How Much Bank Loan Service Owners Make: $120K Pay Plus EBITDA

You’re modeling owner take-home from a US Bank Loan Service, not a banker salary or a guaranteed wage This covers $325K to $2618M in modeled annual revenue, $120K CEO / Lead Loan Advisor pay, EBITDA, costs, reserves, and funded-loan economics It excludes income tax planning, legal licensing advice, lender approval promises, and borrower credit outcomes

Owner income$112K-$1.68MNet margin-2.5% to 59.6%Revenue for target pay$325KBusiness difficultyHard

Want to test your own owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want the six biggest income drivers?

1

Loan Closings

20-150/yr

More funded loans drive most revenue, so each extra closing adds high-fee income.

2

Fee Stack

$3.75K-$4.4K

A richer mix of prep, facilitation, and closing fees lifts revenue per client fast.

3

Lead Cost

13%-8%

Paid marketing and referral spend falls from 13% to 8% of revenue, so more of each fee stays with the owner.

4

Conversion

20%-23%

Moving consultations into closings from 20% to 23% turns the same lead flow into more take-home profit.

5

Payroll

$200K-$585K

Payroll rises hard as staff scales, so hiring ahead of volume can eat the margin from new deals.

6

Cash Reserve

$875K

Fixed compliance, insurance, software, and reserve timing push minimum cash to $875K in Month 2, which protects distributions.

Want to see the owner income model for Bank Loan Service?

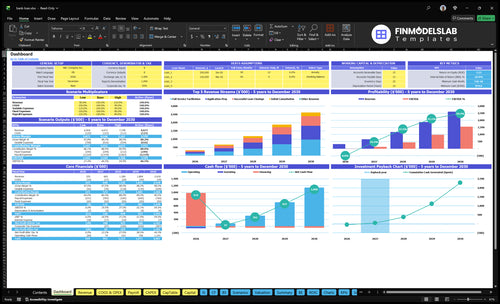

The dashboard shows revenue, EBITDA, cash, breakeven, payback, and owner income. Assumptions cover consultation, application prep, full-service, and successful closing volumes, while cost tabs show 30% to 15% credit-check costs, 100% to 70% marketing, 30% to 10% referral commissions, and $498K overhead; open Bank Loan Service Financial Model Template to plan.

Owner-income model highlights

Owner income sits on dashboard

Volumes drive each service line

Costs and overhead shape take-home

Can a bank loan service replace a full-time income?

Yes, in the modeled case, a Bank Loan Service can replace a full-time income, but only if volume, conversion, and cash runway hold. The model targets $120K owner pay from Month 1 payroll, but Year 1 EBITDA is -$8K, so early pay depends on capital cushion. The minimum cash need is $875K in Month 2; by Year 2, revenue reaches $665K and EBITDA improves to $130K after owner pay target, so this is a planning output, not a guaranteed wage.

What must hold

Keep lead volume steady

Protect conversion rates

Hold enough cash runway

Plan pay as output

Key model numbers

$120K owner pay target

-$8K Year 1 EBITDA

$875K cash need in Month 2

$665K Year 2 revenue

Does a bank loan service owner need to work in the business?

Yes—at least early on, the owner should work in the Bank Loan Service. Keeping the founder as a 10 FTE CEO / Lead Loan Advisor at $120K a year can protect margin when volume is still modest, but by Year 5 the model grows to 80 FTE from 20 FTE in Year 1, so the job shifts into compliance, training, borrower support, and referral-partner oversight.

Owner-led early

10 FTE founder role lowers overhead.

$120K keeps payroll predictable.

Best when volume is still low.

One owner keeps service quality tight.

Staffed growth risk

20 FTE in Year 1 scales to 80 FTE.

More staff can support 150 annual closings.

Higher headcount raises compliance load.

Training and oversight get harder fast.

How many loans does a bank loan service need to close to pay the owner?

A Bank Loan Service needs 40 successful loan closings in Year 2 to support $120,000 CEO / Lead Loan Advisor pay in this model; for the operating KPI behind that target, see What Is The Most Critical Metric To Measure The Success Of Your Bank Loan Service?. The model reaches breakeven in Month 13, with $665,000 Year 2 revenue and $130,000 EBITDA after payroll. Here’s the quick math: don’t count every referred borrower as funded, because the funnel falls from 200 consultations to 100 prep jobs to 60 full-service cases to 40 closings.

