Owner income$0-$70k

Owner income$0-$70kHow Much Can a Scrapbooking Business Owner Make With $70K Pay?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0-$70k  Net margin88%-90.5%

Net margin88%-90.5% Revenue for target pay$23.1k/mo

Revenue for target pay$23.1k/mo Business difficultyHard

Business difficultyHard

You’re estimating owner take-home for a US scrapbook retail business, not a guaranteed salary This model covers Month 1 to Month 60, including store revenue, gross margin, rent, payroll, marketing, inventory costs, reserves, and scenario logic, while excluding tax advice and owner-specific distributions

Owner income$0-$70kNet margin88%-90.5%Revenue for target pay$23.1k/moBusiness difficultyHardWant to test your own scrapbook store pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment. Taxes are excluded from this output, and this is not salary, tax, or owner distribution advice.

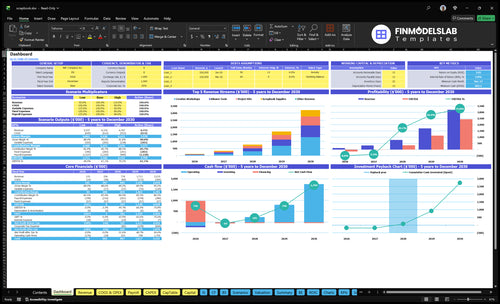

Checking owner income in the Scrapbooking model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Scrapbooking Financial Model Template—open it.

Owner-income model highlights

- Dashboard, startup costs, revenue assumptions

- Inventory margin, operating expenses, payroll

- Owner income outputs, cash flow

- Scenario testing for decisions

- $70,000 owner pay, -$161,000 EBITDA

- Month 21 breakeven, 37-month payback

- 006% IRR, 385 ROE

- $682,000 minimum cash, Month 24

What scrapbook store profit margin should owners expect?

If you’re opening Scrapbooking, expect a big gap between gross margin and what you can actually take home; see What Is The Estimated Cost To Open And Launch Your Scrapbooking Retail Business? for launch-cost context. Based on the provided mix, Year 1 gross margin after COGS is 880%, and after 40% marketing plus 15% processing fees, contribution margin is 825%. That still isn’t owner take-home, because dead stock, shrink, and slow movers can drain cash even when the accounting margin looks strong.

Margin math

- 880% gross margin after COGS

- 825% contribution after fees

- Supplies are 400% of Year 1 sales

- Albums and tools are 250%

Cash risk

- Workshops are 200% of Year 1 sales

- Kits are 150% of Year 1 sales

- Slow inventory cuts cash fast

- Markdowns can erase paper gains

Do scrapbook classes increase profit?

Yes—Scrapbooking classes can lift profit if room capacity, instructor time, and materials stay under control. In the mix, creative workshops are 200% of Year 1 sales mix and rise to 300% by Year 5, while workshop pricing moves from $45 to $55 and instructor staffing grows from 0.5 FTE to 1.0 FTE at a $35,000 annual salary.

Profit lift

- Classes drive repeat visits.

- Crop nights add add-on sales.

- Kits can raise basket size.

- Online orders widen reach.

Cost pressure

- Scheduling eats staff time.

- Fulfillment adds labor and packing.

- Marketing must fill seats.

- Inventory needs tight control.

How much revenue does a scrapbook store need?

If Scrapbooking wants a $70,000 owner pay target, it needs about $23,145 in monthly sales before taxes and reserves. Here’s the quick math: $4,720 fixed expenses + $8,542 non-owner payroll + $5,833 owner pay = $19,095; divide by an 82.5% contribution margin and you get $23,145. Add more sales if you have debt service, inventory reserves, shrink, or extra labor, because this is a sales target, not a payout guarantee.

Core sales target

- $23,145 monthly sales target

- $70,000 owner pay goal

- $19,095 total monthly burden

- 82.5% contribution margin

Costs that raise the bar

- Debt service adds monthly pressure

- Inventory reserves reduce cash

- Shrink cuts usable gross profit

- Extra labor lifts the target

Want the six main income drivers?

1

$267KSales Volume

More visits and better conversion push more orders through the register, and Year 1 traffic already supports about 74 buyers a week at 20% conversion.

2

$69Order Value

A 3-unit basket at a $23.15 weighted item price gives a $69.45 average order, so bundles and add-ons lift revenue fast.

3

88%Margin Mix

The mix leans on low-cost supplies and workshops, and Year 1 gross margin lands near 88% before overhead and payroll.

4

$15KInventory Turns

A $15K opening inventory keeps cash from sitting on shelves, and faster turns cut markdowns and shrink.

5

$172.5KLabor Load

Year 1 payroll is $172.5K including the owner, plus $4,720 a month of fixed overhead, so staffing discipline decides if sales become profit.

6

35%-50%Repeat Sales

Repeat customers rise from 35% to 50% of new buyers, and a 10 to 24 month lifetime plus online sales keeps revenue coming back.

