Time to Open8-16 weeksLaunch runway

Time to Open8-16 weeksLaunch runwayHow to Open a Supplemental Health Insurance Agency in 8 to 16 Weeks

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Time to Open8-16 weeksLaunch runway  Launch Sequence8 stagesCompliance first

Launch Sequence8 stagesCompliance first Key BottleneckLicense gateState rules

Key BottleneckLicense gateState rules First Revenue StepFirst policyCarrier approval

First Revenue StepFirst policyCarrier approval

Key Takeaways

- Licensing and compliance must clear before any sales.

- Carrier appointments unlock product fit and faster applications.

- CRM and enrollment tools reduce dropped leads.

- Runway depends on commissions, cancellations, and CAC.

Time to Open8-16 weeksLaunch runwayLaunch Sequence8 stagesCompliance firstKey BottleneckLicense gateState rulesFirst Revenue StepFirst policyCarrier approvalLaunch timeline

Short web summary of the launch plan for a supplemental health insurance agency; the XLSX export holds the detailed Gantt chart.

Launch scheduleWeek 1Week 2Week 3Week 4Week 5Week 6Week 7Week 8Week 9Week 10Week 11Week 12

Licensing and compliance

- License filing

- Background checks

- Disclosure review

- E&O coverage

- Approval packet

Carrier contracting

- Carrier outreach

- Appointment packets

- Contract review

- Product training

- Workflow signoff

Systems setup

- CRM setup

- Quote build

- E-app build

- Commission tracking

- System testing

Sales marketing

- Messaging draft

- Audience list

- Lead channels

- Sales scripts

- Campaign launch

Onboarding ops

- Intake forms

- Application QA

- Welcome sequence

- First onboarding

- Support playbook

Finance planning

- Budget baseline

- Cash runway

- Commission model

- Payout controls

- Breakeven review

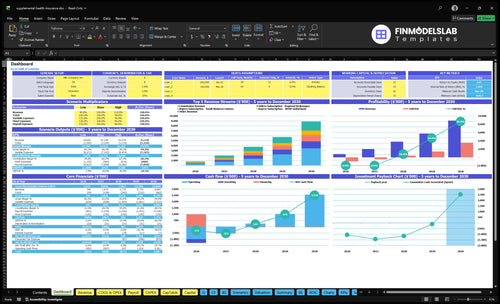

Do your launch assumptions survive the model?

The screenshot in the Supplemental Health Insurance Agency Financial Model Template shows revenue, costs, cash needs, assumptions, and break-even logic—open the model.

Financial model highlights

- $400,000 Year 1 buyer spend

- 5,000 buyers at $80 CAC

- $150,000 Year 1 seller spend

- 300 sellers at $500 CAC

- $5 plus 15% commission

- 50/40/10 buyer mix

- Runway to break-even

- Use dashboard and assumptions tabs

- Scenario sensitivity charts

How long does it take to get carrier appointments?

For a Supplemental Health Insurance Agency, carrier appointments usually take 8 to 16 weeks from the start of licensing to quoting access. The usual order is license first, then E&O proof, then carrier contracting, then product certification. Paid marketing should wait until you can legally quote, disclose, apply, and track policies.

Typical timing path

- 8 to 16 weeks is common

- Start with the active producer license

- Then file E&O proof

- Finish carrier contracting and certification

What slows it down

- Incomplete paperwork adds delay

- Missing entity licensing slows approval

- Background checks can run long

- Weak carrier fit can stall onboarding

What mistakes should I avoid when starting a supplemental insurance agency?

The big mistake is opening a Supplemental Health Insurance Agency before you’re licensed, appointed, trained, and covered. A safer start is simple: licensed, appointed, tracked, and financially tested, because Year 1 can carry $80 buyer CAC, $500 seller CAC, $5 fixed commission, and 15% variable commission. E&O (errors and omissions insurance) matters too, because one bad quote or missing disclosure can turn into a costly claim.

