Owner income$90k

Owner income$90kHow Much Wedding Planning Agency Owners Make: $90k Salary Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$90k  Net margin86%–89%

Net margin86%–89% Revenue for target pay$235k

Revenue for target pay$235k Business difficultyHard

Business difficultyHard

You’re modeling owner pay before the agency has steady bookings This guide estimates wedding planning agency owner take-home pay from booked clients, package revenue, gross margin, fixed overhead, payroll, marketing, reserves, and the owner’s role It uses researched US planning assumptions, not employee salary benchmarks, tax advice, or guaranteed earnings

Owner income$90kNet margin86%–89%Revenue for target pay$235kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the full forecast view on owner pay?

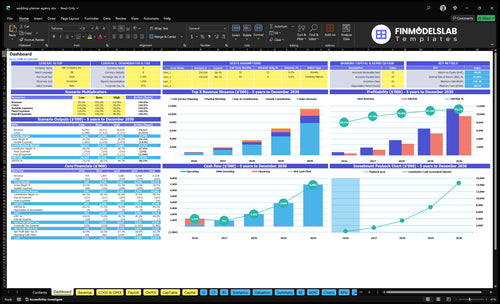

This dashboard shows revenue, gross margin, EBITDA, cash reserve, and owner pay. Use the Wedding Planning Agency Financial Model Template to test service mix, billable hours, hourly price, CAC, marketing budget, fixed expenses, payroll, and direct cost percentages. Scenarios at 50, 160, and 425 clients show Year 1 revenue of $126,525, Year 3 EBITDA of about $101,000, and Year 5 EBITDA of about $897,000 before reserves and taxes. Open.

Owner-income model highlights

- Owner pay charts included

- Revenue and margin tracked

- Scenarios test client volume

How much do wedding planning business owners make per year?

A Wedding Planning Agency owner can make $0 in distributions until profit turns positive, while the boutique model reaches about $101,000 EBITDA in Year 3 on $500,234 revenue; the base agency model already includes a $90,000 lead planner salary. To see if that profit becomes real owner income, tie pay to bookings, price point, gross margin, overhead, workload, and What Is The Most Important Indicator Of Success For Your Wedding Planning Agency?.

Owner pay range

- Solo owner: paid after direct costs

- Base agency: $90,000 planner salary

- Year 3 boutique EBITDA: $101,000

- Year 3 revenue: $500,234

What moves income

- Raise bookings faster than payroll

- Protect gross margin on packages

- Control marketing and fixed overhead

- Watch owner workload before scaling

Can a wedding planner scale income by hiring coordinators?

Yes—a Wedding Planning Agency can scale income with coordinators, but only when pricing, utilization, systems, and client experience support the extra payroll. In this model, staffing may add 0.5 junior planner FTE in Year 2, 1.0 in Year 3, 1.5 in Year 4, and 2.0 in Year 5, with day-of coordinator labor starting in Year 3 at 0.5 FTE.

Owner capacity and agency capacity are different, so seasonality, missed handoffs, weak quality control, and slow lead flow can turn hiring into margin drag.

When hiring helps

- Pricing covers added payroll

- Utilization stays high enough

- Systems support clean handoffs

- Client experience stays consistent

When it hurts

- Seasonality leaves staff underused

- Missed handoffs raise error risk

- Weak quality control hurts margin

- Slow lead flow delays payback

How many weddings do you need to book to make $100k as a wedding planner?

If you want $100k from a Wedding Planning Agency, treat it as a target scenario, not a normal year. Using $2,531 Year 1 weighted revenue per client, 86% gross margin, $300 CAC, $54,000 fixed overhead, and $20,000 admin support, contribution after direct costs and CAC is about $1,876 per booking, so you need about 93 clients ($174,000 ÷ $1,876).

Quick math

- $2,531 revenue per client

- 86% gross margin

- $300 CAC per booking

- ~$1,876 contribution per client

Capacity risk

- 93 bookings to reach target

- $54,000 fixed overhead

- $20,000 admin support

- Owner-led delivery may cap volume

Want to see the six income drivers?

1

50 weddingsAnnual Weddings

At about 50 year 1 clients, each extra booking adds revenue and helps cover fixed costs faster.

2

$2.5KPackage Price

A higher average package price lifts revenue per wedding, so the same booking count produces more owner profit.

3

$300 CACLead Conversion

Keeping customer acquisition cost near $300 protects margin, so more of each booking reaches take-home.

4

14%Event Labor

Direct event labor and related costs at 14% keep delivery margin wide, and every point saved drops to profit.

5

$54KFixed Overhead

With fixed overhead near $54K a year, the business needs enough weddings booked to clear the base cost.

6

$110KTeam Leverage

Year 1 payroll of about $110K only helps take-home if the team frees the founder to sell and manage more weddings.

