White Labeling Startup Costs: $461K Year 1 Funding Floor

This page separates CAPEX, pre-opening expenses, working capital, and total funding need for a US white labeling launch The first operating year model shows $334,000 of sales, $460,982 of known operating costs before CAPEX and deposits, and a $126,982 cash gap before equipment, buildout, taxes, debt service, and contingency

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates launch-ready capitalized startup assets only, not your full funding need.

What this excludes This calculator covers capitalized startup assets only. It excludes raw materials, MOQs, inventory, payroll runway, deposits, debt service, working capital, legal fees, marketing, and subscriptions unless you capitalize them under your accounting policy.

What does the CAPEX tab show?

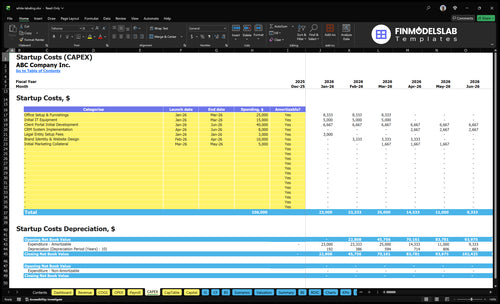

CAPEX tab in White Labeling Financial Model Template shows startup-cost categories, timing, amounts, and depreciation/amortization. Open it and review assumptions.

Key screenshot checks

- Startup assets and quotes

- Launch-month timing

- Funding gap check

How do white label manufacturing costs compare with contract manufacturer versus own production cost?

White Labeling is usually cheaper to start with contract manufacturing, but not always cheaper per unit once fees, deposits, and MOQs kick in. Here’s the quick math: modeled unit costs run from $0.42 for an essential oil blend to $1.55 for a smart plug, plus about 13% of revenue for quality control, factory fee, compliance testing, waste disposal, and utility surcharge. Own production can win only if Year 1 volume of 38,000 units is high enough to justify equipment, tooling, buildout, QC assets, warehouse fixtures, and installation.

Contract cost mix

- Per-unit fees replace fixed labor

- Factory fees raise unit cost

- Deposits tie up cash

- MOQs force bigger buys

Own production tradeoff

- CAPEX hits cash early

- Tooling and buildout add cost

- QC assets improve control

- Volume must cover fixed load

How much money do you need to start a white labeling business?

You need at least $460,982 to start a White Labeling business for the first operating year, and the real funding need is higher once CAPEX, deposits, MOQs, samples, taxes, debt service, and contingency are added; track demand early with What Is The Current Growth Rate Of Your White Labeling Business?. Here’s the quick math: $334,000 Year 1 sales across 38,000 units leaves a $126,982 operating cash gap before startup assets. If you fund only the machines, you’ll run out of cash before the first repeat order.

Funding Floor

- $460,982 first-year operating floor

- $334,000 projected Year 1 sales

- 38,000 units sold in Year 1

- $126,982 cash gap before assets

Cost Traps

- Add CAPEX before launch planning

- Budget supplier deposits and MOQs

- Fund samples, taxes, and debt service

- Expect receivables float with outsourced production

How should you plan funding a white labeling business?

White Labeling should be funded as a full cash plan, not just a startup budget: start with the modeled $460,982 Year 1 cost floor, then add equipment/buildout quotes, deposits, MOQs, samples, insurance binders, legal setup, and a cash cushion because modeled revenue is only $334,000. The gap is at least $126,982 before any extra cushion, so cash leaves before clients pay and runway matters. With $8,250 in monthly overhead before payroll, plus $260,000 for CEO and Head of Operations and $45,000 for a Sales Manager in Year 1, the funding plan should show timing month by month.

Fund the full need

- Start with $460,982 cost floor.

- Add buildout and equipment quotes.

- Include deposits, MOQs, samples.

- Hold cash for delays and overruns.

Track cash timing

- Model $334,000 Year 1 revenue.

- Map client payment timing clearly.

- Track $8,250 monthly overhead.

- Stress test longer onboarding runway.