Do this first

- Get licensed before marketing.

- Confirm appointment access before quoting.

- Carry E&O from day one.

- Use trained scripts and full disclosures.

Avoid these traps

- Do not hide exclusions.

- Do not buy leads without consent proof.

- Do not assume instant commissions.

- Match carriers to gig workers, HDHP buyers, and small business owners.

How do supplemental insurance agencies get clients?

The Supplemental Health Insurance Agency gets first clients through referrals, employer benefit conversations, local professional networks, broker partnerships, compliant digital leads, community education, and cross-sell offers; the first revenue comes from compliant lead handling, needs-based sales, application submission, and carrier approval. For tracking, see What Are The 5 KPI Metrics For Supplemental Health Insurance Agency Business?; a Year 1 plan with $400,000 in marketing at $80 CAC targets about 5,000 buyers, with 50% gig workers, 40% HDHP individuals, and 10% small business owners.

Early client sources

- Ask for referrals after approval

- Use employer benefit talks

- Join local professional networks

- Work broker partnerships

Revenue and tracking

- Sell with needs-based conversations

- Submit complete applications fast

- Track source and consent

- Track follow-up and commission

Confirm what must work before selling policies

Launch readiness checklist

Use this go-live approval checklist before opening to confirm the agency is licensed, appointed, insured, trained, and ready to sell.

Licensing

- Entity formed and activeCritical

The agency needs a legal entity before licensing, banking, and contracts can move ahead.

- Resident producer license activeCritical

A resident producer license is the base requirement before any sales activity starts.

- Nonresident states mappedHigh

Map every selling state first so nonresident licenses do not block launch.

Carrier setup

- Carrier appointments securedCritical

Without carrier appointments, the team cannot submit policies or earn commission.

- Product training completedHigh

Agents must know plan rules, exclusions, and fit limits before talking to buyers.

- Rate and commission files loadedHigh

Correct rates and commission terms prevent bad quotes and payment errors at launch.

Compliance

- E&O insurance boundCritical

Errors and omissions coverage protects the agency if advice or paperwork goes wrong.

- Required disclosures approvedCritical

Disclosures must be ready before any quote, call, or application goes live.

- Call and email rules setHigh

Call and email rules reduce consent, recording, and marketing violations.

Systems

- CRM fully configuredHigh

A CRM keeps leads, quotes, and follow-up in one place for day one control.

- Quote and e-application testedCritical

The quote and e-application flow must work before the first live buyer arrives.

- Commission tracking verifiedHigh

Commission tracking must match carrier terms so revenue is recorded correctly.

Sales

- Buyer lead sources taggedHigh

Lead source tracking shows which channels support the Year 1 buyer CAC of $80.

- Seller acquisition paths setHigh

Seller outreach must fit the Year 1 seller CAC of $500 and $150,000 budget.

- First revenue script approvedHigh

A clear first-sale script helps the team quote, close, and submit cleanly.

Finance

- Banking and payouts readyCritical

Banking must be live so premium flows, commissions, and payouts can settle.

- Year 1 cash plan reviewedCritical

Year 1 spend is heavy, with $400,000 buyer marketing and $150,000 seller marketing.

- Go-live signoff completeCritical

Ready means licensed, appointed, trained, insured, trackable, and able to submit applications.

Which launch drivers matter most?

1Licensing

DOI gateKeeps first quotes legal and lowers regulatory risk before the first sale.

2Carrier Access

Product fitUnlocks product fit across gig, HDHP, and small business buyers.

3Enrollment Flow

Week 1Cuts dropped leads and speeds the first commission posts after submission.

4Lead Gen

$80 CACBuilds a measurable path from lead to approved policy at $80 CAC.

5Sales Team

Licensed repsKeeps first sales compliant as licensed producers and setters scale.

6Cash Runway

Month 28Helps the agency absorb slow commission ramps, marketing spend, and early losses.

