Owner income$278.4M

Owner income$278.4MHow Much Does A Steel Plant Owner Make At 430,000 Tons?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$278.4M  Net margin77%–80%

Net margin77%–80% Revenue for target pay$8.9M

Revenue for target pay$8.9M Business difficultyHard

Business difficultyHard

Key Takeaways

- Saleable tons spread fixed costs; utilization drives profit.

- Blended pricing and mix matter more than tonnage.

- Raw material spread and yield protect gross margin.

- Cash flow depends on debt, inventory, and reserves.

Owner income$278.4MNet margin77%–80%Revenue for target pay$8.9MBusiness difficultyHardWant to test your steel plant owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed salary, tax advice, or owner distribution advice.

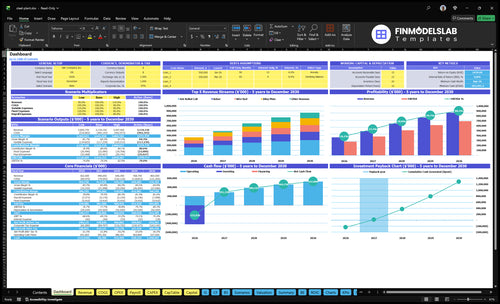

Want to check owner income in the Steel Plant model?

This screenshot shows tons, revenue, gross margin per ton, operating profit, and owner-income planning; open the Steel Plant Financial Model Template.

Model highlights

- Owner-income planning outputs

- Revenue and margin view

- Early, stable, mature scenarios

- Mix, pricing, unit costs

- Overhead, logistics, commissions

- Capex, debt, working capital

- Charts: $3.63B to $8.655B

- Output: 430k to 840k

- Profit: $2.794B to $6.978B

Can a small steel plant be profitable?

A Steel Plant can be profitable, but only if it runs close to the modeled output; underused plants get hit hard by fixed costs and wages. In Year 1, $6,746M in fixed expenses and listed wages sit in front of debt and reserves, while 430,000 tons of output brings about $3,630M revenue and $2,794M pre-debt operating profit. By Year 5, 840,000 tons lifts revenue to about $8,655M and pre-debt operating profit to about $6,978M, but compliance, market cycles, debt load, and capex reserves can still cut owner take-home.

Year 1 case

- 430,000 tons output

- $3,630M revenue

- $2,794M pre-debt profit

- $6,746M fixed costs and wages

Year 5 case

- 840,000 tons output

- $8,655M revenue

- $6,978M pre-debt profit

- Debt and reserves still matter

What affects steel plant profit margin?

Margin in a Steel Plant is mostly a pricing and cost-control story: with a Year 1 blended selling price of $844 per ton and direct unit COGS of about $98 per ton, gross margin per ton after unit COGS and 50% plant overhead is about $704. If you want the startup math behind that base case, see How Much Does It Cost To Open, Start, Launch Your Steel Plant Business?

What cuts margin

- Selling price moves profit first.

- Scrap and alloy costs hit COGS.

- Electricity and labor stay material.

- Yield loss, downtime, and logistics bite.

What lifts margin

- Base case margin is about $704/ton.

- Direct unit COGS averages only $98/ton.

- AHSS Sheet rises from $2,500 to $2,800/ton.

- Better product mix raises blended price fast.

How much can a steel plant owner take home?

A Steel Plant owner cannot take home the full $2,794M Year 1 pre-debt operating profit on $3,630M revenue; see What Is The Current Growth Rate Of Steel Plant's Overall Production? for the production context behind that scale. That profit equals about 77.0% of revenue, but actual take-home comes only after debt service, taxes, reserves, maintenance, working capital, and reinvestment.

What owner can take

- Salary: not specified in the data

- Distributions: paid after required cash uses

- Dividends: depend on ownership and approvals

- Cash flow: not equal to accounting profit

What reduces it

- Pay debt service first

- Cover taxes and maintenance

- Fund working capital needs

- Keep lender or board reserves

Want to see the main steel plant income drivers?

1

430K-840KtProduction Utilization

Higher output spreads the $4.416M annual fixed base across more tons, so utilization is the first cash lever.

2

$844-$1,030/tPrice Mix

A better mix lifts blended selling price from about $844 to $1,030 a ton, and that feeds straight into operating profit.

3

$704-$874/tRaw Spread

The margin per ton moves from about $704 to $874, so scrap, alloy, and yield discipline decide most of the gross profit.

4

$2.9M-$5.5MOperations Efficiency

Year 1 payroll is about $2.92M and reaches $5.46M by Year 5, so labor and energy control protect margin as volume grows.

5

$425MUptime Buffer

With $425M of planned capital spending, lost uptime or thin reserves can turn a strong plant into a cash squeeze fast.

6

24 moCash Load

Cash dips by Month 9, so debt terms, working capital, and reinvestment decide how much cash reaches the owner.

