Owner income$56K–$1.18M

Owner income$56K–$1.18MHow Much a Ramen Restaurant Owner Can Make: $56K to $118M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$56K–$1.18M  Net margin5.5%–43.8%

Net margin5.5%–43.8% Revenue for target pay$85K–$225K

Revenue for target pay$85K–$225K Business difficultyHard

Business difficultyHard

Key Takeaways

- More covers lift revenue without adding rent.

- Higher tickets help if waste stays controlled.

- Food, labor, and rent drive break-even most.

- Delivery volume can shrink margin fast.

Owner income$56K–$1.18MNet margin5.5%–43.8%Revenue for target pay$85K–$225KBusiness difficultyHardWant to test your ramen restaurant owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment.

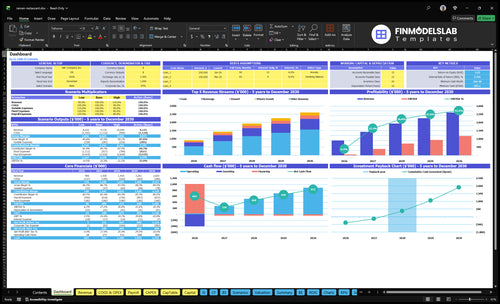

Want to see the Ramen Restaurant financial model?

The Ramen Restaurant Financial Model Template dashboard shows revenue, EBITDA, owner-income capacity, Month 4 breakeven, 28-month payback, and $565K minimum cash; open it.

Owner-income model highlights

- Owner-income capacity shown

- Revenue and EBITDA charts

- Assumptions drive every tab

Does a ramen restaurant owner need to work in the business?

A Ramen Restaurant owner does not have to work in the business, but this model already assumes a $70K manager and $80K head chef, so it is built as a manager-run shop. If the owner replaces the manager role, cash available can improve by about $70K before taxes; if the owner also cooks, the $80K chef cost becomes a major income lever. A passive shop only works with stronger sales, clean margins, and enough cash to pay staff before owner draws.

Owner in the shop

- $70K manager cost can be saved

- Quality and controls must hold

- Owner can cover key gaps daily

- Before-tax cash improves fast

Passive shop risk

- $80K chef cost is a big lever

- Sales must stay strong

- Margins must stay clean

- Cash must cover payroll first

How much revenue does a ramen restaurant need to pay the owner?

A Ramen Restaurant needs roughly $85K/month in model revenue before owner pay is a real discussion, and pay is safer only after Month 4 breakeven and cash above the $565K minimum need. See What Is The Most Important Indicator Of Success For Ramen Restaurant? because sales alone don’t matter if food cost, labor, rent, debt service, and reserves take the cash first.

Owner Pay Trigger

- Target revenue: $85K/month

- Model EBITDA: $47K/month

- EBITDA margin: 55.3%

- Pay starts after reserves

Cash Comes First

- Fixed payroll plus overhead: $51,950/month

- Variable costs come next

- Debt service comes before draws

- Comfort improves after Month 4

How many bowls of ramen per day to be profitable?

If one bowl equals one guest, the Ramen Restaurant needs about 55 covers a day in year one to match the model, and the rough operating break-even is about 42 daily covers with a $51 blended ticket, 175% variable costs, and $51,950 in monthly fixed payroll plus overhead. That leaves a thin cushion, so Friday and Saturday have to carry the week at 80 and 90 covers. Dine-in, takeout, and delivery all have to fit kitchen speed and seating limits.

Break-even math

- 55 covers per day in year one

- 42 covers per day at break-even

- $51 blended ticket used

- 175% variable costs assumed

Traffic split

- 385 weekly covers in the model

- Friday: 80 covers

- Saturday: 90 covers

- Keep service within kitchen limits

Want to see what drives ramen restaurant owner income?

1

55-119/dCustomer Volume

More covers spread fixed costs like rent and payroll, so owner take-home rises fastest.

2

$51-$62Average Ticket

A higher blended ticket lifts sales per guest without adding the same labor or rent.

3

175%-140%Food Cost Control

Tighter ingredient control keeps more of each bowl and drink sale in the owner's pocket.

4

$438K-$671KLabor Model

Payroll moves a lot as the room gets busier, so staffing to covers protects cash flow.

5

$10K/moRent Efficiency

Rent stays fixed, so every extra dollar of sales per seat improves owner take-home.

6

EditableChannel Mix

Delivery fees are not included here, so shifting dine-in versus off-premise mix can change take-home quickly.

Ramen Restaurant Core Six Income Drivers

Customer Volume And Throughput

Customer Volume and Throughput

Customer volume is the number of covers served each week. Here it rises from 385 weekly covers in Year 1 to 835 in Year 5, a gain of 450 covers. That lifts revenue without adding rent, so more of each extra bowl can flow to profit and owner pay.