Licensing and compliance readiness

Licensing readiness

If you cannot clear licensing and state approval, you cannot legally open. For a supplemental health insurance agency, that means the resident producer license, health line of authority, agency entity registration, entity license where required, E&O coverage, disclosures, appointment rules, call and email compliance, and continuing education tracking all need to be ready before the first quote goes out.

The hard dependency is state DOI approval before sales. A delayed background check or missing nonresident license can block appointment access, so a founder may have to wait before quoting HDHP individuals. One missing approval can turn a planned launch into a stalled one.

Lock approvals before marketing

Before launch, verify each license by state, assign one owner for every filing, and track due dates in one checklist. Keep carrier appointment proof, E&O certificates, disclosure templates, and CE tracking in the same file so sales can start cleanly on day one.

- Confirm resident license status.

- Check nonresident license needs.

- Save E&O and disclosures.

- Test call and email scripts.

- Track continuing education deadlines.

Do not let unapproved outreach start early. If the compliance file is complete before marketing begins, the agency can open safely, take first sales, and avoid a stop-start launch when a license, disclosure, or appointment check comes up.

1

Carrier appointments and product portfolio

Carrier Appointments and Product Fit

For a supplemental health insurance agency, carrier appointments are the gate to day-one sales. You need contracted access to accident, critical illness, hospital indemnity, and related products, plus active license and E&O proof, before you can quote or submit business. If carrier approval slips, launch slips with it.

The risk is not just timing. A weak product mix can miss the Year 1 buyer mix of 50% gig economy workers, 40% HDHP individuals, and 10% small business owners. That means product fit, underwriting rules, and quoting access have to match the customer base or first applications will be slow and conversions will be poor.

Verify Appointments Before Launch

Lock the setup in this order: carrier contracting, commission schedule review, product training, underwriting rule review, and quoting access. No appointment means no sale, so confirm every carrier is approved before opening campaigns or training staff to sell.

- Confirm active license and E&O proof

- Match products to buyer mix

- Test quoting access before launch

- Document carrier rules and commissions

What this setup hides: a product mismatch can waste leads fast. If a plan does not fit gig workers, HDHP buyers, or small business owners, the first applications may still come in, but the approval rate and customer experience will drop right at opening.

2

Sales technology and enrollment workflow

CRM and Enrollment Flow

If the CRM and enrollment path are not live on opening day, every new lead can stall after the first call. This workflow must handle lead capture, consent, needs analysis, quoting, e-signature, e-application submission, policy status, renewals, and commission reconciliation, because the model depends on carrier tool access after appointment. A broken handoff means lost leads, missed follow-up, and slower first revenue.

At a $5 fixed commission + 15% model, even a small drop in completed applications hurts cash flow fast, so the team needs clean source tracking and a clear path from quote to paid policy. That’s what gives cleaner onboarding, fewer dropped applications, and faster first revenue.

Prelaunch Setup Check

Use one CRM with fields for source, consent, product fit, quote, application status, renewal date, and commission status. Build the pipeline stages and disclosure templates before the first lead comes in. Then test a full sample case: capture lead, send disclosures, quote, e-sign, submit, and confirm the commission report ties out.

- Map every lead source.

- Log consent before outreach.

- Use an application checklist.

- Track status after submission.

- Reconcile commissions weekly.

3

Lead generation and distribution channels

Compliant Lead Sources

This channel decides whether you have buyers on day one. For supplemental health insurance, you need compliant sources ready before active campaigns: referrals, employer groups, local networks, broker partners, educational content, and small paid tests. The risk is simple: without legal ability to sell and a clear path from lead to application to approved policy, you may open with traffic but no revenue, or worse, with leads you cannot lawfully convert.

Build the Funnel First

Track every source, get consent on the first touch, and use one follow-up cadence. Build landing pages, referral scripts, and disclosure review before launch so each lead can be routed fast and documented. Here’s the quick math: Year 1 marketing is $400,000 at $80 CAC, or about 5,000 buyers; if lead quality slips, that spend turns into noise, not openings.