Owner Pay Target

Close 40 loans in Year 2

Pay owner $120,000

Reach breakeven in Month 13

Produce $130,000 EBITDA after payroll

Funnel Reality

Start with 200 consultations

Convert 100 to application prep

Move 60 into full service

Fund 40, or 20% of consultations

Key Takeaways

Funded closings, not inquiries, drive all revenue.

Conversion leakage can crush loan volume and fees.

Marketing, payroll, and compliance shape margin and cash.

Cash reserves must cover lender payout delays.

Compare lean, base, and high-growth owner-income cases

Owner income scenarios

Owner income moves with closings, fees, and the pace of hiring. Early cash is tight, then the model opens up fast once volume reaches the base and high cases.

Compare lean, base, and high owner income at different loan volumes.

Scenario

Lean CaseLean

Base CaseBase

High CaseHigh

Launch model

A lean launch keeps owner income close to early cash capacity.

A modeled mid-case lifts owner income as volume and margin improve.

A stronger scale case pushes owner income higher as closings and EBITDA rise.

Typical setup

Year 1 runs at 20 closings, about $325K revenue, and -$8K EBITDA, so the owner is still carrying a thin launch profile.

Year 3 reaches about $1.18M revenue, 70 closings, and $443K EBITDA, with a fuller team and better operating spread.

Year 5 reaches about $2.618M revenue, 150 closings, and $1.559M EBITDA, with the largest team and the lowest partner drag.

Cost drivers

20 closings

$325K revenue

-$8K EBITDA

$120K owner pay

early fixed payroll

70 closings

$1.18M revenue

$443K EBITDA

lower marketing spend

added support staff

150 closings

$2.618M revenue

$1.559M EBITDA

more advisor capacity

lower partner fees

Owner income rangeBefore owner reserves

$112,000Lean income

$563,000Base income

$1,679,000High income

Best fit

Use this to stress-test the first-year cash gap and slow sales ramp.

Use this for a realistic third-year run rate and cash build.

Use this to test upside when the sales funnel and close rate stay strong.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; the model shows breakeven in Month 13 and payback in 23 months.

Bank Loan Service Core Six Income Drivers

Funded Loan Volume

Funded Loan Volume

Funded loan volume is the cash event here: no funding, no success fee. Year 1 is 20 closings from about 100 consultations; Year 5 is 150 closings from 650 consultations. At a $3,750 to $3,950 closing fee, closing-fee revenue moves from about $75,000 to $592,500 before any upstream package fees.

The risk is leakage between consultation, application prep, and funded loan stages. Year 1’s 20% close rate and Year 5’s roughly 23% close rate show why volume matters more than inquiries. If that flow slips, the owner still pays staff, software, and compliance costs, so profit and owner draw drop fast.

Track the Funding Funnel

Measure the funnel weekly, not just lead count. The core inputs are consultations, applications, funded loans, and fee per closing. Here’s the quick math: more funded loans lift both closing revenue and attached service revenue, while weak conversion leaves fixed costs exposed.

Track consult-to-fund conversion.

Track application completion rate.

Track revenue per funded loan.

Keep prequalification tight so staff time goes to clients most likely to close. If funded volume stays near 17 closings a month in Year 1 but grows toward 125 closings a month by Year 5, the business can support higher owner pay; if not, cash stays thin.

Borrower Acquisition Cost

Borrower Acquisition Cost

Borrower acquisition cost is what you spend to win one funded loan, not just one lead. In this model, performance-based marketing is 100% of revenue in Year 1 and still 70% in Year 5, so paid growth directly cuts owner income. Referral partner commissions also matter, falling from 30% to 10% as the mix improves.

Here’s the key test: measure cost per funded borrower against closing revenue, not inquiry volume. If you buy cheap leads that do not convert, cash drains fast and profit disappears. A better mix of referrals, lender relationships, content, and partnerships lowers acquisition cost and protects take-home pay.

Track cost per funded borrower

Build the metric from marketing spend, referral commissions, lead volume, consultation count, applications, and funded loans. The owner should watch cost per funded loan each month, plus the path from consultation to application to closing. With 20 funded loans in Year 1 and 150 in Year 5, volume only helps if cost per close falls too.

Use channels that raise conversion, not just traffic. Tie every campaign to funded outcomes, then pause sources with weak close rates. If a channel looks cheap but fails to produce approvals, it is expensive in real terms because it burns cash and lowers owner draw.

Measure cost per funded loan.

Track lead-to-close conversion.

Watch referral fee %.

Cut low-quality lead sources.

Favor lender and referral partners.

