Supplemental Health Insurance Agency Startup Costs: $550K Year 1 Plan

You’re budgeting for a regulated agency before commissions and renewals are steady, so CAPEX alone is too narrow This startup cost guide uses researched planning assumptions, including $550,000 in Year 1 acquisition spend, $14,000 per month in listed fixed overhead, and a first operating year model for launch funding The goal is to size CAPEX, pre-opening expenses, working capital, and the cash runway needed to open and sell legally in the United States

Supplemental Insurance Agency CAPEX Calculator Objective

Startup CAPEX Calculator

Estimates one-time capitalized startup assets only for a supplemental health insurance agency, separate from pre-opening expenses and cash reserve.

Exclude non-CAPEX funding This calculator covers one-time capitalized startup assets only. It excludes payroll runway, rent runway, deposits, licensing renewals, launch marketing, SaaS subscriptions, working capital, owner draws, and debt service. The $6,500 monthly office rent belongs in pre-opening runway or working capital unless it funds fixed improvements.

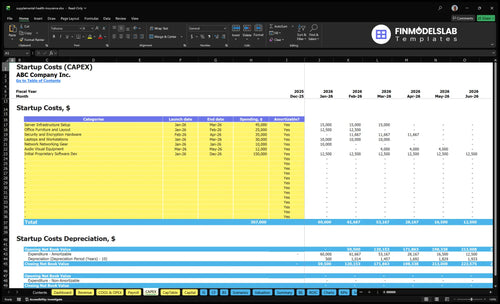

What should this screenshot show?

This screenshot shows CAPEX and startup costs; open the template and check categories, launch timing, costs, depreciation/amortization.

Screenshot highlights

- One-time vs recurring costs

- Month 1 launch timing

- Runway and commission ramp

How much money do I need to start a supplemental insurance agency?

For a Supplemental Health Insurance Agency, the documented startup budget is at least $718,000 for Year 1: $550,000 for acquisition plus $168,000 in fixed overhead at $14,000/month. That excludes software subscriptions, payroll, owner draw, debt service, and CAPEX because those amounts aren’t specified; for profit planning, see How Increase Supplemental Health Insurance Agency Profits?.

Budget items

- $400,000 buyer marketing spend

- $150,000 seller marketing spend

- $14,000/month fixed overhead

- Legal, licensing, rent, research

Acquisition math

- $400,000 ÷ $80 CAC = 5,000 buyers

- $150,000 ÷ $500 CAC = 300 sellers

- Fund producer licensing readiness

- Keep working capital for timing gaps

What are the biggest startup costs for a supplemental insurance agency?

Biggest startup costs for a Supplemental Health Insurance Agency are lead generation, seller acquisition, licensing and compliance, CRM setup, and carrier appointments. In Year 1, buyer marketing is the biggest researched launch cost at $400,000, and seller marketing is next at $150,000, using CAC assumptions of $80 per buyer and $500 per seller. Add fixed overhead like $6,500 rent, $4,000 legal counsel, $2,000 licensing fees, and $1,500 market research per month.

Launch costs

- $400,000 buyer marketing

- $150,000 seller marketing

- $80 CAC per buyer

- $500 CAC per seller

Run-rate costs

- $6,500 monthly office rent

- $4,000 legal counsel monthly

- 60% agent support and training

- 45% cloud hosting and security

40% of variable cost goes to lead verification, so quality control matters fast. 30% of COGS is payment gateway fees, and office versus remote setup changes how hard the first year hits cash.

What hidden costs should I budget for before insurance commissions start?

Before commissions start, budget for the cash gap: appointment delays, background checks, producer onboarding, E&O insurance, compliance docs, secure records handling, CRM onboarding, lead testing, training time, and owner living costs. For the Supplemental Health Insurance Agency, the commission model uses a $5 fixed fee plus 15% of order value, and the provided Year 1 mix implies a $7,350 average order and about $1,603 commission per order before timing and servicing costs; What Are The 5 KPI Metrics For Supplemental Health Insurance Agency Business? shows the KPIs that track this lag. With Year 1 repeat orders of 105, 102, and 110 by segment, you still need working capital before cash turns on.

Pre-open cash

- Separate launch costs from monthly ops.

- Budget for background checks and onboarding.

- Include compliance docs and secure records.

- Hold cash for owner living costs.

Year 1 order math

- 50% gig economy workers.

- 40% high-deductible health plan individuals.

- 10% small business owners.

- $7,350 weighted average order value.

Cash lag risks

- Commission timing can lag revenue.

- Lead testing happens before payouts.

- Training time adds unpaid hours.

- CRM onboarding creates upfront spend.

Keep tracking

- $1,603 commission per order.

- 105, 102, and 110 repeat orders.

- Servicing costs still hit cash flow.

- Owner pay should stay separate.