Wedding Planning Agency Core Six Income Drivers

Weddings Booked Per Year

Booked Weddings

Booked weddings per year is the main cap on owner income. Year 1 marketing and CAC imply 50 acquired clients, Year 3 implies 160, and Year 5 implies 425; the money only shows up when those bookings fit profitable planning capacity.

Here’s the quick math: more bookings raise revenue, but only if the owner can handle peak-season weekends, planning hours, client meetings, vendor calls, and event execution. Low-fit or underpriced inquiries can fill the calendar and still leave take-home pay flat.

Protect Capacity

Measure booked weddings, not inquiry count. Track close rate, hours per client, weekend load, and package mix so each new client still covers labor and direct event costs.

- Booked weddings by month

- Owner hours per wedding

- Peak weekends available

- Low-fit leads declined

One clean rule: stop selling when the next booking creates unpaid revisions or extra event days. If a lead needs too much owner time, price it up or pass, because capacity, not raw demand, drives profit and owner pay.

1

Average Planning Fee

Average Planning Fee

When the average planning fee rises, owner income rises only if the work behind each sale stays controlled. Weighted revenue per client is $2,531 in Year 1 and $3,560 in Year 5, with full-service planning at $3,000, partial planning at $1,950, day-of coordination at $720, and consultation at $525.

Here’s the quick math: higher prices lift gross profit, but only if scope, hours, and client expectations stay tight. Vanity revenue hurts cash flow when premium clients trigger unpaid revisions, extra vendor calls, and more owner time. That turns a bigger invoice into lower take-home pay.

Control Scope and Revisions

Track revenue by package, then compare it with planning hours, revision count, and vendor-management time. The key inputs are client mix, fee per package, and nonbillable work. If full-service clients take far more time than partial or consult clients, the true fee is lower than the invoice says.

Set written limits on meetings, edits, and vendor changes before work starts. A clean scope rule protects margin, so a $3,000 package can stay profitable instead of acting like a discounted labor bundle. If higher-tier clients need extra support, price that support in advance or the owner’s draw gets squeezed.

2

Lead Conversion And Acquisition Cost

Lead Conversion and CAC

This driver is about turning inquiries into booked weddings at a cost that still leaves room for profit. With CAC of $300 in Year 1 and $200 by Year 5, a $15,000 marketing budget can imply about 50 booked clients, while $85,000 can imply about 425. Only profitable bookings help; low-fit leads and long consult cycles burn owner time.

Here’s the quick math: booked clients depend on referrals, venue partners, search visibility, reviews, and the consultation close rate. If close rate slips, CAC rises even when inquiry volume grows. Since this is a service business, each bad lead adds sales time and follow-up with no revenue, so owner pay depends on conversion quality more than raw lead count.

Track close rate by source

Measure inquiries, consults, bookings, and CAC by source so you can see which channels produce real weddings at the lowest cost. Split results by referrals, venue partners, search, and reviews. Use one lead definition each month, or the numbers will drift and hide which channel is actually funding profit.

- Track inquiry-to-consult rate

- Track consult-to-book close rate

- Track CAC by channel

- Cut low-fit leads fast

- Protect time for high-intent couples

Profitable booked clients matter more than volume. If a source brings more inquiries but weak close rates, it raises marketing spend and eats owner time. Tight qualification, faster replies, and stronger proof from past weddings can lift bookings without pushing CAC above $300 now or $200 later.

3

Direct Event Labor And Costs

Direct Event Labor and Costs

Direct event labor and costs are the delivery costs tied to each wedding: travel, on-site coordination, project-specific tools, client entertainment, vendor relationship costs, referral fees, and commissions. In Year 1, they take 14% of revenue, so gross margin is 86%; by Year 5, direct costs fall to 11% and margin rises to 89%. On a $2,531 weighted fee, that is about $354 of direct cost per client.

This margin helps owner pay, but it is not take-home profit. Payroll, rent, marketing, insurance, and admin still come out after gross profit, so a high booking count can still leave weak cash flow if the agency spends too much time or money on each wedding. One bad-fit client can erase the gain from several clean, low-touch bookings.

Track Cost Per Wedding

Measure direct cost by booking and by package, then compare it to fee. If the same wedding needs extra travel, more revisions, or more vendor hand-holding, the gross margin slips fast. Here’s the quick test: direct cost ÷ client revenue should stay near 14% in Year 1 and move toward 11% as systems improve.

- Track travel by event.

- Cap unpaid revision rounds.

- Standardize vendor referral terms.

- Separate entertainment from scope.

Use that data to price high-touch work higher, trim low-value extras, and forecast cash after delivery costs. If delivery cost rises faster than fee, owner draw falls even when sales look strong.

4

Fixed Overhead

Fixed Overhead

Fixed overhead is $54,000 a year, or $4,500 a month, from rent, software, insurance, accounting and legal, utilities, website costs, and supplies. This cost hits profit even in slow months, because it has to be paid before owner pay. It is separate from event delivery costs, so strong gross margin does not protect cash if bookings slow.

