Owner income$0-$85k

Owner income$0-$85kHow Much Does a Tradesman Owner Make? $85k Pay vs Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0-$85k  Net margin-586% to 279%

Net margin-586% to 279% Revenue for target pay$422.8k

Revenue for target pay$422.8k Business difficultyHard

Business difficultyHard

You’re planning owner pay before the trade business has proven enough billable work to carry payroll This US-focused guide uses a five-year model with $85,000 planned owner pay, service rates from $85 to $175 per hour, and clear separation between revenue, profit, reserves, taxes, and owner take-home It excludes employee wage benchmarks, tax advice, guaranteed distributions, and location-specific licensing rules

Owner income$0-$85kNet margin-586% to 279%Revenue for target pay$422.8kBusiness difficultyHardCan this tradesman business pay you?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check the owner-income model?

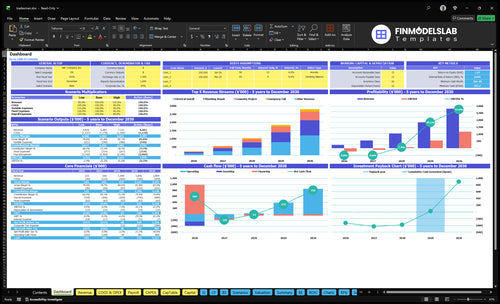

This screenshot shows Tradesman revenue, margin, costs, reserves, and owner take-home assumptions in the Tradesman Financial Model Template; open the model.

Owner-income model highlights

- Owner pay: $85,000 planned

- Year 1 revenue: $38,725

- Charts split EBITDA and reserves

Does a tradesman make more working solo or with a crew?

A Tradesman usually keeps more owner take-home working solo until the crew is fully booked and priced to cover its true costs. Hiring can raise revenue, but this plan adds $190,000 of non-owner payroll in Year 1 and $599,000 by Year 5 before the owner’s $85,000 salary, so track quality and repeat demand with What Is The Current Customer Satisfaction Level For Tradesman?.

Solo wins when

- Owner hours stay billable

- Labor risk stays low

- Callbacks stay owner-controlled

- Revenue cap is acceptable

Crew wins when

- Booked work covers payroll

- Pricing covers workers’ compensation

- Quality control prevents rework

- Vehicles, tools, and scheduling are funded

How can a tradesman increase owner income?

Tradesman can raise owner income by charging better effective rates, filling the calendar, and pushing higher-margin jobs first. In the model, emergency calls run from $150 per hour in Year 1 to $175 in Year 5, while plumbing repair moves from $95 to $110 and electrical install from $105 to $120. Scaling can lift revenue from about $38,725 to $422,813, but payroll and training can cut take-home while you add labor.

Raise the rate

- Book more emergency calls

- Favor higher-rate work

- Cut rework and callbacks

- Keep pricing tight

Grow the load

- Pack more jobs per day

- Add labor after demand

- Use training before scale

- Watch take-home during growth

What expenses reduce tradesman owner income?

The biggest drains on Tradesman owner income are materials, subcontractor overflow, fuel and maintenance, consumables, payroll, and fixed overhead. For startup context, see How Much Does It Cost To Open And Launch Your Tradesman Business? — but the real squeeze is ongoing: materials are tied to 180% of revenue in Year 1 and 150% in Year 5, subcontractor overflow takes 30% then 20%, and payroll rises from $275,000 to $684,000. Fixed overhead runs $5,230 per month, and callbacks and rework should be tracked by job because they turn paid hours into unpaid labor.

Big cost drivers

- Materials: 180% then 150%

- Subcontractors: 30% then 20%

- Fuel and maintenance: 40% then 30%

- Consumables: 25% then 15%

Income pressure points

- Payroll: $275,000 to $684,000

- Overhead: $5,230 each month

- Includes: rent, software, utilities

- Also includes: insurance, licensing, admin

Which drivers matter most?

1

$85-$175/hrPricing Power

Higher hourly rates lift every booked hour, so owner take-home rises fastest when the team can charge near $175 instead of $85.

2

15-50hBillable Utilization

More billable hours per job spread the same crew cost and overhead across more revenue, which leaves more cash for the owner.

3

$275K-$684KLabor Leverage

Payroll can scale from $275K to $684K, so owner income depends on keeping each worker productive; owner pay is not a fixed salary.

4

79%-83%Job Mix

A mix tilted toward higher-margin repair and install work keeps gross margin after materials and subcontractors in the high 70s and low 80s.

5

$5.2K/moCost Control

Holding fixed overhead near $5,230 a month keeps more gross profit from getting eaten before it reaches the owner.