Supplemental Health Insurance Agency Startup Cost Summary Table

Startup cost summary

Shows startup asset costs and the separate cash reserve needed before breakeven for this agency.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Server Infrastructure Setup | $45,000 | Core platform setup and hosting-ready infrastructure | Yes |

| Office Furniture and Layout | $25,000 | Workstations, furniture, and basic office buildout | Yes |

| Security and Encryption Hardware | $35,000 | Secure hardware for protected customer data handling | Yes |

| Laptops and Workstations | $30,000 | Staff computers and producer setup equipment | Yes |

| Initial Proprietary Software Development | $150,000 | Custom software, workflow automation, and launch configuration | Yes |

| Operating Reserve | $929,000 | Cash runway needed through month 28 breakeven | No |

Supplemental Health Insurance Agency Core Five Startup Costs

Licensing, Compliance, and Carrier Appointment Startup Expense

Licensing setup

Month 1 should carry $2,000 for insurance licensing fees and $4,000 for professional legal counsel. That covers entity formation, state insurance department filings, producer licenses, background checks, continuing education setup, compliance documents, secure record rules, and legal review. Costs vary by state, license type, and producer count.

What drives the bill

Here’s the quick math: pricing depends on target states × license types × number of producers × carrier requirements. Add separate work for appointment packets, proof of E&O, background checks, and compliance forms. Carrier appointment readiness is not just a fee; it is a timing and document load that can delay sales if the file is incomplete.

How to keep it tight

Start with the fewest states and product lines that still support launch. Keep one clean document set, one secure record policy, and one owner for filings so nothing gets lost. The fastest way to overspend is adding carriers before the agency can pass their appointment checks. One clean stack beats three messy ones.

Pricing questions

To price this correctly, confirm how many licensed producers, which states, which product lines, how many carriers, and whether the agency uses employee producers, independent producers, or both. Those five inputs decide the real setup load and the pace of carrier appointments.

Software, CRM, and Operating Platform Startup Expense

Setup Buildout

CAPEX here is the one-time platform build: CRM, agency management system, quoting and enrollment tools, VoIP, email, e-signature, website forms, secure document workflows, permission roles, compliance logging, and integrations. Price it from vendor quotes for onboarding fees, form buildout, data migration, and setup hours. Keep this separate from monthly SaaS, which should sit in operating expense.

Monthly SaaS

The recurring stack covers subscriptions for CRM access, call tools, e-signature, storage, and user seats. The research context does not provide a fixed software subscription dollar amount, so don’t invent one. Build the estimate from the number of users, modules, and months of coverage, then add separate lines for onboarding and any annual minimums.

Cloud and Security

Model Year 1 cloud hosting and security at 45% of revenue. That line should cover cloud hosting, secure data storage, access controls, and cybersecurity tools. Here’s the quick math: if revenue changes, this cost moves with it, so it is not a fixed setup fee. Ask vendors for storage limits, user counts, and security scope before you lock the budget.

Payments and Controls

Payment gateway setup needs both launch work and ongoing fee tracking. The research context sets payment gateway transaction fees at 30% of revenue, so keep those out of setup and book them as variable operating cost. What this estimate hides: the final bill depends on payment volume, gateway terms, fraud controls, and how many workflows need compliance logging.

Office, Equipment, and Physical Setup Startup Expense

Launch Layout

A remote launch can keep overhead low, but a hybrid or client-facing office needs more than desks. Budget for computers, monitors, phones or headsets, and secure file handling. If you lease space, the source rent is $6,500 per month starting in Month 1. That rent, plus deposits, is usually working capital unless it funds leasehold improvements.

Cost Build

This cost covers the setup to work and meet clients: desks, chairs, printer or scanner, signage, locked records storage, and any leasehold improvements. Estimate it with quotes for each item plus office size and months of rent runway (cash reserved to cover rent). Put lease deposits and pre-opening rent in working capital unless they are tied to fixed assets.

- Price each desk and chair.

- Quote storage and sign costs.

- Add deposit and rent months.

Keep It Lean

A remote model can save on rent and signage, but it still needs compliant workflows, secure systems, and dependable call tools. The common mistake is underbuying storage or document controls when physical records must be kept on site. Keep the office lean until producer count, walk-in traffic, and retention rules justify more space.

Sizing Checks

Set this budget by asking five things: office size, producer count, client walk-in needs, state document retention rules, and whether physical records will be stored. If records stay on site, locked storage and handling matter as much as furniture. If not, a remote setup can stay much lighter.

- Count people using the space.

- Test walk-in demand first.

- Confirm record storage rules.

Staffing, Training, and Producer-Readiness Startup Expense

Producer Readiness

This line item covers recruiting licensed producers, appointment setters, and admin support, then training them on product scripts and compliance before commissions land. Based on the research inputs, Year 1 agent support and training equals 60% of revenue, and lead verification adds another 40%. That means this startup cost can consume the first-year revenue base before payout timing turns predictable.

Channel Build

Use separate onboarding plans by channel: independent agents need a lighter script-and-compliance track, while boutique agencies and regional brokerages need deeper process, permission, and reporting setup. The Year 1 seller mix starts at 700% independent agents, 200% boutique agencies, and 100% regional brokerages, so producer-readiness cost should be built by channel, not averaged. Estimate it as producer count × hours × cost per producer.