Here’s the quick math: at Year 1 weighted revenue of $2,531 per client and 86% gross margin, each booking contributes about $2,177 before overhead. That means fixed overhead alone takes roughly 25 weddings a year to cover. If bookings fall below that, take-home income gets squeezed fast.

Track Overhead Against Booked Weddings

Watch fixed overhead as a monthly run rate and as overhead per booked wedding. A lean office setup can lower b reak-even, but cutting systems too hard can raise labor later. If admin work, software gaps, or weak documentation add hours, the saving can disappear in payroll.

- Track rent, software, and legal monthly.

- Compare overhead to booked weddings.

- Set a $4,500 cash reserve target.

- Measure extra labor from weak systems.

Use booked-client forecasts, not inquiry volume, to test if overhead is safe. For example, $54,000 spread across 50 Year 1 clients equals about $1,080 per client before any owner pay. That number should stay low enough that pricing still leaves room for draw after direct event costs.

5

Team Leverage

Team Leverage

If the owner stays the lead planner, margins stay cleaner but capacity tops out fast. If the owner shifts into sales and management, bookings can rise only when associate planners stay busy and client work still looks premium. That tradeoff is the whole driver: more team can lift income, but only if pricing covers labor and handoffs don’t create extra rework.

Here’s the quick math: payroll rises from $110,000 in Year 1 to $310,000 in Year 5. That can raise owner pay when each hire supports more booked weddings and better service. But if staff sit idle, or the owner has to fix mistakes, distributions shrink fast.

Keep Payroll Tied to Booked Weddings

Track booked weddings per planner, associate utilization, and rework hours. The owner should know how many active clients each planner can handle before service quality drops. If bookings grow but planners are underused, payroll eats cash. If client handoffs are sloppy, the owner loses time and margin.

- Match hires to booked wedding volume.

- Set clear scope for each package.

- Price for labor, not vanity revenue.

- Review handoffs after every event.

A simple test: if a new planner does not add enough revenue to cover salary plus overhead, the hire lowers take-home pay. The goal is a team that helps the owner sell more and serve more, not one that turns into a fixed cost pile.

6

Compare lean, base, and high owner-income scenarios

Owner income table

Owner income swings with client volume, staffing, and how much work the founder keeps versus delegates. The scenarios show a lean solo start, a boutique base, and a larger-team upside case.

| Scenario | Lean SoloStartup risk | BoutiquePayroll leverage | High TeamExecution complexity |

|---|---|---|---|

| Launch model | This is a lower-earnings path built on early client wins and the owner doing most of the work. | This is the modeled middle path where the agency has steady bookings and a small team. | This is a stronger-earnings path that assumes the team can keep scaling without service slipping. |

| Typical setup | About 50 clients, $126,525 revenue, 86% gross margin, $54,000 overhead, and $15,000 marketing leave the owner very involved because there is no reliable distribution base yet. | By Year 3, about 160 clients, roughly $500,234 revenue, high gross margin, and $242,500 payroll land near $101,000 EBITDA before reserves. | By Year 5, about 425 clients, roughly $1,513,000 revenue, 89% gross margin, and $310,000 payroll can still support about $897,000 EBITDA before reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $39,000Lean solo | $101,000Boutique base | $897,000High team |

| Best fit | Use this to stress-test a new agency that is still proving demand and repeatable lead flow. | Use this as the core plan once repeat referrals and a small team are in place. | Use this to test upside if the agency keeps growing and the team can handle more weddings without hurting quality. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Wedding Planning Agency Porter's Five Forces Analysis

- Wedding Planning Agency BCG Matrix

- Wedding Planning Agency Business Model Canvas

- 7 Critical KPIs for Scaling a Wedding Planning Agency

- Wedding Planning Agency Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Wedding Planning Agency Profitability

- How Much Does It Cost To Run A Wedding Planning Agency Each Month?

- Wedding Planning Agency Startup Costs: $54k CAPEX Plus Runway

- Wedding Planning Agency Financial Model Template in Excel

- How To Open A Wedding Planning Agency In 8 To 12 Weeks

- How to Write a Wedding Planning Agency Business Plan in 7 Steps

- Wedding Planning Agency Marketing Mix

- Wedding Planning Agency Marketing Plan

- Wedding Planning Agency Business Proposal

- Wedding Planning Agency PESTEL Analysis

- Wedding Planning Agency Pitch Deck Example Editable PPTX

- Wedding Planning Agency Business SWOT Analysis

- Wedding Planning Agency Value Proposition Canvas

Frequently Asked Questions

The researched model includes a $90,000 annual lead planner salary That is not the same as profit Year 1 revenue is about $126,525, with an 86% gross margin, but payroll, $54,000 fixed overhead, and $15,000 marketing create a loss before distributions