- Capture consent before outreach.

- Tag every lead source.

- Test small paid channels first.

- Set follow-up within one day.

4

Staffing, training, and sales process

Founder-Led Sales First

At launch, the fastest path is to have the founder handle sales so the agency can open while scripts, disclosures, and follow-up rules are being tightened. This matters because anyone who sells or advises must be licensed, and unlicensed staff crossing into sales activity can block day-one readiness and create compliance risk.

One clean rule: if the role touches product advice, it needs a license and documented training. Build the first workflow around suitability questions, objection handling, call notes, handoff rules, and quality review so the team can add capacity without drifting outside the lines.

Train, Document, Then Scale

Before opening, verify the sales script, compliant disclosures, and handoff steps are written and tested. The founder should be able to sell first, then add licensed producers or appointment setters only after the process shows no gaps in needs-based questions, call notes, and review checks.

- Lock licensing before sales

- Document disclosures and notes

- Test handoffs before adding staff

- Review every early call

For a broader model, use the Year 1 seller mix of 70% independent agents, 20% boutique agencies, and 10% regional brokerages. That mix gives controlled capacity, but only if training stays tight and unlicensed staff never drift into selling or advising.

5

Commission ramp and cash runway

Commission Ramp and Cash Runway

Cash gets tight fast when commissions are small, paid late, or reversed. With a $5 fixed commission plus 15% of order value, a gig buyer at $45 yields $11.75, an HDHP buyer at $65 yields $14.75, and a small business buyer at $250 yields $42.50.

That means launch timing depends on more than sales volume. You need a monthly forecast that separates approved policies, paid commissions, cancellations, and chargebacks, so marketing spend and software costs do not outrun cash before day one is stable.

Run the cash model before opening

Track each policy from lead to approval to commission paid. A simple blended mix of 50% gig workers, 40% HDHP individuals, and 10% small business owners points to a rough commission of $16.03 per policy before reversals, so runway math must assume some lag and some fallout.

Stress-test the first 60 to 90 days with retention assumptions, policy approval timing, and chargebacks. The disclosed repeat order assumptions of 105, 102, and 110 should sit in the forecast, along with CAC tracking and software fees, so the team knows when cash turns positive instead of guessing.

- Map commission timing by carrier.

- Set monthly CAC and refund limits.

- Review breakeven sensitivity every month.

6

Related Products

- Supplemental Health Insurance Agency Porter's Five Forces Analysis

- Supplemental Health Insurance Agency BCG Matrix

- Supplemental Health Insurance Agency Business Model Canvas

- What Are The 5 KPI Metrics For Supplemental Health Insurance Agency Business?

- Supplemental Health Insurance Agency Business Plan Template in Pre-Written Word

- How Increase Supplemental Health Insurance Agency Profits?

- What Are Operating Costs For Supplemental Health Insurance Agency?

- Supplemental Health Insurance Agency Startup Costs: $550K Year 1 Plan

- Supplemental Health Insurance Financial Model Template in Excel

- Supplemental Health Insurance Agency Owner Income: $101M Revenue Case

- How To Write A Business Plan For Supplemental Health Insurance Agency?

- Supplemental Health Insurance Agency Marketing Mix

- Supplemental Health Insurance Agency Marketing Plan

- Supplemental Health Insurance Agency Business Proposal

- Supplemental Health Insurance Agency PESTEL Analysis

- Supplemental Health Insurance Agency Pitch Deck Example Editable PPTX

- Supplemental Health Insurance Agency Business SWOT Analysis

- Supplemental Health Insurance Agency Value Proposition Canvas

Frequently Asked Questions

Start with licensing, not marketing Get the right resident producer license, confirm any agency entity license with your state DOI, buy E&O coverage, and apply for carrier appointments Then set up CRM, quoting, e-application, disclosures, and commission tracking A realistic launch window is 8 to 16 weeks if paperwork and appointments move cleanly