Owner income$85k-$1.47M

Owner income$85k-$1.47MHow Much Does A Tea Lounge Owner Make With $85K Year 1 EBITDA?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$85k-$1.47M  Net margin8%-42%

Net margin8%-42% Revenue for target pay$1.09M

Revenue for target pay$1.09M Business difficultyHard

Business difficultyHard

Key Takeaways

- Traffic drives revenue; Monday starts at 10 covers.

- Average ticket lifts sales without adding seats.

- Margin improves as drink and food COGS fall.

- Fixed costs and payroll shape break-even, not just sales.

Owner income$85k-$1.47MNet margin8%-42%Revenue for target pay$1.09MBusiness difficultyHardWant to test your tea lounge owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want to check Tea Lounge owner income in the model?

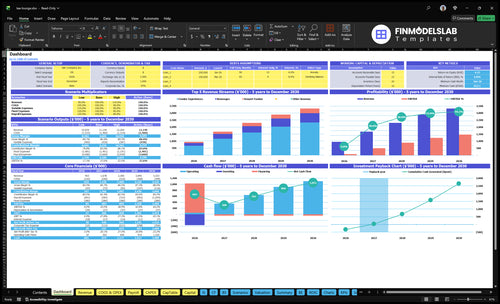

Yes — the Tea Lounge Financial Model Template shows revenue, EBITDA, breakeven, cash need, and owner pay scenarios in one view. Open the model to see the full owner-income picture.

Owner-income model highlights

- Month 4 breakeven

- Month 6 cash: $622k

- 24-month payback case

- Capex: $365k upfront

- Low, base, high traffic

How much revenue does a tea lounge need to pay the owner?

A Tea Lounge needs about $650k/month in Year 1 revenue just to reach operating break-even before owner pay; to pay the owner, add the monthly draw, reserves, and debt service on top. For KPI context, track the revenue driver behind this target here: What Is The Most Important Metric To Measure The Success Of Tea Lounge?

Break-even math

- Fixed expenses: $233.5k/month

- Payroll: $290k/month

- Fixed-plus-labor load: $523k/month

- Contribution after costs: 80.5%

Owner pay target

- Break-even: $523k / 80.5% = ~$650k

- Add owner draw above break-even

- Add reserves above break-even

- Add debt service above break-even

How does the owner’s role change tea lounge income?

If the owner runs the Tea Lounge, income can look higher because the owner is covering the $75k general manager job, but that is paid labor, not extra profit. A manager-run model protects owner time, yet it keeps payroll higher across service, kitchen, host, beverage, and management roles. Add-ons like extended hours, reservations, classes, memberships, wholesale tea, and a second location can raise income, but they also add scheduling, training, inventory, and cash complexity.

Owner-operated income

- $75k can be owner labor.

- Not all of it is profit.

- Owner saves payroll cash.

- Owner works in the business.

Manager-run growth

- Protects owner time.

- Keeps payroll higher.

- Adds income from new offers.

- Adds scheduling and cash complexity.

Is a tea lounge profitable?

Yes—Tea Lounge can be profitable if covers, ticket size, and staffing line up; the model reaches Month 4 breakeven. It shows EBITDA of $85k, $503k, $894k, $1238M, and $1469M across Years 1-5, with gross margin improving as COGS fall from 150% to 120% and beverage mix rises from 200% to 250%. The main limits are seating, service time, and payroll.

Profit drivers

- Month 4 breakeven supports the case.

- Covers drive top-line volume.

- Ticket size lifts revenue per guest.

- Beverage mix helps margins.

Main limits

- Seating caps peak revenue.

- Service time slows table turns.

- Payroll can squeeze EBITDA.

- COGS must keep falling.

Want the six main tea lounge income drivers?

1

265-680/wkCustomer Traffic

More covers spread fixed rent and payroll over more sales, so EBITDA rises fastest.

2

$65-$105Average Ticket

Higher spend per guest lifts revenue with little extra overhead, especially on busy days.

3

$348K-$815KLabor Scheduling

Payroll climbs as staffing scales, so tight scheduling protects take-home cash.

4

85%-88%Beverage Margin

Stronger drink and food mix keeps more of each sale after ingredient costs.

5

$23.35KOccupancy Cost

Rent and site costs set the breakeven floor, so lower occupancy improves cash flow.

6

UnmodeledAdd-Ons

Extra dessert, retail, or premium upsells can lift income, but they need separate assumptions.

Tea Lounge Core Six Income Drivers

Customer Traffic And Seating Use

Traffic and Seating Use

Traffic drives revenue first. Weekly covers rise from 265 in Year 1 to 680 in Year 5, so more seats filled means more sales before any margin work matters. Saturday is the main cash day, growing from 90 to 200 covers. Monday starts at only 10 covers in Year 1, so a quiet midweek can drag cash flow and make owner pay uneven.