Scrapbooking Core Six Income Drivers

Sales Volume And Average Order Value

Sales Volume and Basket Size

Owner income starts with enough visits that turn into buyers, then enough items in each basket. The Year 1 model uses 370 weekly visitors, a disclosed 200% visitor-to-buyer conversion, and basket math of 30 units per order at a weighted $2315 unit price, or about $6945 AOV. If conversion slips, breakeven moves out and Month 21 gets pushed back.

Sales only help if they create gross profit. Use the model’s 88% gross margin assumption and watch revenue × gross margin, not revenue alone. With fixed costs still in place, weaker traffic or smaller baskets cuts cash for owner pay fast. One clean miss on conversion can matter more than a small price tweak.

Track Visits, Buyers, and Basket Value

Measure three things every week: visitors, buyer rate, and average order value. Split baskets by category so you can see whether supplies, albums, tools, workshops, or kits are carrying the mix. If buyer rate drops or basket size falls, the owner’s draw gets squeezed even when sales look busy.

- Track weekly visitors and buyers.

- Watch units per order.

- Watch weighted AOV by category.

- Test bundle offers and add-ons.

1

Product Margin Mix

Product Margin Mix

Margin mix decides owner pay. This business sells supplies, albums and tools, creative workshops, and project kits, and Year 1 mix is listed at 400%, 250%, 200%, and 150%. Prices run from $850 for supplies to $4,500 for workshops, so profit depends on what sells, not just total sales.

The model shows 120% blended COGS and 880% gross margin in Year 1, with COGS easing to 95% by Year 5 only if buying discipline and supplier terms hold. If the mix drifts toward lower-yield items or markdowns rise, cash for overhead and owner draw gets squeezed fast.

Track mix before you chase more sales

Measure sales by category, unit price, and COGS every month. The key inputs are category mix, supplier cost, and markdowns, because those three move gross profit faster than total revenue. Here’s the quick math: if workshops and higher-priced items hold share, the owner keeps more cash from the same sales base.

- Track mix by category monthly.

- Watch COGS by supplier.

- Cap markdowns on slow movers.

- Test price changes by category.

Build the forecast around buying discipline and supplier terms, not one blended average. If those two slip, the Year 5 95% COGS target weakens, and the owner’s take-home income falls even if the store is busy.

2

Inventory Turnover And Markdowns

Inventory Turns

When paper sets, seasonal kits, tools, and embellishments sit too long, cash gets trapped on shelves and owner pay shrinks. This model starts with a $15,000 inventory buy, and Year 1 product wholesale cost is 100% of cost basis, so slow turns hit cash before profit. The key inputs are sell-through, shrink, reorder limits, and markdown timing. One line: if stock does not move, take-home does not move either.

Here’s the quick math: accounting profit can look fine while inventory cash lags, because unsold units still tie up money until they sell or are cleared. Watch items with short life or changing themes first, since those are most likely to need discounts. If clearance starts late, margin falls and the business can miss the path to Month 21 breakeven.

Track Sell-Through

Use a simple rule set: track units sold by SKU weekly, count aging stock weekly, and cap reorders on slow paper designs and seasonal kits. Set a markdown trigger before stock gets stale, not after. The goal is to convert inventory back to cash fast enough to protect gross margin and keep owner draw funded from real sales, not from money stuck on the shelf.

- Measure sell-through by SKU weekly.

- Flag stock older than 60 days.

- Cut reorders on weak movers.

- Clear seasonal goods early.

- Count shrink in every closeout.

What this estimate hides is the timing gap: even good products can hurt income if the cash cycle is slow. Tie markdowns to a fixed calendar and a stock-age limit, then review it against cash on hand. That keeps inventory from becoming hidden debt.

3

Classes, Crop Nights, And Events

Workshop Events

Classes and crop nights can lift income, but only if you control seat fill, ticket price, materials, and instructor FTE. In Year 1, workshops are 200% of the sales mix, then 300% by Year 5. The workshop price rises from $4,500 to $5,500, while materials stay at 20% of revenue in Year 1 and 15% in Year 5.

Here’s the quick math: if the room is half full, the fixed event cost hits harder, and take-home pay falls before rent and payroll even show up. Instructor labor grows from 0.5 FTE to 1.0 FTE, so empty seats hurt margin fast. Events only help if each session clears its direct labor and material cost.

Hold Fill Rate Above Break-Even

Track booked seats, show-up rate, and gross profit per event. Use a simple rule: if a session won’t cover materials plus instructor hours, don’t run it. That keeps cash from leaking on weak nights and protects owner draw.

Use deposits, advance sign-ups, and a minimum headcount before staffing. Then compare each event’s revenue to its labor and supply cost, not just to total store sales. A small change in attendance can swing margin a lot when labor is already at 1.0 FTE.

- Track fill rate by session.

- Price above direct event cost.

- Cut low-attendance dates early.

4

Fixed Costs And Staffing

Fixed Burn and Staffing

Fixed monthly costs of $4,720, led by $3,500 rent, set the cash floor before profit reaches the owner. With $172,500 in Year 1 payroll, including the $70,000 owner/operator salary, recurring payroll averages $14,375/month. That makes recurring monthly overhead about $19,095 once fixed costs and owner pay are included.

