Owner income$175k

Owner income$175kHow Much Roller Compacted Concrete Owners Make On $4135M

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$175k  Net margin70.5% to 72.9%

Net margin70.5% to 72.9% Revenue for target pay$4.1M

Revenue for target pay$4.1M Business difficultyHard

Business difficultyHard

A roller compacted concrete contractor owner can model $175,000 in annual salary in this forecast, with any extra distributions depending on cash, debt service, and reserves On $4135M of Year 1 revenue, listed direct job costs are 295%, leaving a 705% gross margin before payroll, overhead, equipment debt, taxes, and owner draws After wages, fixed overhead, and marketing, the model shows about $16M of operating profit before debt, reserves, taxes, and capex That does not mean the owner should take $16M home, because startup equipment totals $148M and minimum cash falls to -$619,000 early in the model

Owner income$175kNet margin70.5% to 72.9%Revenue for target pay$4.1MBusiness difficultyHardWant to test your RCC owner-income target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner take-home depends on work mix, taxes, debt, weather, and timing. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see how owner income is checked in the model?

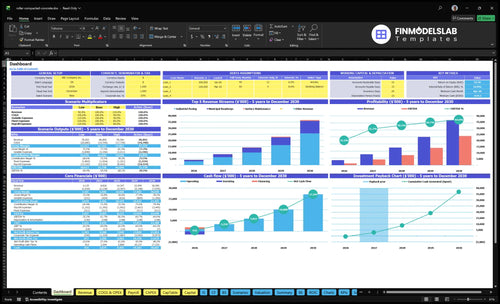

This screenshot shows revenue, margin, costs, reserves, and owner take-home logic in the Roller Compacted Concrete Services Financial Model Template. It also ties in the $175k salary, Year 1 revenue, startup equipment, cash runway, and debt planning—open the model after you understand the drivers.

Owner-income model highlights

- Owner pay scenarios

- Revenue and margin tabs

- Cash runway and reserves

How much does a roller compacted concrete contractor owner make?

For Roller Compacted Concrete Services, the modeled owner pay is $175,000 for the CEO and principal estimator role, not a universal market average; see How Increase Roller Compacted Concrete Services Profits? for the profit levers behind that number. The plan shows revenue growing from $4.135M in Year 1 to $8.826M in Year 2 and $14.347M in Year 3, while extra owner distributions should wait until debt service, retainage customer holdbacks, repairs, and reserves are covered.

Owner Pay

- Modeled owner salary: $175,000

- Role: CEO and principal estimator

- Owner-operated crews may take salary only

- Cash stays tight during early growth

Income Drivers

- Year 1 revenue: $4.135M

- Year 2 revenue: $8.826M

- Year 3 revenue: $14.347M

- Pay depends on margin and utilization

What margins affect roller compacted concrete contractor income?

Bid margin is the biggest driver of income in Roller Compacted Concrete Services, then cement and aggregate pricing, fuel, haul distance, QA testing, mobilization, and field productivity; if you want the pricing angle, see How To Write A Business Plan For Roller Compacted Concrete Services?.

Here’s the quick math: the Year 1 model lists direct costs at 185% for raw materials and admixtures, 65% for fuel and consumables, 25% for QA testing, and 20% for site logistics and mobilization, for 295% total listed direct costs and 705% left before payroll and overhead.

So your bid has to cover mix design, placement rate, compaction, curing, traffic control, contingencies, and rework risk. Miss one of those, and margin gets hit fast.

Top margin drivers

- Bid margin sets owner income.

- Cement and aggregate swing fast.

- Fuel rises with haul distance.

- QA testing cuts take-home cash.

Cost items to watch

- Mobilization can be a big drag.

- Field productivity changes job profit.

- Traffic control adds hidden cost.

- Rework risk can erase margin.

Does scaling a roller compacted concrete business increase owner income?

Yes, but only if the extra work keeps the crew and machines busy. In Roller Compacted Concrete Services, revenue is modeled to grow from $4.135M in Year 1 to $8.826M in Year 2 and $14.347M in Year 3, while staffing rises from 3 operators and 4 laborers to 6 operators and 8 laborers; if backlog, bid margin, and equipment utilization do not cover the added overhead, owner cash can shrink. Growth pays when the spread stays busy.

Scale helps cash

- Year 1: $4.135M revenue

- Year 2: $8.826M revenue

- Year 3: $14.347M revenue

- More volume can spread overhead

Cash risk at scale

- Staff grows to 6 operators

- Labor grows to 8 laborers

- More PMs and sales add cost

- Equipment debt can hit cash fast

Want the six biggest RCC income drivers?

1

$4.1M-$36.6MProject Volume

More completed paving work is the main income engine, moving revenue from $4.1M in Year 1 to $36.6M in Year 5.

2

$680-$850/hrBid Rates

Industrial and municipal pricing climbs from $680 to $850 per hour, so small rate gains add fast to owner take-home.

3

85-125hCrew Hours

Raising billable hours per active customer spreads the yard, truck, and management base over more revenue.

4

29.5%-24.7%Material Control

Materials, fuel, testing, and mobilization stay near a quarter of revenue, so savings flow straight to EBITDA.