6

$150->$120Repeat Demand

Cutting CAC from $150 to $120 makes each job cheaper to win, and repeat or referral work usually needs less paid marketing.

Tradesman Core Six Income Drivers

Pricing Power

Pricing Power

When the shop raises its effective rate without letting job costs rise, more of each dollar falls to gross profit. In Year 1, modeled rates start at $95 plumbing, $105 electrical, $85 carpentry, and $150 emergency; by Year 5 they reach $110, $120, $100, and $175. That is roughly a 15% to 18% lift before adding more jobs.

Protect the rate card

Track quoted rate, billed rate, and job cost by trade. Minimum service charges, emergency premiums, and tighter estimates should cover specialty, urgency, licensing, travel, and diagnostic time. Here’s the quick math: if a bid misses material waste or gives away drive time, owner pay drops fast because the higher invoice does not turn into higher take-home.

Set prices by job type, not just hours. If the mix shifts toward emergency work, the same crew can earn more with the same fixed overhead. But if fixed bids are too low, margin gets eaten by rework, waste, and callbacks, and pricing power disappears at the cash line.

- Quoted rate vs billed rate

- Minimum service charge

- Emergency premium collected

- Travel and diagnostic time

- Material waste by job

- Callback cost and rework

1

Billable Utilization

Billable Hours That Pay

Billable utilization is the share of owner time that turns into paid work. In this model, jobs can carry 15 emergency hours in Year 1 or 40 carpentry hours, then rise to 18 to 50 hours by Year 5. Unpaid estimates, drive time, supply runs, admin, cancellations, permit waits, and seasonal slowdowns all cut take-home income, because hours worked do not equal hours billed.

Schedule density matters too. Two nearby $190 plumbing jobs can beat one distant job at the same hourly rate if travel and setup eat the day. Here’s the quick math: when more of the owner’s day is billed, revenue rises without adding fixed cost, so profit and owner pay improve faster than raw labor hours do.

Track Paid Time, Not Just Busy Time

Track billed hours, paid hours, and total owner hours separately. Compare each job by trade, route, and day of week so you can see where time leaks out. If cancellations or permit waits are common, book clustered jobs or add a minimum service charge so dead time does not wipe out margin.

Test utilization by job mix, not just volume. A full calendar with low-density calls still drains cash if too many hours are unpaid. The target is more paid hours per owner hour, fewer gaps between jobs, and faster billing, so the business can cover overhead and pay the owner without stretching the day.

2

Job Mix

Job Mix

Job mix is the share of plumbing, electrical, carpentry, and emergency work you sell. It changes income because Year 1 labor revenue per job is $190, $315, $340, and $225 before materials and other costs; by Year 5, that rises to $275, $420, $500, and $315. The best mix is the one that lifts gross profit and keeps cash moving.

Repairs usually turn cash faster, installs can slow cash because of scheduling and materials, carpentry can bring scope creep, and emergency work can earn a premium. What this hides is simple: local demand and execution decide profit, not the trade label alone. Track job count, labor revenue, material spend, and callback rate by trade.

Measure Mix by Trade

Break each job into trade type, labor revenue, material delay, and gross margin. Then compare how many cash days each job needs. A $500 Year 5 carpentry job can beat a faster repair only if scope stays tight and rework stays low.

Use a monthly mix target, not gut feel. If emergency work is filling gaps, price the premium and watch response time. If installs are tying up cash, require deposits or staged billing. The one-line rule: more revenue per job only helps if it also improves margin and timing.

3

Labor Leverage

Crew Leverage

This driver is the gap between what crews can bill and what they cost to keep busy. With non-owner payroll at $190,000 in Year 1 and $599,000 in Year 5, plus subcontractor overflow at 30% of revenue in Year 1, owner pay only improves if pricing, schedule density, and billable hours cover the wage load.

The inputs are lead wages of $68,000 for plumbing, $70,000 for electrical, $62,000 for carpentry, and $42,000 for admin, plus helpers, apprentices, and supervision time. What this hides is the cost of callbacks, drive time, and idle gaps; if those rise, labor leverage can cut profit instead of growing it.

Make Crew Time Pay Back

Track gross profit per crew week, billable hours per paid hour, and callback rate by trade. Here’s the quick test: if utilization slips, added staff just raises fixed cost. Subcontracted overflow should be priced so the 30% revenue share still leaves room for coordination, quality control, and your own margin.

Keep high-skill labor on high-value work, bundle nearby jobs, and move admin off the wrench. The owner’s take-home grows when routing, pricing, and job mix fill the payroll base faster than it grows. If supervision is weak, the extra headcount only buys more rework.