Calculate Fuding Needs

Startup cost summary

This table covers white-label startup CAPEX and the non-CAPEX cash reserve needed to launch and reach breakeven.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Office Setup & Furnishings | $25,000 | Launch workspace buildout | Yes |

| Initial IT Equipment | $15,000 | Owner and ops hardware | Yes |

| Client Portal Initial Development | $40,000 | Build customer ordering portal | Yes |

| CRM System Implementation | $8,000 | Set up sales tracking | Yes |

| Brand Identity & Website Design | $10,000 | Launch brand and site | Yes |

| Working Capital Reserve | $968,000 | Payroll runway, fixed overhead, and launch cash before breakeven | No |

White Labeling Core Five Startup Costs

Production Equipment and Facility Buildout Startup Expense

CAPEX split

If you make products in-house or partly in-house, treat durable assets as CAPEX: machinery, tools, fixtures, quality-control gear, installation, utility readiness, workspace upgrades, and production testing. Keep raw materials, packaging, consumables, and payroll out of this bucket. The split changes fast between outsourced, hybrid, and in-house setups.

Quote math

Here’s the quick math: use user-entered quotes for each asset, then multiply by quantity and add install and startup testing. The model does not provide vendor CAPEX quotes, so the clean input is what you were actually quoted. Refine it by asking what products are made internally, what batch size is needed, and which items are depreciable.

Spend control

To keep spend tight, buy only the assets tied to internal production and phase the rest after launch. Don’t bury labels, packaging, or consumables in equipment cost. For outsourced runs, this line should shrink; for in-house runs, it grows with batch size and QC needs. Lease-versus-buy can help, but only for assets you will use often.

Funding check

Anchor the buildout against the known $460,982 of Year 1 operating costs. If equipment, buildout, and readiness work create a big upfront cash need, fund it separately from monthly ops. One clean filter helps: if the item helps you make or test product before first shipment, it belongs here; if not, it belongs elsewhere.

Product Development, Samples, and Quality Testing Startup Expense

Pre-Launch Work

Treat prototypes, sample batches, specs, SOPs, packaging mockups, testing, revisions, and documentation as pre-opening expenses unless you capitalize them. For these five lines — skincare serum, protein powder, essential oil blend, custom T-shirt, and smart plug — the spend belongs in startup funding, not unit cost.

Testing Budget

Here’s the quick math: compliance testing is modeled at 0.2% of Year 1 revenue and quality control at 0.5%. With $334,000 of product revenue, that equals $668 plus $1,670, or about $2,338 combined. Budget by SKU, test round, and revision count.

Cut Rework

Lock specs before you order samples, and test packaging early. Failed samples and label changes can delay sales even when unit economics look clean. One bad revision can push launch dates across every line, so keep each round tight and track what changed, who approved it, and whether the fix is still worth the delay.

Delay Risk

Use one sample plan for all five product lines, but do not share assumptions across them. A serum, powder, oil blend, T-shirt, and smart plug each need their own test path, and compliance steps. If packaging or documentation changes after approval, treat that as extra pre-opening spend and extra launch time.

Compliance, Legal, Insurance, and Contract Setup Startup Expense

Legal Setup

For white labeling, the startup cash goes to business formation, MSAs (master service agreements), NDAs (nondisclosure agreements), and IP ownership terms. Keep product-law language general, since US rules vary by category. The fixed load is $1,000 per month for legal and accounting plus $350 per month for insurance, or $16,200 a year.

What It Covers

This cost covers product liability insurance, labeling review, industry-specific compliance, and customer contract templates. It also includes revenue-linked compliance testing at 0.2% of product revenue, or $668 in Year 1. Here’s the quick math: $16,200 fixed plus $668 variable, before any product-specific legal work or filing fees.

How To Control It

Use one core contract pack, then add product-specific addenda only when needed. Ask for flat fees on formation, templates, and review cycles, and avoid redoing terms for each client. Keep insurance binders and contract setup out of CAPEX; they are startup expenses, not durable assets. The main waste is paying twice for the same review.

Budget Guardrail

Use $16,200 as the base annual compliance budget, then add 0.2% of product revenue for testing. For Year 1, that means $668 on $334,000 of revenue. If product rules change by category, keep the legal reserve flexible so labeling, insurance, and contract updates do not stall launches.

Initial Inventory, Raw Materials, Packaging, and MOQ Startup Expense

Launch Inventory

Inventory and MOQs are working capital, not CAPEX. They cover supplier deposits, raw materials, components, labels, primary and secondary packaging, freight, and buffer stock. In Year 1, modeled unit costs total $29,260 across 38,000 units, so cash is tied up before customer invoices are paid.

Unit Costs

Use per-unit quotes and MOQ sheets for each line: $0.60 skincare serum, $1.25 protein powder, $0.42 essential oil blend, $0.75 custom T-shirt, and $1.55 smart plug. Add packaging, labels, and freight to each unit, since small line items become real money at scale.

