Owner income$296k-$4.24M

Owner income$296k-$4.24MHow Much Can a Real-Time Captioning Service Owner Make at $693M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$296k-$4.24M  Net margin49%-71%

Net margin49%-71% Revenue for target pay$577k-$5.94M

Revenue for target pay$577k-$5.94M Business difficultyHard

Business difficultyHard

A real-time captioning service owner can model Year 1 income around a $180,000 CEO salary plus possible distributions from $3374M of EBITDA, if cash, taxes, debt, capex, and reserves allow it Revenue starts at $693M in Year 1 and reaches $71279M by Year 5 in the researched case EBITDA margin rises from 487% to 712% as delivery costs fall and customer hours grow Owner take-home is not the same as revenue or EBITDA

Owner income$296k-$4.24MNet margin49%-71%Revenue for target pay$577k-$5.94MBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, gross margin, labor, fixed overhead, marketing, reserves, and target owner pay.

Planning note: Research-based planning estimate only. It excludes personal taxes, debt structure, and guaranteed wages, and it is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the full model?

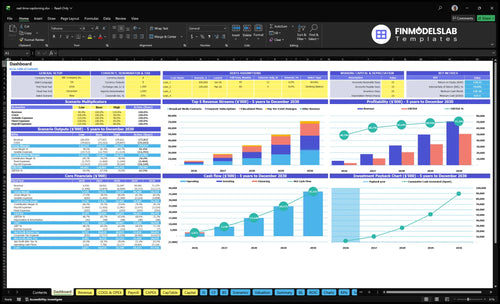

The Real-Time Captioning Service Financial Model Template screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions—open the model.

Owner-income model highlights

- Owner pay comes last

- Revenue and EBITDA charts

- Scenarios and cash timing

What affects real-time captioning service profit margin?

If you’re pricing a Real-Time Captioning Service, the margin comes down to captioner labor, cloud processing, quality checks, rush coverage, and the billing rate; see How To Launch Real-Time Captioning Service Business? for the setup side.

Here’s the quick math: in Year 1, freelance captioner fees are 18% and cloud processing is 5%, so delivery gross margin is 77%; by Year 5, those costs drop to 14% and 3%, lifting delivery gross margin to 83%.

Sales commissions stay at 4%, payment fees fall from 25% to 21%, and high-quality live work still needs backup capacity, so margin gets hit fast if rush coverage is thin.

Main cost drivers

- Labor is the biggest cost.

- Cloud processing adds 5% in Year 1.

- Quality assurance protects live accuracy.

- Rush coverage needs backup capacity.

Margin changes over time

- Year 1 delivery margin: 77%.

- Year 5 delivery margin: 83%.

- Sales commissions stay at 4%.

- Payment fees fall from 25% to 21%.

Can a real-time captioning service owner scale income?

Yes, Real-Time Captioning Service can scale income, but the owner stops acting like a captioner and starts running sales, scheduling, QA, contractor coverage, and client management. The model says revenue can grow from $693M to $71,279M over five years, and staff expands across engineering, sales, customer success, and QA. Owner income rises only if utilization and margin hold as volume goes up.

Revenue engine

- $693M to $71,279M over five years

- Owner shifts to sales and scheduling

- QA and contractor coverage become daily work

- Customer success protects repeat bookings

Scale risks

- Uneven bookings can hurt cash flow

- Staff shortages can cap delivery

- Cancellation windows can create idle time

- Quality misses and client concentration add risk

How much can I make owning a real-time captioning service?

A Real-Time Captioning Service owner can earn as a solo operator, small service provider, or agency-style owner; the model shows a $180k CEO salary plus $3.374M EBITDA in Year 1, rising to $50.747M EBITDA on $71.279M revenue by Year 5. EBITDA means profit before interest, taxes, depreciation, and amortization, but How Increase Real-Time Captioning Service Profits? starts with one rule: don’t treat all EBITDA as owner cash. Taxes, retained cash, staffing, capex, and quality coverage reduce what can be taken out.

Owner roles

- Solo operator: owner labor drives income

- Small provider: margin depends on staffed coverage

- Agency owner: salary plus business profit

- CEO pay: modeled at $180k

Cash limits

- Year 1 EBITDA: $3.374M

- Year 5 revenue: $71.279M

- Year 5 EBITDA: $50.747M

- Not all EBITDA is distributable cash

What drives owner take-home the most?

1

12.5-20.0hBillable volume

More billable hours per active customer raise revenue per account and flow straight into owner take-home.

2

$110-$240Average rate

The hourly rate ladder is a clean top-line lever because the delivery base stays mostly fixed.

3

77%-83%Delivery margin

As freelance captioner fees and cloud costs fall, more of each billable dollar becomes pre-tax profit.

4

55% corpClient mix

A heavier mix of corporate subscriptions and broadcast media contracts supports steadier cash and better pricing.

