Owner income$250k base

Owner income$250k baseHow Much Residential Development Owners Make With 6 Closings

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$250k base  Net margin39%

Net margin39% Revenue for target pay$641k est.

Revenue for target pay$641k est. Business difficultyHard

Business difficultyHard

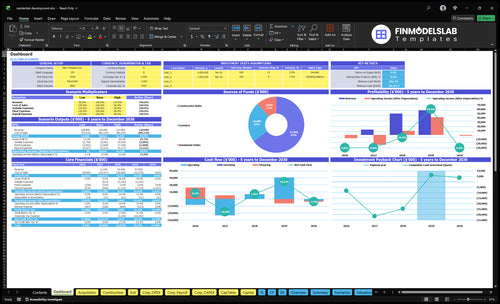

You’re planning owner pay before the projects have turned into cash This guide estimates residential development owner income over a 60-month model covering homes, townhomes, condos, and apartments, with 10 projects, 6 planned sale closings, $695M in construction budget, and $278k monthly fixed overhead It excludes personal tax advice, guaranteed returns, and one-off windfalls

Owner income$250k baseNet margin39%Revenue for target pay$641k est.Business difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on project timing, sales pace, financing, taxes, and retained cash. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full development cash flow?

This Residential Development Financial Model Template shows timing, cash needs, owner income, $695M build spend, and $278k overhead—open it.

Owner-income model highlights

- Revenue, margin, owner pay

- Month 3-60 pipeline timing

- Six planned sales tracked

- Land, overruns, reserves, splits

- Sales velocity, financing costs

How much profit does a residential developer make per project?

A Residential Development project’s profit is the sale price or exit value minus land, hard costs, soft costs, selling costs, financing, and allocated overhead; for growth context, see What Is The Current Growth Rate Of Your Residential Development Business?. Here’s the quick math: $480M across 6 planned sale projects means an average $80M land-plus-construction basis before selling costs and financing.

Profit Drivers

- Start with sale or exit value

- Deduct land and hard costs

- Deduct soft costs and overhead

- Deduct financing and selling costs

Model Limits

- 6 planned sale projects

- $480M land plus construction basis

- Selling costs fall from 55% to 35%

- Owner income comes after reserves and splits

Is it more profitable to sell or hold residential development projects?

For Residential Development, selling is better for near-term profit because it turns a project into lump-sum cash at closing, while holding can build rent income but delays owner payouts. In the 60-month model, there are 6 sale projects and 4 held or rented projects, and there is no sale inside the 60-month window for the held assets. Once all rented assets are active, site rental costs reach $355k per month, so owner take-home depends on whether cash is paid out, used for debt service, or kept for the next land buy.

Sell for fast cash

- Closes into lump-sum proceeds

- Speeds owner distributions

- Fits shorter hold periods

- Reduces rent-cycle exposure

Hold for cash flow

- Builds monthly rental income

- Delays distributions to owners

- Supports debt service needs

- Can fund the next land deal

How many homes does a developer need to sell to pay the owner?

You can’t pin this to a home count from the data given, because the model doesn’t show sale price or profit per home. What it does show is that $250,000 in annual owner pay has to be covered on top of $278k in monthly fixed overhead and project costs before any distributions, so owner pay is a planning output, not a guaranteed salary. With 6 planned closings across Months 22, 31, 36, 46, and 47, cash timing matters as much as total volume.

Owner pay math

- $250,000 annual CEO pay is the floor.

- $278k monthly fixed costs come first.

- Project costs also need coverage before payouts.

- No exact home count is shown here.

Timing risk

- 6 planned closings are spread out.

- Months 22, 31, 36, 46, 47 are key.

- Late sale proceeds can delay distributions.

- Accounting profit can show up before cash.

Want the six drivers behind owner income?

1

6 salesDeal Volume

More closings turn the 10-project pipeline into cash, so this is the biggest swing in owner take-home.

2

$150MLand Basis

Lower land cost and cleaner entitlements protect gross margin before a single home is sold.

3

39% ROEExit Value

Higher sale prices or exit values lift equity return, which is where the owner gets paid.

4

$695MBuild Cost

Tighter construction spending keeps the spread between sale proceeds and project cost from getting squeezed.

5

-$29.4MCapital Stack

Better financing terms can reduce cash strain while the model runs through its cash trough.

6

$278K/moOverhead

Fixed overhead and 35% to 55% selling costs eat cash fast, so reserve discipline matters.

