Owner income$17.4k

Owner income$17.4kWhite Labeling Owner Income: $209K Year 1 Before Reserves

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$17.4k  Net margin62.5%

Net margin62.5% Revenue for target pay$334k

Revenue for target pay$334k Business difficultyHard

Business difficultyHard

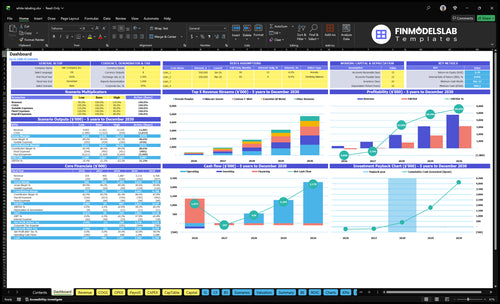

Using the researched assumptions, white labeling business owner income starts with cash the business earns before the owner withdraws it In the first year, the model produces $334,000 in revenue and about $208,600 in operating profit before owner pay, taxes, debt, and reserves, based on the listed fixed costs By the mature year, revenue reaches $4768 million and operating profit before owner pay and reserves reaches about $412 million Actual take-home is lower if cash is held for inventory, deposits, hiring, quality issues, or reinvestment

Owner income$17.4kNet margin62.5%Revenue for target pay$334kBusiness difficultyHardWant to test your white labeling take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Results use model inputs like 334000 in first-year revenue, 4768000 in mature-year revenue, 90 percent gross margin, and 5700 in monthly fixed costs.

Want to check owner income in White Labeling?

See revenue, gross margin, operating profit, and reserve-adjusted owner cash in White Labeling Financial Model Template; scenario tables split profit, costs, reserves, and pay.

Owner-income model highlights

- $334k to $4.768m

- Five product lines

- Volume, pricing, costs

How do white label profit margins affect owner income?

If you’re selling White Labeling products, owner income is driven first by gross margin quality, not just top-line sales. With about $33,602 in first-year unit and production charges on $334,000 of revenue, gross margin is roughly 90%; see How Much Does It Cost To Open And Launch Your White Labeling Business? for the startup-cost side. Logistics at 4% and sales spend at 3% may look small, but they still cut owner cash fast when volume scales.

Margin drives pay

- 90% gross margin on year one

- $300,398 gross profit left

- 38,000 first-year units sold

- 470,000 mature-year units planned

Cash gets squeezed

- 4% logistics eats margin

- 3% sales spend adds up

- Packaging changes cash flow

- Returns and rush runs hurt income

Is a white labeling business profitable?

Yes, White Labeling can be profitable under these planning assumptions: $334,000 first-year revenue, about $300,398 gross profit before logistics and sales spend, and about $208,618 operating profit before owner pay and reserves. The real test is repeat orders, clean production, and cost control; track the growth side with What Is The Current Growth Rate Of Your White Labeling Business? before scaling spend.

Profit math

- Start with $334,000 revenue

- Plan $300,398 gross profit

- Deduct 7% variable expenses

- Cover $68,400 fixed overhead

Risk checks

- Protect repeat client orders

- Control rework and defects

- Avoid heavy client concentration

- Watch logistics and sales spend

How much revenue does a white label business need to pay the owner?

For White Labeling, a $100,000 owner-pay target needs about $202,900 in annual revenue before reserves. Here’s the quick math: with about 90% gross margin, 7% first-year variable expenses, and about 83% contribution after product and variable costs, you still have to cover $68,400 of fixed overhead first.

Quick math

- $100,000 owner pay target

- $68,400 fixed overhead

- 83% contribution rate

- $202,900 revenue needed

Cash drains

- Reserves raise the target

- Debt eats cash flow

- Reinvestment delays pay

- Not guaranteed compensation

Want the six main income drivers?

1

$334K->$4.77MClient Volume

Revenue grows from 38,000 units in Year 1 to 470,000 units in Year 5, so more orders drive the biggest jump in owner take-home.

2

90%Gross Margin

Year 1 gross margin is about 90% after direct unit costs and revenue-based fees, so small price or cost shifts move profit fast.

3

12.4xRepeat Retention

Total units rise from 38,000 to 470,000, so repeat orders compound income more than one-off wins.

4

$0.42-$1.55Supply Efficiency

Direct unit cost ranges from $0.42 on essential oil blends to $1.55 on smart plugs, so sourcing and yield control protect margin.

5

$8.3K/moOverhead Control

Known fixed expenses are about $8.3K per month before wages, so tighter overhead helps EBITDA turn up sooner.

6

$968KCash Buffer

Minimum cash lands at $968K in Month 24, so reserve size and reinvestment pace decide how much cash the owner can safely pull out.