5

20.0hUtilization policy

Keeping active customers near the high end of billable hours spreads labor across more revenue and lifts EBITDA.

6

$244K/$634KOverhead reserves

A $244K monthly fixed base, a $634K cash floor, and a $180K CEO salary set how much profit reaches the owner.

Real-Time Captioning Service Core Six Income Drivers

Billable live captioning volume

Billable Captioning Hours

Billable captioning hours drive revenue because this model sells time. Rising from 125 monthly hours per active customer in Year 1 to 200 in Year 5 is a 60% increase in paid volume, before any pricing change. Segment assumptions also stretch from 12 pay-per-event hours to 160 broadcast hours, so mix matters as much as total demand.

The catch is capacity. Income improves only if sold hours grow faster than qualified captioner and QA coverage. Recurring contracts smooth staffing, while cancellation and no-show rules protect booked time. If sales outrun coverage, overtime, rework, or missed jobs can cut gross margin and delay owner pay.

Track Hours, Not Just Leads

Measure active customers, billable hours per customer, segment mix, cancellation rate, no-show rate, and the share of recurring work. That tells you whether revenue is coming from stable volume or from one-off spikes that are hard to staff.

- Book hours by segment.

- Set minimums for small jobs.

- Charge for late cancels.

- Match sales to coverage.

Use recurring contracts to fill the calendar first, then sell event hours into remaining capacity. If booked hours rise faster than captioner and QA coverage, service quality slips and the extra revenue can turn into lower take-home income.

1

Average real-time captioning rate

Average real-time captioning rate

Pricing sets revenue per billable hour. Year 1 assumptions are $150 corporate, $110 education, $180 broadcast, and $220 event; Year 5 rises to $170, $130, $200, and $240. Higher rates lift owner income only if clients accept the service level, rush support, and minimums. Rate pressure is strongest when buyers compare basic remote captions with higher-touch live accessibility work.

Inputs are segment mix, billable hours, minimums, and discounting. If pricing slips by $10 per hour on 1,000 monthly hours, revenue falls $10,000 before labor and cloud costs. So the real question is not just “what’s the rate?” but “what rate can you hold on the hardest jobs?”

Protect the hourly rate

Track realized rate by client type, not just quoted rate. Measure discounts, rush premiums, cancellations, and minimum booking compliance, because those decide whether the headline price turns into cash. A clean rate card plus stricter service levels helps keep premium work premium; without that, education and corporate buyers will push the price toward the lower end.

Test one change at a time: raise event minimums, charge for rush coverage, and separate broadcast from standard remote work. If the mix shifts toward higher-touch work, the owner keeps more of each billed hour, and that helps cover fixed overhead, taxes, and pay draws.

2

Gross margin after captioner delivery costs

Captioner Delivery Margin

Owner income comes from the spread between client billing and delivery labor. In Year 1, freelance captioner fees are 18% of revenue and cloud processing is 5%, so delivery gross margin is about 77%. By Year 5, those costs drop to 14% and 3%, lifting delivery gross margin to 83% and leaving more room for owner pay.

Owner-performed captioning can look more profitable, but it caps scale because income depends on the owner’s own hours. Subcontracted work scales better, but only if QA and backup coverage keep accuracy high and rework low.

Track the Spread by Job Type

Measure revenue, captioner fee %, cloud cost %, and rework for each client and event. Here’s the quick math: delivery gross margin = (revenue - delivery costs) / revenue. If a segment falls below the 77% to 83% range, owner take-home gets squeezed even when sales rise.

- Track billed hours and fee %.

- Separate cloud cost from labor.

- Test owner labor versus subcontractors.

- Keep backup coverage ready.

3

Client mix and contract quality

Client mix and contract quality

This driver is about which clients pay you and how reliably they renew. A shift toward 55% corporate subscriptions, 35% education, and 30% broadcast, with pay-per-event down to 15%, improves planning and utilization because recurring work is easier to staff than one-off jobs.

One-off events can still price higher, but they need more sales time, scheduling work, and backup coverage. The real cash question is payment terms, churn, renewal timing, and account concentration, because profit only helps the owner if it turns into cash fast enough to fund captioners and pay themselves.

Shift the mix toward recurring contracts

Track revenue by contract type, renewal month, days to collect, and the share of revenue from your largest accounts. Predictable subscriptions make it easier to forecast booked hours and avoid idle capacity; a heavy event mix can look strong on price but still squeeze margins through extra sales and scheduling effort.

Ask for shorter terms or faster billing on event work, and set renewal reminders before contracts roll off. If one client gets too large, concentration risk rises and one missed renewal can hit both revenue and cash flow at the same time.

4

Utilization and scheduling efficiency

Cluster Paid Hours

When paid hours are packed into larger blocks, each active customer can move from 125 to 200 billable hours per month. That lifts revenue without adding the same amount of extra staffing, so idle captioner time falls and owner take-home improves. If work is scattered across small event jobs, the calendar looks busy but the margin gets thin fast.