This driver depends on location, atmosphere, hours, neighborhood demand, repeat visits, events, and seating capacity. The core math is simple: covers × average check. If seats sit empty, rent and labor still hit, so profit and take-home pay fall fast even when the menu is strong.

Track Covers by Daypart

Measure covers by day, by hour, and by seat turn. Track Saturday, Sunday, and Monday separately, since the gap from 10 Monday covers to 200 Saturday covers changes staffing, prep, and cash needs. One seat that turns twice on a busy day beats three empty seats all week.

To improve this driver, test hours, events, and reservation blocks before adding fixed cost. Watch repeat-visit rate and fill rate by day. If weekday demand stays soft, trim labor and prep to match it; if weekends sell out, protect seating capacity and speed so you can convert demand into owner profit.

- Track covers by day and hour.

- Match labor to peak traffic.

- Test events on slow days.

- Protect seating on Saturdays.

1

Average Ticket Size

Average Ticket Size

Average ticket, or AOV (average order value), is the dollars each guest spends per visit. In this model, midweek AOV rises from $65 to $85, and weekend AOV rises from $85 to $105. That is a 31% lift midweek and a 24% lift on weekends, without adding seats. Higher ticket size can lift revenue, gross profit, and owner pay if labor and waste stay controlled.

It includes premium tea service, tasting flights, pastries, snacks, packaged tea, and accessories. The risk is simple: if price moves up faster than comfort, service quality, or perceived value, checks stall and cash flow weakens even when traffic holds. Strong ticket growth should come from a better mix, not just a higher menu tag.

Track AOV by daypart

Watch midweek AOV and weekend AOV separately, not as one blended number. Track check size, add-on rate, and menu mix for tea, food, and retail. Revenue is covers × AOV, so the owner should know which upsells raise the ticket without adding much labor, spoilage, or table time.

- Test add-ons on quiet days first.

- Match price to service and room.

- Watch discounts and comps closely.

- Forecast owner pay from gross profit.

If higher tickets need more prep, more touch, or more waste, the cash gain shrinks fast. Keep the service promise tight, because the business only wins when the higher check still leaves room for rent, payroll, and the owner’s draw.

2

Gross Margin On Drinks, Food, And Retail

Gross Margin on Drinks, Food, and Retail

Gross margin is what’s left after direct product costs. In this model, COGS improve from 150% of sales in Year 1 to 120% in Year 5, so every $1 sold still loses $0.50 at first and $0.20 later before overhead. Beverage cost falls from 40% to 30%, and food ingredients from 110% to 90%.

That means the owner’s pay is not set by sales alone. Rent and labor still come out after gross profit, so weak recipe control, premium ingredients, milk, syrups, packaging, spoilage, and pastry waste can shrink take-home income fast. Retail tea should be tracked on its own, because each item has its own cost and margin.

Track COGS and waste weekly

Build a recipe card for every drink, food item, and retail pack, then compare actual cost to menu price each week. Watch milk, syrups, packaging, premium ingredients, spoilage, and pastry waste. The goal is simple: keep beverage cost near 30% and food ingredients near 90% so gross profit can help cover rent and payroll.

- Track cost per item sold.

- Separate drinks, food, retail.

- Log waste by daypart.

- Review margin before payroll.

3

Labor Scheduling And Owner Involvement

Labor Scheduling and Owner Time

Labor is the main controllable swing after traffic. In this model, payroll is $3475k in Year 1, then $490k, $590k, $715k, and $815k through Year 5, so small staffing errors can hit owner pay fast. The real question is whether labor matches rush periods, table turns, prep, and closing work, not just scheduled hours.

Owner shifts can cut cash payroll, but they also add unpaid work and fatigue. Every unpaid hour should be priced against target pay, or the business can look profitable while the owner is underpaid. If midweek demand is light and weekends are busy, the schedule should flex with that pattern so gross profit is not eaten by idle labor.

Track Labor by Daypart

Measure labor against covers, rush windows, prep hours, and close-down time. That tells you whether staffing is tied to demand or just to habit. Here’s the quick test: if labor rises faster than traffic, owner income drops even when sales hold.

Set a weekly schedule that separates service, prep, and cleaning, then compare planned hours to actual hours. If the owner is filling gaps, track those hours at a target wage and build them into the forecast. That keeps the pay picture real and stops “free” owner time from hiding the true cost of running the lounge.