White Labeling Core Six Income Drivers

Client Order Volume And Frequency

Client Order Volume

38,000 units in year one, rising to 470,000 units in the mature year, changes how fast fixed costs get spread. More orders can lift gross profit and steadier cash flow, but only if the business can handle deposits, inventory, production slots, and receivables without delaying owner pay.

Track revenue per client order through average order value, reorder cadence, and minimum order size. One clean rule: more sales help only when capacity and cash keep up; otherwise, growth can create profit on paper and a cash squeeze in the bank.

Measure Order Frequency

Watch order count by client, product, and month, then compare it to production capacity and payment timing. If repeat orders slow or minimum order size drops, revenue quality weakens fast because the same setup work supports less volume.

Use a simple order dashboard: units shipped, reorder days, open receivables, and cash tied up in deposits. The key test is whether added volume improves owner draw after working capital needs, not just top-line revenue.

1

Gross Margin Per Order

Gross Margin Per Order

Gross margin per order is the cash left after direct unit cost and revenue-based production charges, before logistics, sales spend, payroll, overhead, reserves, and owner pay. In this model, first-year source margin is about 90%, with 13% revenue-based production charges. That means the owner’s take-home depends on keeping each order’s direct spread wide enough to fund the rest.

The examples are extreme: a $850 serum with a $0.60 unit cost, or a $1,500 protein powder with a $1.25 unit cost. Even with that spread, margin can get eaten by freight, sales spend, payroll, and rework, so a high sales price alone does not guarantee profit.

Track Margin by Order, Not Just by Line

Build a per-order bridge: selling price minus unit cost, production charge, logistics, and any rush or rework cost. Track gross margin by SKU, client, and order size so you can see which products actually pay for overhead. Here’s the quick rule: if an order does not cover its direct cost plus a fair share of fixed costs, it does not help owner pay.

- Price per unit

- Unit cost

- Production charge

- Logistics rate

- Sales spend per order

- Rework and defect cost

- Overhead share

If logistics runs at 4% in year one and improves to 2% later, the margin lift is real. The same goes for tighter supplier terms and fewer defects. Small leaks matter because this business scales on repeat orders, so every point of gross margin supports more cash for reserves and owner draw.

2

Repeat Purchase Retention

Repeat Purchase Retention

Repeat orders lift owner income because each client order needs less selling work, and the same production setup gets reused. In white labeling, that steadier demand helps forecast materials, packaging, compliance, and fulfillment windows, so rush fees and rework stay lower. One-off custom projects can still bring revenue, but they often add setup time and margin drag.

Track reorder rate, account lifetime value, and churn by client brand. If retention weakens, profit drops before revenue does, because sales effort and waste rise first. That matters when annual overhead is already $68,400 and first-year operating profit only turns into owner pay if enough cash stays free for draws and reserves.

Improve Reorder Cadence

Retention starts with contract terms, quality control, and delivery reliability. Measure repeat order timing by client brand, unit price, order size, and defect or late-ship reason, then compare brands with steady reorders against brands that stall. A client that orders again on schedule is cheaper to serve than a new client.

Here’s the quick math: when reorders come back faster, fixed sales and admin work are spread across more shipped units, so gross margin keeps more of each sale. If a retained client needs fewer corrections, the business keeps more of the $208,618 first-year operating profit for cash, growth, and owner draw.

3

Production, Supplier, And Fulfillment Efficiency

Production and Fulfillment Efficiency

If client price is fixed, this driver decides how much cash is left after production. It covers raw materials, direct manufacturing, packaging, labeling, assembly, testing, waste disposal, utilities, logistics, and sales spend, plus supplier control. Better execution protects the margin spread and raises owner take-home because fewer units get lost to defects, delays, rush fees, and fulfillment errors.

Here’s the quick math: the model assumes logistics at 4% in year one and 2% in the mature year. That drop alone lifts contribution, but only if in-house production and outsourced vendors stay on spec. Track unit cost, scrap rate, on-time ship rate, and rework hours. If those slip, gross profit turns into repair work fast.

Track Unit Cost and Error Rate

Measure each order by unit cost, logistics % of revenue, defect rate, and rush fees. Use the same check at the product, supplier, and shipment level so you can see where margin leaks. If a line needs extra testing, re-labeling, or expediting, price that into the next quote instead of letting owner profit absorb it.

Set a weekly review for supplier lead times, fill rate, and order accuracy. Stable reorders matter because they let you buy materials in planned lots, lock production slots, and cut emergency freight. When fulfillment stays clean, the business keeps more of each dollar of client revenue and has more cash left for payroll, reserves, and owner draw.