Steel Plant Core Six Income Drivers

Production utilization

Saleable Tons Utilization

Utilization is the share of output that becomes saleable tons, not theoretical capacity. For a steel plant, that matters because fixed costs like insurance, security, rent, software, R&D, marketing, compliance, and management payroll stay in place when tons fall.

Here’s the quick math: saleable output rises from 430,000 tons in Year 1 to 840,000 tons in Year 5. With $6,746M of Year 1 fixed expenses plus wages, every extra ton helps spread overhead and lifts operating profit, cash flow, and the owner’s draw.

Track Saleable Tons, Not Capacity

Measure downtime, demand, shift coverage, yield loss, and product routing. Those inputs tell you why saleable tons miss plan and where margin leaks out before overhead hits the P&L.

- Saleable tons each week

- Downtime hours by cause

- Yield % by product line

- Shifts staffed vs planned

If utilization slips, fixed costs do not shrink with it, so profit drops fast. Keep the forecast tied to saleable tons, not furnace nameplate capacity, or owner pay will look better on paper than in cash.

1

Selling price and product mix

Selling Price and Product Mix

Revenue per ton matters more than tonnage alone. Here’s the quick math: blended price rises from about $844 per ton in Year 1 to about $1,030 per ton in Year 5, while product prices range from $750 per ton for Rebar in Year 1 to $2,800 per ton for AHSS Sheet in Year 5. Mix, contracts, grade, and form shape gross margin and owner take-home pay.

A plant can sell more tons and still earn less if the mix shifts toward lower-priced products or price caps. The inputs that matter are tons by product, contract price, customer mix, and value-added processing. Headline steel prices do not guarantee owner income; cash only improves when the blended price holds up against direct cost and overhead.

Track mix, not just tons

Measure tons by product line, average selling price, and blended price per ton each month. Break revenue into Rebar, coil, sheet, and alloy grades so you can see which mix lifts margin and which mix drags it down. If AHSS or other high-value grades are slipping, owner profit can fall even when total tons hold steady.

- Track price by grade weekly.

- Forecast mix by customer contract.

- Test value-added processing returns.

- Watch market-cycle price resets.

Use contract terms and customer demand to protect the higher-priced mix. If pricing moves from $844 to $1,030 per ton, that extra spread flows through revenue first, then gross margin, then owner draw. If onboarding or processing delays push sales toward lower-grade stock, the cash benefit shrinks fast.

2

Raw material spread and yield

Raw Material Spread

Raw material spread is the gap between finished steel price and input cost, and it hits gross margin before overhead, debt, or owner pay. In Year 1, direct unit COGS total $4,232M versus $3,630M revenue, so the spread is already under pressure by $602M on a simple comparison.

This driver includes scrap, iron units, alloys, refractory use, purchasing discipline, and yield loss. Unit COGS by product are $95 for Hot Rolled Coil, $128 for Alloy Plate, $227 for AHSS Sheet, $86 for Rebar, and $104 for Wire Rod. If yield slips, the owner feels it fast in lower cash available for pay.

Improve Yield and Buy Better

Track spread by product line: sales price per ton, melt cost, scrap mix, and tons lost to rework or off-spec output. The quick math is simple: selling price minus direct input cost minus yield loss. If the spread narrows, gross margin falls even when tons shipped hold steady.

Watch purchase timing, charge mix, and furnace yield by heat, then compare plan vs actual every week. Use saleable tons, not theoretical tons, and flag any step that raises scrap or alloy use. Small yield gains matter because they protect the cash that can fund reserves and owner distributions.

3

Energy and labor efficiency

Energy and labor efficiency

Conversion costs are the cost to turn raw inputs into saleable steel. Here, direct electricity runs $22 to $35 per ton and direct operating labor runs $14 to $30 per ton. Add 15% of revenue for energy overhead and 10% of revenue for indirect labor, and gross margin can shrink fast before profit reaches the owner.

The owner’s take-home income improves when furnace uptime, shift efficiency, and staffing mix improve. Listed wages start at $233M in Year 1 and rise with engineers, operators, and maintenance technicians, so weak output spreads those dollars over fewer saleable tons. One clean rule: more tons, fewer stoppages, better labor mix.

Track cost per ton

Track this by product line, shift, and ton sold. Use tons produced, electricity per ton, labor hours per ton, downtime, and saleable yield to forecast gross margin and cash. If one grade needs more power or more hands, price it for that load or cut its volume.

- Measure power use by ton.

- Review labor by shift and grade.

- Cut downtime before adding headcount.

- Match staffing to furnace uptime.

What this estimate hides: a plant can look busy and still under-earn if energy spikes or crews are oversized. If electricity, labor, or stoppages drift up, owner pay falls first through lower operating profit, then through tighter cash available for draws.