4

Rent And Fixed-Cost Pressure

Fixed-Cost Floor

Using the listed line items, monthly fixed costs are $50,350 before owner pay: $15,000 rent, $3,000 utilities, $12,000 property taxes, $900 insurance, $500 software, $18,000 cleaning, $800 accounting and legal, and $150 music licensing. That is the sales floor the lounge must clear every month before the owner starts taking money home.

This pressure hits hardest when traffic is thin. If Monday opens at 10 covers and Year 1 weekly traffic is only 265 covers, weekends can look fine while the month still falls short. Better locations can add traffic, but higher rent only pays back if seats turn often, tickets stay strong, and repeat demand stays steady.

Track the sales floor

Build the model from covers, average check, hours open, and each fixed cost line. Then test whether added rent brings enough extra sales to cover the gap, not just more foot traffic. One clean rule: if the location does not lift weekday covers, it usually does not lift owner pay.

- Track rent per seat.

- Watch midweek covers closely.

- Forecast fixed costs monthly.

- Protect cleaning and utility spend.

If the site change raises traffic, document the lift by daypart and compare it to the added fixed load. That is the real payback test: more gross profit after fixed costs, with enough left over for the owner’s draw.

5

Events, Classes, And Retail Tea Sales

Add-On Tea Revenue

Add-on revenue comes from tea tasting classes, afternoon reservations, private tea parties, memberships, packaged loose-leaf tea, and workshops. It lifts income beyond walk-in drinks because it can fill slow midweek periods and raise average revenue per guest. The model does not give separate assumptions, so each line needs its own forecast.

Owner income improves when these sales help cover fixed costs like $15k rent and $3k utilities with less reliance on daily covers. The key metric is contribution after direct tea, food, and event labor. One-time promos and recurring memberships should not be mixed together, or cash flow will look stronger than it is.

Measure Each Add-On Separately

Track each line on its own so you can see what really pays. Use new sign-ups, renewals, class bookings, retail units sold, and added labor hours. The simple test is: revenue minus direct cost minus added labor equals true add-on profit.

- Book classes by month

- Separate memberships from promos

- Track retail tea margin

- Log setup and cleanup hours

Use these offers to use empty seats first. In Year 1, Monday starts at only 10 covers, so a paid class or private tea party can spread rent and payroll across more sales. Price each offer to cover product, prep, and cleanup, or owner pay gets squeezed.

6

Compare low, base, and high tea lounge owner income scenarios

Owner income scenarios

Owner income shifts with weekly covers, ticket size, and payroll. This table shows low, base, and high cases before reserves, debt service, and taxes are set.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower owner-income path from Year 1 volume and pricing. | This is the modeled middle path from Year 3 volume and pricing. | This is the stronger owner-income path from Year 5 volume and pricing. |

| Typical setup | Year 1 runs 265 weekly covers at $65-$85 AOV, 15% COGS, and $347.5k payroll, with early revenue still absorbing fixed costs. | Year 3 reaches 520 weekly covers at $75-$95 AOV, 13.5% COGS, and $590k payroll, with a steadier mix across weekdays and weekends. | Year 5 reaches 680 weekly covers at $85-$105 AOV, 12% COGS, and $815k payroll, with stronger weekend demand and better labor spread. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $85k EBITDA-ledYear 1 plan | $894k EBITDA-ledYear 3 plan | $1.469M EBITDA-ledYear 5 upside |

| Best fit | Use this to stress-test opening-year traffic and labor load. | Use this as the core operating case for budgeting and hiring. | Use this to test full-capacity trading and upside cash flow. |

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Tea Lounge Porter's Five Forces Analysis

- Tea Lounge BCG Matrix

- Tea Lounge Business Model Canvas

- 7 Essential KPIs to Maximize Tea Lounge Profitability

- Tea Lounge Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Tea Lounge Profit Margins

- What Are the Monthly Running Costs for a Tea Lounge?

- How Much Does It Cost To Open A Tea Lounge? $622k Cash Plan

- Tea Lounge Financial Model Template in Excel

- How To Open A Tea Lounge In 12–28 Weeks With A Launch Checklist

- How to Write a Tea Lounge Business Plan: 7 Steps to Funding

- Tea Lounge Marketing Mix

- Tea Lounge Marketing Plan

- Tea Lounge Business Proposal

- Tea Lounge PESTEL Analysis

- Tea Lounge Pitch Deck Example Editable PPTX

- Tea Lounge Business SWOT Analysis

- Tea Lounge Value Proposition Canvas

Frequently Asked Questions

A tea lounge owner’s take-home depends on whether they take salary, distributions, or both In this model, EBITDA is $85k in Year 1 and $1469M in Year 5 before taxes, debt service, depreciation, and reserves The owner should not treat all EBITDA as personal cash, especially during ramp-up