4

Overhead And Staffing Discipline

Fixed-Cost Load

Overhead is the money that gets paid before the owner sees take-home. Here, $4,500 monthly office rent plus $1,200 software equals $5,700/month, or $68,400/year. That cost sits on top of gross profit, so if sales growth does not outrun it, owner draw gets squeezed fast.

What this hides: real scaling may also need account management, compliance help, warehouse labor, insurance, and admin support, but those costs are not listed. A new $1,000/month fixed cost means another $12,000/year of profit needed just to keep the owner whole.

Control the Fixed-Cost Run Rate

Track monthly overhead, headcount, and owner draw together. The key test is simple: does each added cost improve order volume, retention, or fulfillment speed enough to pay for itself? If not, it is creep, not scale. Use a monthly budget review before hiring or adding tools.

- Measure overhead against gross profit.

- Separate growth hires from admin drift.

- Stress-test payback before adding staff.

- Watch rent, software, and insurance.

For a white-label business, fixed costs should stay tied to capacity use. If warehouse or compliance work becomes busy every month, model that labor as a needed scale cost. If it is idle most of the time, it is just drag on cash flow and owner income.

5

Working Capital, Reserves, And Reinvestment

Cash Locked In Operations

Here’s the quick math: the model shows $208,618 in first-ye ar operating profit before owner pay and reserves. That is not final take-home. Cash can sit in supplier deposits, inventory, production runs, packaging, and receivables, so the owner may see less spendable cash than the P&L suggests.

One clean rule: if clients pay after you buy materials and ship product, slow distributions until the cash gap is covered. The business also carries $68,400 a year of listed overhead, so growth should fund reserves first, then reinvestment, then owner draw.

Protect the Cash Buffer

Track deposit timing, receivable collection, inventory buys, packaging cash, quality rework, and hiring plans. Those inputs tell you how much profit is truly free cash. A bigger production run can raise profit, but it also raises the cash tied up before the next client payment lands.

- Track deposit timing.

- Watch receivable days.

- Model inventory cash.

- Count rework costs.

- Set reserves before hiring.

A reserve is not profit. Set cash aside for the next production cycle and any delays, then pay yourself only from leftover cash, not from booked earnings.

6

Compare low, base, and high white labeling income scenarios

Planning scenarios

Owner income moves with client volume, unit mix, and margin, while staffing and overhead stay fixed. These three cases show how fast take-home can swing from a slow start to a mature run rate.

| Scenario | Low CaseDownside case | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower-earning path if client volume, repeat orders, and margin all run below plan. | This is the modeled path using the source first-year run rate and the planned operating mix. | This is the stronger earnings path if the business reaches the mature-year run rate and keeps execution tight. |

| Typical setup | The owner stays hands-on while order flow stays soft, gross margin slips, logistics run higher, and reserves stay tight. | Year 1 revenue is $334,000, gross margin is about 90%, variable expenses run near 7%, and fixed overhead plus staffing keep EBITDA at negative $148,000 before breakeven in Month 15. | Year 5 revenue reaches $4.768 million on 470,000 units, with larger sales coverage, better logistics spread, and EBITDA rising to $3.147 million before reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No owner draw yetCash tight | Modest owner drawStabilized draw | High mature-year drawScale-up upside |

| Best fit | Use this to stress-test a slow launch and weaker repeat demand. | Use this as the main planning case for a steady but capital-heavy build. | Use this to test upside if volume scales fast and quality stays under control. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- White Labeling Porter's Five Forces Analysis

- White Labeling BCG Matrix

- White Labeling Business Model Canvas

- 7 Essential KPIs to Track for White Labeling Success

- White Labeling Business Plan Template in Pre-Written Word

- 7 Strategies to Increase White Labeling Profitability and Scale Margins

- How to Calculate Running Costs for a White Labeling Business

- White Labeling Startup Costs: $461K Year 1 Funding Floor

- White Labeling Financial Model Template in Excel

- How To Start A White Label Business With An 8 To 20 Week Launch Plan

- How to Write a White Labeling Business Plan: 7 Actionable Steps

- White Labeling Marketing Mix

- White Labeling Marketing Plan

- White Labeling Business Proposal

- White Labeling PESTEL Analysis

- White Label Pitch Deck Example Editable PPTX

- White Labeling Business SWOT Analysis

- White Labeling Value Proposition Canvas

Frequently Asked Questions

In this planning case, first-year operating profit before owner pay and reserves is about $208,600 on $334,000 of revenue That is not guaranteed take-home The owner still needs to hold cash for reserves, debt, taxes, inventory, hiring, and reinvestment Mature-year operating profit before owner pay and reserves reaches about $412 million in the model