lead by source.

- Review conversion weekly.

- Pause weak channels fast.

Insurance stack

Cover errors and omissions, cyber liability, general liability, and D&O if you are raising capital. Do not guess premiums here; get quotes and confirm limits, deductibles, and coverage dates . This spend protects the platform’s credibility with lenders and partners, especially when handling supplier docs, customer data, and funding approvals.

Source tracking

Build the CRM so each deal shows where it came from: broker, referral partner, directory, outbound, or campaign. That lets you connect spend to referral conversion and spot weak intake paths before they create bad-fit deals. One clean rule helps: if a source cannot be tracked, it should not get budget.

Compare 3 Startup Cost Scenarios

Scenario table

Scenario scale changes cash needs fast because this model carries fixed compliance, tech, and payroll costs before loan volume ramps. Client funding capacity is modeled separately from setup cost.

| Scenario | Lean Launchlean validation | Base Launchbase controlled launch | Full Launchfull-service scale |

|---|---|---|---|

| Launch model | Founder-led underwriting with narrow scope and limited initial deal flow. | A professional setup with dedicated underwriting and recurring compliance work. | A staffed platform with deeper compliance, broader broker outreach, and stronger controls. |

| Typical setup | Use outsourced legal review, basic KYC, and light marketing. | Run a credit data stack, compliance review, and a steady sales workflow. | Add more underwriting staff, operations support, and tighter cyber protection. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $250,000 - $500,000low cash need | $750,000 - $1,200,000core setup | $1,500,000 - $2,500,000scale build |

| Best fit | Best for testing demand before adding a full credit team. | Best for operators who want controlled growth and repeatable deal flow. | Best for teams ready to scale volume fast and support larger borrowers. |

Planning note: These scenario ranges are researched planning assumptions, not exact quotes or lender offers.

Related Products

- Purchase Order Financing Service Porter's Five Forces Analysis

- Purchase Order Financing Service BCG Matrix

- Purchase Order Financing Service Business Model Canvas

- What Are The 5 Core KPIs For Purchase Order Financing Service?

- Purchase Order Financing Business Plan Template in Pre-Written Word

- How Increase Profits In Purchase Order Financing Service?

- How Increase Purchase Order Financing Service Profitability?

- Purchase Order Financing Service Financial Model Template in Excel

- How Much Can A Purchase Order Financing Owner Make On $65M Funded?

- How To Open A Purchase Order Financing Service In 60 To 120 Days

- How To Write A Business Plan For Purchase Order Financing Service?

- Purchase Order Financing Service Marketing Mix

- Purchase Order Financing Service Marketing Plan

- Purchase Order Financing Service Business Proposal

- Purchase Order Financing Service PESTEL Analysis

- Purchase Order Financing Pitch Deck Example Editable PPTX

- Purchase Order Financing Service Business SWOT Analysis

- Purchase Order Financing Service Value Proposition Canvas

Frequently Asked Questions

Plan runway separately from deal funding The model already shows $25,700 per month in disclosed non-payroll overhead, or $308,400 across the first operating year before payroll, office, insurance, and one-time setup Add a payroll runway layer and a reserve layer, because Year 1 financing volume is modeled at $65 million