Funded Loan Conversion Rate

Funded Loan Conversion Rate

Conversion rate is the share of consultations that turn into funded loans, so it is the bridge between busy activity and real revenue. In Year 1, 100 consultations led to 20 successful closings, a 20% consult-to-fund rate. By Year 5, 650 consultations produced 150 closings, or about 23%, so small gains in conversion matter a lot to owner income.

Here’s the quick math: Year 1 moved from 100 consultations to 50 prep jobs, 30 full-service cases, and 20 closings; Year 5 moved to 380 prep jobs, 220 full-service cases, and 150 closings. The real risk is pipeline leakage between stages. Better borrower fit, cleaner documents, and tighter lender matching lift funded volume, but final approval still depends on borrower quality and lender rules.

Track Stage Conversion, Not Just Leads

Measure each step: consultation to prep, prep to full-service, and full-service to funded close. The data here shows 50% of consultations became prep jobs in Year 1 versus about 58.5% in Year 5, while full-service to close held near 67% to 68%. That tells you where the funnel is leaking and where staff time is being wasted.

Use a simple checklist before moving a borrower forward: income docs, debt picture, credit quality, and lender fit. Forecast cash using funded closings only, not inquiries, because revenue lands at the close and owner pay follows. A one-line rule helps: no clean file, no close.

Compliance, Reserves, And Cash Timing

Compliance and Cash Reserves

Compliance protects fee income, because weak controls can block payouts or force refunds. This model has $300 professional insurance, $500 CRM, $200 cybersecurity, and $400 legal and compliance retainer each month, before variable checks. Credit and background checks can run from 30% to 15% of revenue, so margin drops fast if the file quality is poor.

Cash timing is the other pressure point. Delayed lender payouts can create a gap even after a loan closes, and the minimum cash need is $875K in Month 2. Here’s the quick math: owner income only becomes usable after fees clear, bills are paid, and the cash lands on time.

Track the payout gap, not just the closing

Measure compliance risk by closed loans, check costs as a percent of revenue, and days from lender approval to cash receipt. Validate licensing, insurance, and referral rules with qualified professionals, because one rule miss can wipe out a deal’s profit and delay owner pay.

Hold $875K by Month 2.

Watch checks at 30% to 15%.

Match payout timing to bills.

Document licensing and referral rules.

Average Fee Per Funded Loan

Average Fee per Funded Loan

Average fee per funded loan is the main revenue lever on each close. Moving the modeled success fee from $3,750 to $3,950 adds $200 per funded loan; at 20 closings, that is $4,000 more revenue. Consult, prep, and facilitation fees sit upstream, so the real revenue per closing is higher, but only if fee limits and lender rules still allow the structure.

At the model’s Year 1 level, revenue is $325K on 20 closings; by Year 5, the provided model shows $2,618M on 150 closings. The owner’s take-home rises when the fee mix grows faster than delivery cost. If client mix shifts toward lower-fee cases, profit and cash flow fall even when funded volume holds steady.

Track the fee mix by closing

Measure revenue per funded loan by package, not just by lead. Split consult, prep, facilitation, and success fee income so you can see which step pays and which one gets capped by lender rules or referral limits. The key check is simple: if the average fee rises but conversion falls, net owner income may not improve.

Track fee by client type.

Watch funded closings monthly.

Compare fee caps by lender.

Test $3,750 vs $3,950.

Also watch the borrower mix. A case that needs more prep can justify more upstream revenue, but if it takes longer to close, cash comes in later. That matters when fixed costs keep running and the owner draw depends on funded loans, not just signed clients.

Staffing Model

Owner Pay vs Payroll

At low volume, owner-led delivery can protect margin because the founder does more of the work. In Year 1, the model assumes $120K owner pay plus $80K for a senior advisor, so staffing is still lean. The key is to treat owner labor as an operating cost, not profit, so take-home income is not overstated.

By Year 5, payroll rises to $585K with advisors, processors, marketing, and admin support. Here’s the quick math: more funded loans need more people to keep turnaround time and service quality stable. The risk is hiring before volume supports utilization, meaning billable time tied to funded work.

Staff to Funded Loan Volume

Track staffing against funded loans, not inquiries. If consultations rise but closings do not, payroll can outrun revenue fast. Use monthly funded volume, advisor capacity, and processor load to decide when to add headcount. One clean rule: hire only when current staff is close to fully used on real cases.

Split reports into owner labor, paid staff labor, and profit draw. That keeps the real margin visible and helps you see whether the business can still pay the owner after wages. What this estimate hides: if onboarding is slow or case mix is messy, utilization drops and payroll pressure shows up before revenue does.