The ceiling is operational. Saturday moves from 90 to 180 covers, and weak Monday-through-Thursday demand can leave fixed costs underused. Service speed, seat turnover, kitchen pacing, and open days decide whether the room turns demand into cash or into lost sales.

Track Turns, Not Just Traffic

Here’s the quick math: volume only helps if the restaurant can serve it. Watch covers per day, seat turnover, and covers by day of week. The model’s daily average rises from 55 to 119 covers, so the weekday gap matters as much as the weekend peak.

- Count covers by lunch and dinner.

- Measure table turn time.

- Match staffing to peak days.

- Test faster kitchen pacing.

What this estimate hides is fixed-cost drag. If Monday through Thursday stays soft, rent and labor sit there anyway, and owner income stays thin even with a strong Saturday. More open days only help when the room can stay busy enough to cover the shift cost.

1

Average Ticket And Menu Mix

Average Ticket And Menu Mix

Higher checks lift owner income when ingredient and labor costs stay controlled. In Year 1, the model assumes $45 midweek AOV and $55 on weekends; by Year 5, that rises to $55 and $68. That means more revenue from the same covers, which helps gross profit and cash flow if add-ons do not create extra waste or slow turns.

The mix also shifts from 60% food and 25% beverage in Year 1 to 55% food and 28% beverage in Year 5. Toppings, appetizers, drinks, desserts, and private events can raise the average ticket, but only if prep time and spoilage stay below the sales lift. One clean rule: sell more per guest, not more complexity per bowl.

Track AOV and add-on mix by day

Measure average order value by midweek and weekend, plus the attach rate for toppings, beverages, desserts, and events. Compare each add-on’s extra sales to its prep minutes and waste. If a high-selling item slows the line or throws off product usage, it can cut the owner’s take-home even when revenue looks better on paper.

- Track AOV by daypart

- Price add-ons for margin

- Limit waste on slow sellers

- Book events with clear minimums

2

Food Cost And Kitchen Yield

Food Cost And Kitchen Yield

Food cost percentage is cost of goods sold (COGS) as a share of sales. In this ramen model, listed food ingredients fall from 100% of sales in Year 1 to 80% in Year 5, and beverage ingredients fall from 40% to 30%. Broth yield, protein portions, noodle waste, topping control, and supplier pricing all flow straight into gross profit and the owner’s take-home pay.

Here’s the quick math: the plan says a 1-point cost swing on first-year revenue of $102M equals about $102K before tax. So if portions drift or waste rises, cash for payroll, rent, and owner draw shrinks fast even when sales look fine.

Track Yield, Not Just Price

Track recipe yield, not just vendor price: broth gallons per batch, protein grams per bowl, noodle trim loss, and topping counts. Then compare planned plate cost to actual sales mix. If a heavy lunch rush pushes portions off spec, margin drops before revenue does.

Use a weekly food cost % log by station and by menu item. The goal is simple: keep the bowl consistent, cut waste, and protect gross profit that funds owner pay after rent and payroll.

3

Labor Structure And Owner Role

Payroll And Owner Coverage

Payroll is the biggest fixed cost you can control after buildout. In year 1 it runs $438K across manager, chef, sous chef, line cooks, servers, bartender, and dishwasher; by year 5 it rises to $671K, or about $36.5K to $55.9K a month. If the owner fills shifts, cash out the door drops, but unpaid labor can hide a model that still cannot support paid management.

Replacing the $70K manager or $80K chef role changes take-home materially because those salaries sit inside the fixed labor base. The real risk is understaffing: slower turns, weaker service, and fewer repeat visits. Here’s the quick test: if labor savings hurt guest flow, you may lose more in sales and owner draw than you save in payroll.

Track Labor By Role, Not Just Total Payroll

Track paid hours, owner hours, and covers per labor hour by lunch, dinner, and weekend. Build the schedule around demand peaks, then test whether cutting one manager or chef layer still keeps turns and repeat visits stable. Use market-rate pay in the forecast so owner labor does not mask a weak staffing model.

- Separate owner hours from paid hours.

- Measure covers per labor hour weekly.

- Test speed before trimming staff.

- Budget market pay for key roles.

If owner labor is the only thing holding the model together, treat that as a warning. A cleaner forecast uses paid staff at the year 1 base of $438K, then checks whether the concept can still absorb the year 5 load of $671K without pushing service too thin.

4

Rent, Footprint, And Location Economics

Rent Burden

This driver is the fixed lease cost and the occupancy burden, meaning rent as a share of sales. At $10,000 per month or $120,000 per year, rent is about 118% of Year 1 revenue and about 44% of Year 5 revenue, so early cash is tight and later sales have more room for owner pay.

Here’s the quick math: the same lease gets easier only when covers, ticket size, and traffic rise. Estimate it with monthly rent, seat count, kitchen capacity, lunch and dinner throughput, and local foot traffic. A small footprint can work; a pretty space that cannot push enough bowls will bury profit fast.