Broadcast and education contracts help fill open blocks because they repeat and are easier to schedule. One clean rule: booked time beats busy-looking time. Minimum booking rules, cancellation fees, rush premiums, and after-hours coverage protect margin when demand is uneven.

Fill the Calendar in Blocks

Track billable hours per active customer, cancellation rate, after-hours share, and the share of rush work. Those inputs tell you whether demand is becoming profit or just creating gaps. If booked hours are too thin, you need more captioner coverage to earn the same income, and that lowers the owner’s pay.

Use minimum booking rules for small events, then price late requests with rush premiums. Schedule recurring broadcast and education work first, because those blocks smooth labor and reduce idle capacity. Then fit one-off events around them, not the other way around.

- Track hours per active customer.

- Watch cancellations and no-shows.

- Price after-hours separately.

- Fill recurring blocks first.

5

Overhead, reserves, and owner role

Overhead and Cash Reserves

Fixed overhead runs about $244k a month for rent, software, insurance, utilities, legal and accounting, and marketing tools. That cost sits there even if billable captioning hours slip, so it can squeeze profit fast. In this model, payroll starts at $925k in Year 1 and reaches $228M in Year 5, so the owner’s draw has to sit behind the operating engine, not ahead of it.

The cash load also matters. The marketing budget rises from $150k to $550k, and the minimum cash need is $634k in Month 2. That means owner take-home can’t drain working capital, capex, taxes, or reinvestment. One bad month of collections or a staffing spike can turn paper profit into a cash crunch.

Keep Owner Pay Last

Track overhead as a fixed monthly burn rate and compare it to booked revenue, not just signed demand. The key test is simple: if gross margin does not cover $244k in overhead plus payroll and marketing, the owner should hold back draws. Cash reserve planning should also protect the $634k Month 2 need.

Use a rolling 13-week cash forecast and separate owner pay from operating cash. Watch payroll, marketing spend, and collections timing each week. If cash gets tight, cut discretionary spend before touching reserve levels needed for taxes, capex, and reinvestment.

- Forecast cash every week

- Cap owner draws last

- Protect Month 2 reserve

- Review fixed costs monthly

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with billable hours, pricing mix, and staffing load. Early years lean on salary, while higher-volume years can support optional distributions if cash stays strong.

| Scenario | Low CaseLean launch | Base CaseModeled scale | High CaseUpside run |

|---|---|---|---|

| Launch model | This is the lower earnings path, built on Year 1 revenue of $6.930 million and EBITDA of $3.374 million. | This is the modeled earnings path, using Year 3 revenue of $32.047 million and EBITDA of $21.015 million. | This is the stronger earnings path, using Year 5 revenue of $71.279 million and EBITDA of $50.747 million. |

| Typical setup | Year 1 is a lean launch with a 48.7% EBITDA margin, a $180k CEO salary, and a mix led by corporate subscriptions, education, broadcast, and event work. | Year 3 reflects a scaled operation with a 65.6% EBITDA margin, higher billable hours, and a heavier mix of corporate and education accounts. | Year 5 shows a 71.2% EBITDA margin, more broadcast and subscription volume, and enough scale that optional distributions become more realistic. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyLower income band | Salary plus optional distributionMid income band | Salary plus stronger optional distributionUpper income band |

| Best fit | Use this to stress-test slow sales, lower utilization, and a payroll-heavy start. | Use this as the core planning case for steady growth and controlled staffing. | Use this to test fast demand growth, larger contracts, and stronger cash generation. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Real-Time Captioning Service Porter's Five Forces Analysis

- Real-Time Captioning Service BCG Matrix

- Real-Time Captioning Service Business Model Canvas

- What Are The 5 KPIs For Real-Time Captioning Service?

- Real-Time Captioning Service Business Plan Template in Pre-Written Word

- How Increase Real-Time Captioning Service Profits?

- What Are Real-Time Captioning Service Operating Costs?

- Real-Time Captioning Service Startup Costs: $634K Cash Need

- Real-Time Captioning Service Financial Model Template in Excel

- How To Open A Real-Time Captioning Service In 6 To 12 Weeks

- How To Write A Business Plan For Real-Time Captioning Service?

- Real-Time Captioning Service Marketing Mix

- Real-Time Captioning Service Marketing Plan

- Real-Time Captioning Service Business Proposal

- Real-Time Captioning Service PESTEL Analysis

- Real-Time Captioning Service Pitch Deck Example Editable PPTX

- Real-Time Captioning Service Business SWOT Analysis

- Real-Time Captioning Service Value Proposition Canvas

Frequently Asked Questions

The researched model carries $180,000 in CEO pay and $3374M of Year 1 EBITDA on $693M revenue That does not mean the owner takes all EBITDA home Taxes, capex, debt service, working capital, and reserves come first By Year 5, EBITDA reaches $50747M on $71279M revenue