Cash Discipline

Keep pre-opening recruiting and training separate from ongoing salaries, benefits, and sales commissions, or runway gets blurry fast. A lean start uses staggered hiring, remote onboarding, and one compliance script set for all sellers, then adds channel-specific modules only where needed. The main mistake is paying full payroll before commissions are predictable.

Runway Need

Working capital is the cash cushion for payroll, training, and lead verification before commission receipts normalize. With spend modeled at 60% of revenue for agent support and training plus 40% for lead verification, the first-year cash burden tied to seller readiness and lead quality equals 100% of revenue.

Launch Marketing and Lead Generation Startup Expense

Launch scope

Launch spend her e is the visibility test, not a promise of sales. It covers website, landing pages, local search setup, referral materials, employer outreach, community marketing, review setup, paid leads, lead verification, and launch campaigns. The case sets Year 1 buyer marketing at $400,000 and seller marketing at $150,000.

Buyer budget

Estimate the buyer side from the target mix and acquisition cost. The research case lists 500% gig economy workers, 400% high-deductible health plan individuals, and 100% small business owners, with $80 per buyer. Here’s the quick math: buyer count × $80, then layer in site, forms, and lead tools. That feeds the $400,000 Year 1 buyer line.

Seller budget

Seller spend should track channel proof, not guesses. The case uses $500 per seller, plus $25 in ads or promotion fees per seller in Year 1. Start with small tests for independent agents, boutique agencies, and regional brokerages, then widen only after lead quality holds. That keeps the $150,000 seller budget tied to verified demand.

Lead quality

Lead verification sits at 40% of revenue, so weak leads can squeeze margin fast. Build review setup, call tracking, and a simple verification flow before scaling paid leads. The seller mix is recorded as 700% independent agents, 200% boutique agencies, and 100% regional brokerages, so each source needs its own follow-up script.

Lean, Base, and Full Supplemental Insurance Agency Startup Cost Scenarios

Launch cost scenarios

Lighter launches keep cash needs lower, but this model still carries licensing, compliance, and lead-test costs. Bigger producer teams and fuller office setups raise both spend and working capital.

| Scenario | Lean LaunchLower cash need | Base LaunchModel-aligned | Full LaunchHigher capital |

|---|---|---|---|

| Launch model | Remote-first or very small office with 1-2 producers and a tight software stack. | This matches the Year 1 plan with a standard office setup, 2-4 producers, and the current acquisition budget. | This is a larger launch with a real office presence, 4-8 producers, and deeper software. |

| Typical setup | Keep licensing, compliance, and lead testing in place, then add only the tools needed to sell and service policies. | Use a normal office, standard carrier appointments, a full compliance stack, and a steady marketing plan. | Assume broader carrier appointments, more support staff, and a larger working capital cushion. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $450,000 - $800,000Tighter budget | $900,000 - $1,300,000Base plan | $1,500,000 - $2,200,000Capital heavy |

| Best fit | Best for founders testing demand with a small footprint, but cash still needs room for licensing, compliance, and early lead tests. | Best for operators who want to follow the provided Year 1 build and fund the first ramp without stretching cash too thin. | Best for teams that want faster scale and wider carrier coverage, but the cash load rises fast and payback still takes time. |

Planning note: These scenario ranges are researched planning assumptions, not exact quotes.

Related Products

- Supplemental Health Insurance Agency Porter's Five Forces Analysis

- Supplemental Health Insurance Agency BCG Matrix

- Supplemental Health Insurance Agency Business Model Canvas

- What Are The 5 KPI Metrics For Supplemental Health Insurance Agency Business?

- Supplemental Health Insurance Agency Business Plan Template in Pre-Written Word

- How Increase Supplemental Health Insurance Agency Profits?

- What Are Operating Costs For Supplemental Health Insurance Agency?

- Supplemental Health Insurance Financial Model Template in Excel

- Supplemental Health Insurance Agency Owner Income: $101M Revenue Case

- How to Open a Supplemental Health Insurance Agency in 8 to 16 Weeks

- How To Write A Business Plan For Supplemental Health Insurance Agency?

- Supplemental Health Insurance Agency Marketing Mix

- Supplemental Health Insurance Agency Marketing Plan

- Supplemental Health Insurance Agency Business Proposal

- Supplemental Health Insurance Agency PESTEL Analysis

- Supplemental Health Insurance Agency Pitch Deck Example Editable PPTX

- Supplemental Health Insurance Agency Business SWOT Analysis

- Supplemental Health Insurance Agency Value Proposition Canvas

Frequently Asked Questions

Budget around the researched Year 1 plan of $550,000 for acquisition if you’re building both buyer and seller channels That includes $400,000 for buyer acquisition at an $80 CAC and $150,000 for seller acquisition at a $500 CAC Treat this as a testing and ramp budget, not a guarantee of policies sold