5

$1.27MLabor Base

Year 1 payroll is $954K and fixed overhead adds about $311K, so the company carries a $1.27M base before fuel or materials.

6

-$619KCash Reserve

Cash turns negative by Month 4 at -$619K, so reserve funding and billing speed decide whether growth gets financed or stalled.

Roller Compacted Concrete Services Core Six Income Drivers

Completed-Project Revenue And Backlog

Completed-Project Revenue

Bids do not pay bills until work is completed, billed, and collected. That’s why completed-project revenue is the base that funds owner pay. The model’s sensitivity shows $4135M in Year 1, $8826M in Year 2, and $14347M in Year 3, so any slip in award timing or closeout pushes income out and tightens cash for the $175k owner salary.

Track Backlog, Not Just Bids

Measure signed backlog by start month, percent complete, retainage, and days from award to mobilization. A stronger backlog spreads fixed costs across more finished work and reduces cash strain in industrial paving, municipal roadways, and surface maintenance. Short seasons, delayed awards, and weather can leave crews and equipment idle even when bids are strong.

- Track billings versus collections.

- Watch retainage and aging.

- Map starts to weather windows.

- Flag mobilization gaps early.

1

Bid Pricing And Gross Margin Discipline

Bid Pricing And Gross Margin Discipline

Gross margin is what’s left after direct job costs. In RCC, those costs include mix, placement rate, compaction, curing, mobilization, traffic control, QA testing, fuel, contingencies, and trucking. The disclosed Year 1 model puts direct costs at 295%, so a weak bid can wipe out owner take-home fast and force the job to use operating cash before it is finished.

Missed trucking, rework, and slow production make it worse. One underpriced job can tie up crews and equipment while cash keeps leaving for labor, fuel, and testing. That’s why bid discipline is not just pricing; it’s cash protection.

Price From Field Inputs

Build every estimate from actual job inputs, then check it against the last completed project. Track mix yield, placement rate, compaction time, mobilization, traffic control, QA testing, fuel, and rework hours. If one of those moves, the bid should move too.

- Separate direct cost from profit.

- Add contingency for trucking misses.

- Raise markup on slow jobs.

- Walk away from thin margins.

That keeps gross profit intact and lowers the odds that operating cash has to finish the work.

2

Crew Productivity And Equipment Utilization

Crew And Equipment Utilization

This driver is how much the pavers, rollers, loaders, trucks, operators, and paving labor are on billable work instead of waiting. With Year 1 staffing at 3 specialized equipment operators and 4 field paving laborers, rising to 6 operators and 8 laborers by Year 3, income only rises when those hours turn into completed jobs.

Idle equipment still carries payroll, lease, insurance, maintenance, and financing pressure. Weather, maintenance downtime, bad scheduling, and slow site prep cut revenue twice: they delay cash coming in and keep fixed costs running. More utilization means the same fleet produces more completed revenue, which protects profit and owner pay.

Track Billable Days

Measure productive hours ÷ available hours, plus idle time by cause. If a site is not ready, a machine sitting still is not “cheap downtime”; it is paid labor and equipment cost with no offsetting revenue. The best schedule is built around ready sites, not hoped-for start dates.

- Count ready-to-pave days each week.

- Separate weather from planning misses.

- Match labor to active machines.

- Move crews fast between jobs.

Use utilization to test staffing growth. Year 3 headcount only works if the pipeline keeps machines moving; if not, labor and equipment costs rise faster than completed revenue. The goal is simple: more finished square footage from the same fleet, with less dead time and stronger take-home income.

3

Materials, Fuel, Trucking, And Job-Cost Control

Materials, Fuel, and Job Cost Control

On RCC work, owner pay lives or dies on job cost. The disclosed Year 1 mix is heavy: 185% of revenue for raw materials and admixtures, 65% of revenue for fuel and consumables, 25% of revenue for QA testing, and 20% of revenue for mobilization. That is 295% before labor and overhead, so small overruns can wipe out planned distributions.

Here’s the quick math: gross profit swings with cement content, aggregate source, haul distance, plant access, and waste. Long hauls, rejected mix, rework, and poor yield tracking push cash out faster than the job pays back, so a bid that looks fine on paper can still starve the owner’s draw.

Track Yield by Load

Measure each job by cement content, tons hauled, miles from plant, test failures, and waste. The key is simple: planned cost per yard versus actual cost per yard. If QA testing or mobilization starts running hot, raise price on the next bid or tighten the scope before the margin leak reaches owner pay.

Use a job-cost sheet that separates materials, fuel, trucking, testing, and rework. When those buckets are visible, you can spot a few points of overrun early, cut loss-making haul routes, and protect the cash needed for distributions.

- Track cost per ton and per yard

- Log haul miles and wait time

- Flag rejected mix and rework

- Compare bid vs actual daily

4

Overhead, Insurance, And Equipment Debt Burden

Fixed Overhead and Debt Burden

This driver is the fixed bill stack: yard and office lease, liability and umbrella insurance, fleet maintenance, software, utilities, safety training, and equipment debt. At $259k/month or $3.108M/year, the business has to clear that cash load before owner pay. In slow months, overhead still lands, so income can drop fast even if gross profit looks okay.