4

Maintenance downtime and capex reserves

Maintenance Downtime and Capex Reserves

Maintenance can drain owner cash even when accounting profit looks fine. In this steel plant, maintenance overhead is 12% of revenue, or about $436M in Year 1 and $1.039B in Year 5. Listed maintenance technician salaries are $640,000 in Year 1 and $128M in Year 5, so the cash burden grows fast with scale.

This driver includes planned outages, unplanned failures, safety shutdowns, and equipment replacement. The key inputs are maintenance expense, repair capex, outage hours, and the cash reserve kept for major work. One line says it all: profit is not cash. If downtime cuts output or delays replacement, owner distributions can shrink or stop.

Fund the reserve before you pay yourself

Track maintenance as % of revenue, plus outage hours and emergency repair spend. Separate routine maintenance from repair capex so the plant does not hide big cash needs in operating costs. If the plant is running near full load, even a short shutdown can hit saleable tons and push back owner draws.

- Budget cash for planned outages.

- Log unplanned stops by cause.

- Fund replacement parts early.

- Hold back cash before distrib utions.

Use a monthly reserve target tied to the 12% maintenance load and the next major overhaul. If the reserve is thin, the next safety shutdown or equipment swap can force a cut in pay, even with strong reported earnings.

5

Debt service, working capital, and reinvestment

Debt, Cash Timing, and Owner Pay

Steel plants are capital-intensive and inventory-heavy, so cash can lag profit. With $2,794M of Year 1 pre-debt operating profit, the plant still has to fund inventory, receivables, raw material buys, taxes, reserves, and reinvestment. Debt service is not provided, so operating profit is not distributable income. The cash conversion cycle is just how long cash sits in stock and customer bills.

If customer terms stretch or raw material purchases rise before sales cash comes in, owner draws fall even when profit looks strong. Retained earnings matter because they protect the plant during steel price swings, lender covenant pressure, and planned repairs. The real question is not profit alone; it is how much cash stays free after the plant stays funded and safe.

Track the cash trap before paying owners

Measure working capital every month: inventory, receivables, supplier payables, and minimum cash. Tie those needs to raw material buys and customer payment terms, then cap owner distributions after financing, taxes, reserves, and reinvestment. If stock builds faster than tons sold, cash gets stuck and the owner draw shrinks.

- Inventory days: track raw, work-in-process, finished stock.

- Receivable days: collect faster than cash goes out.

- Reserve cash: fund repairs before distributions.

- Covenants: keep leverage and cash headroom safe.

6

Compare steel plant owner income scenarios

Owner income scenarios

Owner income swings with tonnage, product mix, pricing, and the heavy fixed plant base. The low, base, and high cases show how much cash stays above debt, taxes, and reserves.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the early ramp case, where owner take-home stays well below operating profit. | This is the modeled steady case, with owner take-home still below operating profit. | This is the stronger earnings case, with owner take-home still below operating profit. |

| Typical setup | 430,000 tons, $3.630B revenue, about $704 gross margin per ton, and $2.794B pre-debt operating profit before debt, taxes, and reserves. | 675,000 tons, $6.463B revenue, about $806 gross margin per ton, and $5.112B pre-debt operating profit before debt, taxes, and reserves. | 840,000 tons, $8.655B revenue, about $874 gross margin per ton, and $6.978B pre-debt operating profit before debt, taxes, and reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Under $2.794BLow Case | Under $5.112BBase Case | Under $6.978BHigh Case |

| Best fit | Use this to test early ramp risk and cash pressure before the plant is fully loaded. | Use this as the main planning case for budgets, lenders, and covenant checks. | Use this to test upside if the plant reaches full use and pricing holds. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Owner take-home will sit below operating profit once debt, taxes, and reserves are set.

Related Products

- Steel Plant Porter's Five Forces Analysis

- Steel Plant BCG Matrix

- Steel Plant Business Model Canvas

- 7 Critical KPIs to Measure Steel Plant Performance

- Steel Plant Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Steel Plant Profitability and Boost Margins

- Quantifying Steel Plant Running Costs: A 2026 Financial Breakdown

- Steel Plant Startup Costs for a 430,000-Unit Year 1 Plan

- Steel Plant Financial Model Template in Excel

- Start a US Steel Plant: 24–48+ Month Launch Roadmap

- How to Write a Steel Plant Business Plan in 7 Actionable Steps

- Steel Plant Marketing Mix

- Steel Plant Marketing Plan

- Steel Plant Business Proposal

- Steel Plant PESTEL Analysis

- Steel Plant Pitch Deck Example Editable PPTX

- Steel Plant Business SWOT Analysis

- Steel Plant Value Proposition Canvas

Frequently Asked Questions

The researched assumptions show $3630M in Year 1 revenue and $8655M by Year 5 Output rises from 430,000 tons to 840,000 tons over the model period Revenue is not owner income, because unit costs, overhead, logistics, commissions, wages, debt, taxes, and reserves come first