Residential Development Core Six Income Drivers

Deal Volume And Closings

Closing Cadence

The model has 10 projects but only 6 planned sale closings in the 60-month window, and the source data dates five of them at Months 22, 31, 36, 46, and 47. That means owner income comes from completed, monetized units, not starts. If a closing slips, profit and distributions slip too, while overhead keeps running.

More closings can spread fixed costs, but only if sale prices, construction execution, capital, and absorption hold. Here’s the quick math: more volume helps cash only when units actually close. A stalled exit can delay both the project profit and the owner’s draw, even when the build is mostly done.

Track the Close Date

Track each project by expected close month, sale price, funding readiness, and completion status. Absorption, meaning how fast the market takes units, is the gate on cash. Build a rolling close plan and flag any project with less than full funding or a likely slip; one delayed close can push owner pay into the next period.

- Close month versus plan

- Sale price versus budget

- Funding before completion

- Buyer absorption by project

- Slip days and delay causes

1

Land Basis And Entitlements

Land Basis and Entitlements

When sale values are fixed, land basis moves owner income the other way: every extra dollar paid for land comes out of project profit. Here, owned land purchases total $150M across 6 projects, or about $25M per project. The 4 rented sites shift cost from upfront basis to monthly site cost, so cash flow timing matters as much as purchase price.

Entitlements are the zoning and permit approvals that let a project move forward. Better zoning or more density can raise profit per acre, but delays push construction and carrying costs later, which can cut owner take-home before a sale ever closes. If land is overpriced, the deal can look busy on paper and still leave little cash for the owner.

Buy Right, Entitle Fast

Track land cost per acre, usable density, entitlement months, and monthly carry on every site. The key question is simple: does the added sale value from zoning and density beat the land basis plus delay cost? If not, the owner is paying for upside that never reaches the bank account.

Build the forecast with purchase price, site rent, approval timing, and carry cost. One clean formula helps: owner profit = sale value - land basis - carry - construction. Faster approvals and lower basis protect distributions; slower approvals do the opposite, even if the project still sells well.

- Track basis per acre.

- Track density by zoning.

- Track entitlement months.

- Track monthly site carry.

- Track profit per acre.

2

Sale Price, Absorption, And Exit Value

Sale Price and Absorption

Sale price sets revenue, and absorption is the speed of sales. This plan shows sale timing for 6 projects, but it does not show sale prices or apartment exit values, so project profit and owner distributions are not yet calculable. Faster closings help cash return sooner and cut carry risk, but they do not prove higher margins.

Here’s the quick math: if a home sells sooner, the owner usually pays less carry on tax, insurance, interest, and overhead. But if pricing is weak or incentives rise, a fast sale can still leave less profit. The key limit is simple: timing is known, but exit value is still missing.

Track Net Price, Not Just Speed

Measure net sale price per unit, days on market, concessions, and closing costs for each project. Compare each signed contract to the plan so you can see whether faster absorption is improving cash flow or just pulling margin forward. If exit value assumptions stay blank, owner pay should stay tentative.

- Track signed contracts by month

- Track discounts and concessions

- Track net proceeds per closing

What this estimate hides: a unit can sell quickly and still underperform if the price is too soft. To protect take-home income, separate market upside from execution and model both speed and net pricing before planning distributions.

3

Construction Cost Control

Construction Cost Control

Construction cost control is where residential development protects gross margin. On a $695M total construction budget, and projects sized from $35M to $120M, hard cost overruns, site work surprises, change orders, and delays hit owner income before any sale proceeds are paid out. A deal can look profitable on paper and still turn tight after cost variance and reserve funding.

Measure each job with budget, committed cost, approved change orders, contingency left, and days delayed. Here’s the quick math: when actual cost rises, gross margin falls dollar for dollar, and that reduces cash for debt, reserves, and the owner draw. The input set is the full cost stack, not just the base build.

Hold Margin With Weekly Cost Tracking

Use a weekly cost-to-complete report. Compare budget, committed contracts, actual spend, and remaining contingency on every project. If a job drifts above plan, tighten scope fast; this is where site work surprises and late change orders start eating margin and push owner cash out of reach.

Require change orders in writing before work proceeds, and separate hard costs from delay carry. That helps you see whether the issue is bad pricing, field changes, or schedule slippage. The goal is not lower spend at any cost; it is more cash left for reserves and owner pay.