The big swing item is the $148M startup equipment base. If debt service is not covered by backlog, the gap hits cash, not just accounting profit. Repairs and bonding pressure make this worse, so the owner’s take-home income depends on keeping overhead tight and work booked ahead.

Track Monthly Burn and Debt Coverage

Measure overhead against completed, billed, and collected work, not just signed jobs. Here’s the quick math: $259k × 12 = $3.108M. If backlog slips, the fixed base does not. Track whether the next 90 days of work covers overhead, insurance, repairs, and debt service before any owner distribution.

- Backlog for the next 90 days

- Monthly insurance and repair spend

- Debt payment versus gross profit

- Cash left after overhead

Price job s so fixed overhead is spread across enough billable production. If a project drags, the same crew, yard, and equipment sit on the books longer, and owner pay gets squeezed. Keep accounting profit closer to cash profit by rejecting work that cannot cover the monthly burn.

5

Reserves, Reinvestment, And Cash-Flow Discipline

Cash Reserves Before Owner Pay

Reserves are the cash buffer that keeps profitable RCC work from turning into a cash squeeze. This model can still drop to a -$619k minimum cash balance in Month 4 because of retainage, slow collections, winter slowdown, and project timing. Owner draws should wait until debt service and reserve targets are covered, not just after accounting profit.

Reserve needs also cover equipment replacement, repairs, working capital, and bid bonds. With startup equipment capex at $148M, cash tied up in the fleet is a real risk, so taking cash too early can force borrowing or missed supplier payments. That makes owner income less steady, even when jobs look profitable on paper.

Protect Cash Before You Draw

Set a reserve floor and test it against the worst cash month, not the average month. Track billed vs. collected cash, retainage aging, and the next 90 days of debt service. If one delayed payment or one major repair breaks the plan, the reserve is too thin.

- Hold cash for winter gaps.

- Ring-fence repair money.

- Separate retainage from profit.

- Pause draws before cash dips.

Use project-by-project cash forecasts so each job funds its own working capital. When collections lag, keep distributions small until the buffer rebuilds. That rule makes owner pay steadier over the year, even if it trims the biggest checks in the strong months.

6

Compare lean, base, and high-utilization RCC owner-income cases

Owner income scenarios

Owner income depends on crew load, estimating time, and how fast overhead grows. The low case protects cash; the high case tests scale risk.

| Scenario | Low CaseLean owner-operator | Base CaseModeled plan | High CaseGrowth upside |

|---|---|---|---|

| Launch model | The owner stays close to estimating and field execution, and salary is the main take-home while revenue stays lighter. | This is the modeled first-year operating case, with the owner salary as the anchor and profit built on the Year 1 plan. | This is the higher-utilization path, where the owner keeps crews busier and takes on more management load. |

| Typical setup | This is the cash-first setup: the business runs near the lower end of the plan, the owner stays hands-on, and overhead growth stays restrained. | Revenue is $4.135M in Year 1, direct costs are about 70.5% of sales, and EBITDA is about $1.457M before debt, reserves, taxes, and capex. | Revenue moves into the $8.826M to $14.347M range, larger crews and backlog needs drive the plan, and cash stays tight as scale risk rises. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary-led take-homeLean pay | Salary plus profitBase pay | Salary plus larger upsideUpside pay |

| Best fit | Use this to stress-test a first-year owner who wants pay first and does not want to assume fast crew scaling. | Use this as the main planning case for a first-year owner who wants steady pay and a workable contractor model. | Use this to test what happens when growth is strong but staffing, cash, and execution pressure rise fast. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Roller Compacted Concrete Services Porter's Five Forces Analysis

- Roller Compacted Concrete Services BCG Matrix

- Roller Compacted Concrete Services Business Model Canvas

- What Are The 5 Core KPIs For Roller Compacted Concrete Services?

- Roller Compacted Concrete Business Plan Template in Pre-Written Word

- How Increase Roller Compacted Concrete Services Profits?

- What Are Operating Costs For Roller Compacted Concrete Services?

- Roller Compacted Concrete Startup Costs: $148M CAPEX Plan

- Roller Compacted Concrete Services Financial Model Template in Excel

- How To Start A Roller Compacted Concrete Business In 3 To 6+ Months

- How To Write A Business Plan For Roller Compacted Concrete Services?

- Roller Compacted Concrete Services Marketing Mix

- Roller Compacted Concrete Services Marketing Plan

- Roller Compacted Concrete Services Business Proposal

- Roller Compacted Concrete Services PESTEL Analysis

- Roller Compacted Concrete Services Pitch Deck Example Editable PPTX

- Roller Compacted Concrete Services Business SWOT Analysis

- Roller Compacted Concrete Services Value Proposition Canvas

Frequently Asked Questions

In this forecast, the owner role is modeled at $175,000 per year as CEO and principal estimator Extra distributions are not automatic They depend on completed revenue, reserves, debt service, and cash timing Year 1 revenue is $4135M, but startup capex is $148M and minimum cash falls to -$619k