- Track rent as sales percent monthly

- Watch covers by lunch and dinner

- Match seats to kitchen pace

- Check foot traffic by daypart

- Stress-test weak Monday to Thursday demand

Fit the lease to throughput

Before signing, test whether the room can process enough covers to cover a fixed $10K monthly lease. If sales stay soft, rent stays fixed, so every slow day squeezes gross profit and delays owner draws. The lease should fit the number of seats you can turn, not just the look of the space.

Measure the monthly gap between rent and revenue, then compare it with actual bowls sold. If lunch and dinner turns are strong, a smaller footprint can protect cash. If traffic is uneven, choose less space over more image. Better to rent a room you can fill than one you only admire.

5

Channel Mix, Takeout, And Delivery Fees

Channel Mix and Delivery Fees

Dine-in, takeout, and delivery do not earn the same margin. Delivery can raise sales, but commissions, packaging, and refunds cut owner income fast. For this ramen concept, listed disposable supplies are 15% of sales in Year 1 and 12% in Year 5, but third-party delivery commissions are not included, so net profit can be overstated if the model ignores them.

The key inputs are delivery mix, fee percentage, order count, average ticket, and refund rate. Ramen also loses quality in transit, so a weak delivery setup can hurt repeat visits and cash flow. Own-channel pickup usually protects more margin than marketplace delivery because it avoids commission drag and reduces quality-related refunds.

Track Net Margin by Channel

Here’s the quick math: more delivery only helps if net margin stays above dine-in or pickup. Track sales by channel, then subtract packaging, commissions, and refunds before you count profit. If delivery volume rises but repeat orders fall, owner pay can shrink even while top-line revenue looks better.

- Split orders into dine-in, pickup, delivery.

- Log fees and packaging by channel.

- Track refunds and repeat-rate weekly.

- Test pickup promos before adding delivery.

Own-channel pickup should be the first lever. It usually keeps more margin than third-party delivery, and it gives cleaner cash flow. If delivery is needed, price it with the fee percentage already built in, then watch whether the channel still covers labor and fixed costs after refunds.

6

Compare low, base, and high ramen restaurant owner income scenarios

Owner income scenarios

Owner income moves with guest counts, ticket size, staffing, and fixed rent. Year 1 is tight, while Year 3 and Year 5 support much stronger take-home if sales density holds.

| Scenario | Low CaseTight start | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the cautious case, where Year 1 traffic and tight cash keep owner income modest. | This is the modeled case, where Year 3 volume and margin support stronger owner income. | This is the upside case, where Year 5 density and discipline push owner income much higher. |

| Typical setup | Year 1 runs about 55 covers a day, roughly $1.02M of revenue, and $56k EBITDA, with owner draws constrained by reserves and debt. | Year 3 reaches about 95 covers a day, roughly $2.00M of revenue, and $711k EBITDA, with about $601k payroll behind the line. | Year 5 reaches about 119 covers a day, roughly $2.71M of revenue, and $1.18M EBITDA, with about $671k payroll and tighter sales density. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Up to $56kThin cash | Up to $711kCore case | Up to $1.18MHigh upside |

| Best fit | Use this to test early-month cash strain and whether the launch can stay solvent before volume builds. | Use this as the main operating plan for budgets, staffing, and lender discussions. | Use this to test a fully scaled dining room with strong weekday and weekend traffic. |

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or cash distributions.

Related Products

- Ramen Restaurant Porter's Five Forces Analysis

- Ramen Restaurant BCG Matrix

- Ramen Restaurant Business Model Canvas

- 7 Critical Financial KPIs for Your Ramen Restaurant

- Ramen Restaurant Business Plan Template in Pre-Written Word

- 7 Financial Strategies to Increase Ramen Restaurant Profitability

- How Much Does It Cost To Run A Ramen Restaurant Each Month?

- Ramen Restaurant Startup Costs: Plan Around $565K Before Opening

- Ramen Restaurant Financial Model Template in Excel

- How To Open A Ramen Restaurant In 6 To 12 Months

- How to Write a Business Plan for a Ramen Restaurant: 7 Steps

- Ramen Restaurant Marketing Mix

- Ramen Restaurant Marketing Plan

- Ramen Restaurant Business Proposal

- Ramen Restaurant PESTEL Analysis

- Ramen Restaurant Pitch Deck Example Editable PPTX

- Ramen Restaurant Business SWOT Analysis

- Ramen Restaurant Value Proposition Canvas

Frequently Asked Questions

In this model, first-year owner income capacity is tied to $56K of EBITDA, not a guaranteed paycheck Revenue is about $102M, or $85K per month, from 55 average daily covers By Year 5, EBITDA reaches $118M, but taxes, debt, reserves, and reinvestment reduce safe take-home