- Ask for landed unit cost.

- Match buys to launch dates.

- Track cash before invoicing.

Packaging Cash

Packaging and labels look tiny per unit, but they hit cash hard when you buy them before sales land. On 38,000 units, even a few cents each adds up inside the $29,260 launch inventory pool, and freight plus buffer stock raise the check before any customer payment.

- Quote labels separately.

- Price cartons by volume.

- Keep buffer stock lean.

Cash Timing

Place smaller first buys against real launch dates and customer commitments, not the full forecast. That cuts idle stock, but keep enough buffer for reorders and freight delays. The main mistake is treating launch inventory like a fixed asset; it is cash tied up until products ship and invoices clear.

Software, Client Onboarding, and Sales Launch Startup Expense

Split setup from run rate

For a software, client onboarding, and sales launch budget, keep one-time setup separate from recurring spend. That means website build, CRM setup, order management, invoicing, client portal, catalog, spec sheets, sales materials, trade outreach, and onboarding workflows sit in startup costs, while monthly software and payroll sit in runway.

Recurring systems

The model includes $1,200 per month for software subscriptions and $800 per month for platform maintenance, or $24,000 annually. Add the Sales Manager early in ramp-up and plan $45,000 of Year 1 payroll. Here’s the quick math: recurring operating cost starts at $69,000 before sales support spend.

- $1,200 software per month

- $800 platform maintenance per month

- $45,000 Sales Manager payroll

Launch spend control

Keep launch costs tight by buying only the tools you need on day one, then add features after the first client wins. Variable sales and marketing is modeled at 30% of Year 1 revenue, or $10,020, so every extra outreach dollar should tie to a booked order. One clean rule: if it won’t help close or onboard clients, delay it.

- Buy setup once, not twice

- Delay extra software seats

- Track payback by client

Budget watchout

What this estimate hides: the monthly stack starts fast, because $24,000 of software and maintenance plus $45,000 of Sales Manager payroll comes before variable sales spend. If onboarding takes longer than planned, cash ties up in tools and labor before client orders scale.

Compare 3 Startup Cost Scenarios

Scenario table

Lean, base, and full launch paths change upfront cash needs fast. All three start from the same Year 1 model: $334,000 sales, $460,982 known costs, and 38,000 units.

| Scenario | Lean LaunchLowest CAPEX | Base LaunchBalanced control | Full LaunchHighest control |

|---|---|---|---|

| Launch model | Lean launch outsources most production and keeps owned assets light. | Base launch mixes outsourced production with selective owned tools and QC assets. | Full launch brings production, installation, and compliance readiness in-house. |

| Typical setup | Use small in-house tools, sample checks, deposits, and outsourced runs. | Keep core systems and quality checks in-house, while using outside partners for part of production. | Build the facility, buy equipment, install tooling, and staff for end-to-end control. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | Lowest-capex bandLowest setup load | Mid-range funding bandBalanced setup load | Highest setup bandHighest setup load |

| Best fit | Best for founders testing demand with limited cash and higher supplier dependence. | Best for teams that want more control without a full factory build. | Best for high-volume products where compliance and process control matter most. |

Planning note: Ranges are researched planning assumptions from the model, not vendor quotes or exact bids.

Related Products

- White Labeling Porter's Five Forces Analysis

- White Labeling BCG Matrix

- White Labeling Business Model Canvas

- 7 Essential KPIs to Track for White Labeling Success

- White Labeling Business Plan Template in Pre-Written Word

- 7 Strategies to Increase White Labeling Profitability and Scale Margins

- How to Calculate Running Costs for a White Labeling Business

- White Labeling Financial Model Template in Excel

- White Labeling Owner Income: $209K Year 1 Before Reserves

- How To Start A White Label Business With An 8 To 20 Week Launch Plan

- How to Write a White Labeling Business Plan: 7 Actionable Steps

- White Labeling Marketing Mix

- White Labeling Marketing Plan

- White Labeling Business Proposal

- White Labeling PESTEL Analysis

- White Label Pitch Deck Example Editable PPTX

- White Labeling Business SWOT Analysis

- White Labeling Value Proposition Canvas

Frequently Asked Questions

A lean outsourced launch still needs meaningful cash because the model shows $460,982 of known Year 1 costs before CAPEX, deposits, MOQs, and contingency That includes $305,000 of wages, $99,000 of fixed overhead, and $56,982 of direct and revenue-linked variable costs against $334,000 of Year 1 sales