4

Financing And Capital Structure

Capital Stack Cost

Financing and capital structure cover debt amount, interest rate, draw schedule, equity share, preferred return, and the waterfall that decides who gets paid first. In this model, those terms are still TBD, so owner distributions cannot be priced yet. Without the loan and equity terms, you can’t calculate true cash left for the sponsor.

This driver hits income through interest carry, loan fees, and investor splits. Higher debt or slower draws usually raise carry and delay cash to the owner. Faster closings help, but only if the capital stack leaves enough spread after financing costs, reserves, and preferred return obligations.

Model The Waterfall Early

Start with the core inputs: debt amount, rate, draw schedule, equity share, preferred return, and waterfall. Then test how each change shifts cash flow and the sponsor’s take-home. If the model does not show these fields, owner pay is still a placeholder, not a forecast.

Track the gap between project profit and distributable cash. What this estimate hides: fees, carry, and investor priority can absorb early proceeds even when a project looks profitable on paper. This is planning support, not tax, securities, or legal advice.

5

Overhead, Reserves, And Reinvestment

Overhead, Reserves, And Reinvestment

Accounting profit is not the same as cash the owner can take home. With fixed overhead at $278k per month, that is $3.336M a year before payroll and project costs, so the business must fund a big cash base just to stay open. The modeled owner salary is $250k per year, or about $20.8k per month, but distributions still depend on reserves, debt service, contingencies, and reinvestment needs.

This driver includes the cash held for predevelopment work, construction gaps, and the next acquisition. If cash stays inside the business, owner pay can lag reported profit. Here’s the quick math: overhead first, then salary, then reserves, then anything left for distributions. In a development shop, cash discipline is what decides whether profit becomes a paycheck.

Track Cash Before You Draw It

Build a monthly cash forecast that starts with operating cash and subtracts $278k overhead, the $250k owner salary, debt service, and set reserves. That lets you see what is truly distributable. Do not treat project profit as spendable until the model shows cash after those uses.

- Track cash by project and entity.

- Ring-fence reserve dollars early.

- Separate reinvestment from owner draws.

- Update the forecast every month.

6

Compare low, base, and high owner-income scenarios without guessing sale values

Owner income scenarios

Owner income swings because closings are lumpy, projects take months to build, and fixed overhead keeps running before sale cash shows up.

| Scenario | Low Casesalary | Base Casedistribution | High Casecash retained |

|---|---|---|---|

| Launch model | Delayed sales and higher cost variance keep owner pay at the funded salary base. | Planned closings land on schedule, so owner pay can add limited distributions after reserves. | Stronger sale values and tighter costs lift owner income beyond salary and into larger distributions. |

| Typical setup | Projects slip, cash stays trapped in work in progress, and the model still shows breakeven at month 22 while minimum cash bottoms at -$29.391M in month 35. | Six modeled closings hit months 22, 31, 36, 36, 46, and 47, and fixed overhead runs about $27.8k a month before reserve needs are covered. | Pricing comes in stronger, selling costs run lower, hard costs stay controlled, and cash remains after reinvestment and reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyfunded salary | Salary + drawsafter reserves | Salary + retained cashcash retained |

| Best fit | Use this to stress-test the business when sales lag and reserves block payouts. | Use this as the planning case for a steady build-and-sell path with modest owner distributions. | Use this to test upside when the project stack throws off more free cash after growth spending. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Residential Development Porter's Five Forces Analysis

- Residential Development BCG Matrix

- Residential Development Business Model Canvas

- 7 Critical KPIs for Residential Development Success

- Residential Development Business Plan Template in Pre-Written Word

- How to Increase Residential Development Profit Margins

- How Much Does It Cost To Run Residential Development Monthly?

- Residential Development Startup Costs: $847M Before Runway

- Residential Development Financial Model Template in Excel

- How To Start A Residential Development Company In 2–4 Months

- How to Write a Residential Development Business Plan in 7 Steps

- Residential Development Marketing Mix

- Residential Development Marketing Plan

- Residential Development Business Proposal

- Residential Development PESTEL Analysis

- Residential Development Pitch Deck Example Editable PPTX

- Residential Development Business SWOT Analysis

- Residential Development Value Proposition Canvas

Frequently Asked Questions

The model supports a clear planning salary of $250,000 per year for the CEO / Managing Partner role Project distributions are separate and cannot be calculated from the provided data because sale prices, financing costs, investor splits, taxes, and reserves are not included Treat salary as planned compensation and distributions as deal-dependent cash