4

Cost Control

Cost Control

When payroll is fixed, even small leaks cut owner pay fast. In this model, Year 1 variable costs equal 275% of revenue from materials, subcontractors, fuel, and consumables; by Year 5 they improve to 215%, but the business is still cost-heavy. The key test is gross margin by job, because waste, underbilled materials, or rework can turn booked work into weak cash.

$5,230 per month of fixed overhead sits in the business before marketing and wages, so every job has to carry its share. Track reimbursable materials separately from true margin, and flag callbacks as lost contribution, not free cleanup.

Control Job Costs Early

Use job-level costing with five inputs: invoice value, materials, subcontractors, fuel, and consumables. If a quote does not separate reimbursable material from markup, the owner can’t see real profit. That matters because a few percent of waste, travel, or tool loss hits take-home income hard when fixed payroll already sits in the background.

Keep overhead buckets clear: van maintenance, tool replacement, insurance, software, advertising, storage, licensing, waste, and rework. One clean rule helps: if the cost belongs to a job, assign it to that job; if it supports the whole shop, put it in overhead.

5

Repeat And Referral Demand

Repeat and Referral Demand

Repeat and referral demand means past customers and word-of-mouth bring back jobs without a fresh ad spend. Here’s the quick math: at a $15,000 budget and $150 CAC, the model buys 100 customers; at $75,000 and $120 CAC, it buys 625 customers. More repeat work cuts idle time, supports steadier billing, and gives the owner more confidence to hold price on urgent or specialty jobs.

What this estimate hides: not every lead turns into the same job mix or margin. The owner still needs to track lead source, booked jobs, and gross profit by service so referrals do not hide weak pricing or low-margin work. Booked profitable work pays the owner; empty calendar slots do not.

Track repeat jobs, not just leads

Measure how many booked jobs come from repeat customers and referrals, then compare their CAC, close rate, and gross profit against paid leads. If repeat demand is strong, the same marketing dollar should buy more revenue quality, not just more inquiries.

- Track source on every booked job

- Separate repeat, referral, and paid leads

- Review gross profit by service line

- Watch idle days and schedule gaps

Use that data to shift spend only after the schedule is filling with profitable work. If repeat jobs stay steady, the owner can protect margin, reduce ad waste, and keep take-home pay tied to real booked hours, not just lead volume.

6

Compare low, base, and high tradesman owner-income planning cases

Owner income scenarios

Owner income shifts with billable hours, job mix, and payroll against fixed overhead. The low case defers draws; the high case only works if demand and margins improve.

| Scenario | Low CaseDownside | Base CaseBase case | High CaseUpside |

|---|---|---|---|

| Launch model | This case assumes revenue stays below the cost base, so the owner defers draws. | This case matches the modeled start, but owner pay is still under pressure. | This case assumes stronger demand and a cleaner cost base can support the owner's target pay. |

| Typical setup | Year 1 volume stays thin, billable hours stay low, helper labor is kept tight, and cash reserves come first. | Year 1 modeled revenue is $38,725, pricing holds, and the $85,000 owner pay target is not covered by operating profit alone. | Billable demand rises above payroll load, pricing holds, CAC falls from $150 to $120, job costs improve from 27.5% to 21.5%, and owner pay can be funded. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Deferred drawsCash protected | Target pay unsupportedModel check | $85,000 target payMargin upside |

| Best fit | Use this to stress-test survival if jobs arrive slowly or collections lag. | Use this as the planning baseline for monthly staffing, pricing, and cash calls. | Use this to test upside if job flow, labor use, and close rates all improve. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Tradesman Porter's Five Forces Analysis

- Tradesman BCG Matrix

- Tradesman Business Model Canvas

- 7 Critical KPIs to Track for Tradesman Service Businesses

- Tradesman Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Tradesman Profitability and Scale Service Revenue

- How Much Does It Cost To Run A Tradesman Business Monthly?

- Tradesman Startup Costs: $146K CAPEX Plus Cash Reserve

- Tradesman Financial Model Template in Excel

- Start A Tradesman Business In 4 To 12 Weeks With A Revenue-Ready Plan

- How to Write a Tradesman Business Plan: 7 Steps to Financial Clarity

- Tradesman Marketing Mix

- Tradesman Marketing Plan

- Tradesman Business Proposal

- Tradesman PESTEL Analysis

- Tradesman Pitch Deck Example Editable PPTX

- Tradesman Business SWOT Analysis

- Tradesman Value Proposition Canvas

Frequently Asked Questions

The model includes $85,000 of planned owner pay, but take-home depends on cash profit Year 1 revenue from the provided CAC and service assumptions is about $38,725, while total payroll is $275,000 That means the owner may need to defer draws, add demand, or fund the gap before treating $85,000 as safe take-home