The main risk is staffing too tight or too rich. Non-owner payroll of $102,500 is about $8,542/month, so each labor hour has to support sales, classes, and service. Owner coverage can save cash early, but unpaid owner hours lower cash burn, not true income. If service slips, repeat business can fall with it.

Track Labor Against Gross Profit

Watch fixed cost per open day, payroll per sales dollar, and labor by role. If rent, wages, utilities, software, insurance, and local marketing rise faster than gross profit, owner pay gets squeezed first. The goal is not the cheapest team; it’s enough coverage to protect service and margin.

- Track rent as a cash floor

- Separate owner and non-owner labor

- Test staffing by peak hour

- Match hours to workshop demand

- Cut slow software and ad spend

If the owner is filling gaps too long, document those hours as a bridge plan. Replace them only when sales can support paid labor without pulling owner income down. That keeps the business from looking profitable on paper while still starving cash in the bank.

5

Repeat Customers And Online Sales

Repeat Buyers And Online Sales

This driver is the gap between a one-time walk-in sale and a longer stream from repeat buyers, clubs, kits, subscriptions, and email-driven orders. In the model, repeat customers are 350% of new customers in Year 1 and 500% by Year 5, with repeat lifetime growing from 10 to 24 months. That lifts lifetime value (LTV), meaning the gross profit one customer can bring over time.

Online sales can help, but they only improve owner pay if each order clears the $100 monthly platform cost, payment fees, fulfillment time, shipping, and marketing. With repeat order frequency rising from 0.5 to 0.8 orders per month, the business wins when every order adds margin after those costs, not just revenue.

Measure Repeat Margin

Track repeat rate, order frequency, and gross profit by channel. Here’s the quick math: margin per order minus platform, payment, shipping, pack time, and marketing is the cash that can fund owner draw. If online orders do not beat store sales on contribution margin, they can grow revenue and still shrink take-home pay.

Use email lists, kits, clubs, and subscriptions to lift lifetime value, then test whether buyers return within 10 months or stay near 24. The fastest control is simple: watch customer groups by month, cap free shipping thresholds, and drop slow offers that create orders with weak margin.

- Repeat buyers by month

- Orders per customer

- Average order value

- $100 platform fee

- Packing and shipping cost per order

- Email, club, and subscription sales

6

Compare lean, base, and strong owner-income scenarios

Owner income scenarios

Owner pay starts as a cash-funded launch draw, reaches breakeven around Month 21, and can open to distributions only when traffic, repeat buying, and margins scale.

| Scenario | Low CaseLaunch risk | Base CaseBreakeven | High CaseScale-ready |

|---|---|---|---|

| Launch model | Year 1 owner pay is a cash-funded draw because EBITDA is still negative at -$161,000. | By Month 21, operations can support the modeled $70,000 owner pay from the business base. | In Year 5, stronger traffic and repeat buying can support owner pay plus distributions after core obligations are covered. |

| Typical setup | Traffic is still building, conversion is 20.0%, repeat buying is 35.0% of new customers, and fixed rent and wages outrun sales. | Sales cover the breakeven point, with about $23,100 in monthly sales needed before taxes and reserves. | Year 5 uses 35.0% visitor conversion, 50.0% repeat customers, a 24-month repeat life, and a 30.0% workshop mix, with EBITDA at $2,438,000. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $70,000 cash-funded payCash pay | $70,000 salary supportBreakeven pay | Salary plus distributionsDistribution upside |

| Best fit | Use this to test the launch period when owner pay depends on cash, not profit. | Use this for payroll planning once sales are steady enough to cover fixed costs. | Use this when cash is strong enough for owner pay, inventory, debt service, and reserves. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Scrapbooking Porter's Five Forces Analysis

- Scrapbooking BCG Matrix

- Scrapbooking Business Model Canvas

- 7 Essential KPIs to Track for a Scrapbooking Retail Business

- Scrapbooking Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Scrapbooking Business Profitability

- How Much Does It Cost To Run A Scrapbooking Business Monthly?

- Scrapbook Business Startup Costs: $47K Setup Plus $15K Inventory

- Scrapbooking Financial Model Template in Excel

- How To Open A Scrapbooking Store In 8-16 Weeks With First Sales

- How to Write a Scrapbooking Business Plan: 7 Actionable Steps

- Scrapbooking Marketing Mix

- Scrapbooking Marketing Plan

- Scrapbooking Business Proposal

- Scrapbooking PESTEL Analysis

- Scrapbooking Pitch Deck Example Editable PPTX

- Scrapbooking Business SWOT Analysis

- Scrapbooking Value Proposition Canvas

Frequently Asked Questions

The researched model includes $70,000 in annual owner/operator pay before taxes That pay is not fully profit-supported in the first year because EBITDA is -$161,000 The store reaches breakeven in Month 21, so early income depends on startup cash, owner labor, and whether the owner takes the full modeled salary