Bank Loan Service Startup Costs: $385K CAPEX Plus Cash Reserve

Plan for $38,500 in launch CAPEX plus working capital sized to the model’s $875,000 minimum cash need in Month 2 This page covers startup budget categories, CAPEX, pre-opening expenses, payroll ramp, marketing, compliance, and first operating year funding needs, excluding borrower loan capital supplied by banks These are researched planning assumptions, not vendor quotes, regulatory advice, or guaranteed costs

Calculate Fuding Needs

Startup Cost Summary Table

This table shows modeled startup cash needs for office setup, technology, branding, and the opening cash buffer.

Highlighted CAPEX$38,500Base planning example

Excluded cash needs$875,000Outside CAPEX total

Funding need$913,500CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

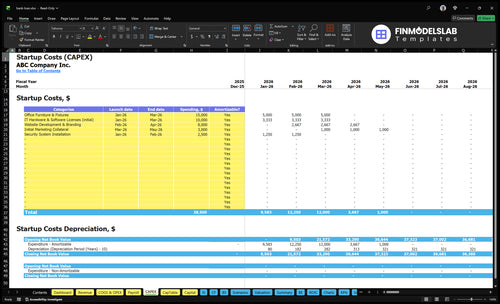

Office Furniture & Fixtures

$15,000

Office buildout and furnishings

Yes

IT Hardware & Software Licenses

$10,000

Initial computers, devices, and licenses

Yes

Website Development & Branding

$8,000

Site build and brand setup

Yes

Initial Marketing Collateral

$3,000

Launch materials and client outreach

Yes

Security System Installation

$2,500

Premises security equipment and install

Yes

Opening Cash Buffer

$875,000

Month 2 runway for payroll, rent, and overhead before breakeven

No

Estimate Startup Costs with Calculator

Startup CAPEX

This estimates capitalized startup assets only, before working capital and other operating needs.

!

Excluded costs This tool excludes inventory, payroll runway, rent deposits, debt service, working capital, monthly CRM, monthly cybersecurity, monthly marketing, and other operating expenses unless they create a capitalized asset.

Office size, advisor count, and compliance load move cash needs fast in a loan service. Lean keeps spend tight; full launch adds staff and process cost.

Lean, base, and full launch cost bands

Scenario

Lean LaunchSolo consultant

Base LaunchSmall advisory office

Full LaunchMulti-advisor support

Launch model

Founder-led service from a home office with limited paid support.

Small-office launch built around the core setup in the model anchor.

Client-facing team model with broader lending support, more staff, and heavier compliance.

Typical setup

One advisor, basic software, and light marketing.

Two advisors, standard office space, CRM, legal support, and steady lead gen.

Multiple advisors, a processor, marketing staff, and a fuller office build-out.

Cost drivers

Licensing scope

home-office overhead

basic software stack

light marketing

compliance review

Office footprint

advisor count

software stack

compliance burden

marketing budget

Advisor count

processor timing

larger office footprint

compliance burden

referral spend

Planning rangeCAPEX only

$250,000 - $500,000Low cash need

$750,000 - $950,000Model anchor

$1,000,000 - $1,400,000High cash need

Best fit

Best for a solo consultant testing demand before hiring.

Best for a small advisory office serving a steady loan pipeline.

Best for a multi-advisor lending support operation built for scale.

!

Planning note: Scenario ranges are researched planning assumptions, not exact quotes or guaranteed outcomes.

How do I turn bank loan service startup costs into a funding plan?

For Bank Loan Service, fund the launch with $38,500 CAPEX, then add $4,150 in monthly fixed overhead, $200,000 in Year 1 payroll, launch marketing, and variable costs until the fee model reaches $325,000 in Year 1 revenue. That still leaves EBITDA at -$8,000, so the funding plan has to cover burn through Month 13 breakeven and a 23-month payback. Price consultation, application prep, full-service facilitation, and success fees so each closing helps fund the next staffing step.

Funding stack

$38,500 CAPEX first

$4,150 monthly overhead

$200,000 Year 1 payroll

Include launch marketing cash

Model checks

Target $325,000 Year 1 revenue

Expect -$8,000 EBITDA

Test Month 13 breakeven

Model 23-month payback

What hidden costs should a bank loan service budget for?

A Bank Loan Service should budget for setup and operating costs that hit before fee income arrives: rent deposits, CRM onboarding, credit-report access, background-check setup, secure document collection, compliance binders, insurance certificates, data protection, lead testing, lender outreach, and payroll. The base load is already $4,150 a month in fixed overhead before wages, plus a $16,667 monthly Year 1 payroll run-rate from $200,000 in annual wages; that’s why the service must keep operating costs separate from borrower loan funds and optional growth spend, as in How Much Does The Owner Of Bank Loan Service Typically Make?.

Fixed launch costs

Rent deposits before revenue

CRM onboarding setup fees

Credit access setup costs

Compliance and insurance files

Year 1 variable costs

100% performance marketing

30% referral partner commissions

30% third-party checks

Payroll before cash comes in

Also budget for secure document collection, lead testing, and lender outreach, because those tasks burn cash early even when they do not create revenue right away.

What to track

$4,150 fixed overhead monthly

$16,667 payroll monthly

Year 1 check and ad costs

Cash timing before first close

Cost buckets

Operating costs, not loan funds

Growth spend stays separate

Setup costs hit first

Revenue lag drives strain

How much does it cost to start a bank loan service?

The base launch assumes $325,000 in Year 1 revenue from 100 consultations, 50 application prep packages, 30 full-service clients, and 20 successful closings, with breakeven in Month 13 and payback in 23 months.

Key Takeaways

Legal and compliance costs start with monthly retainers.

Technology needs one-time setup plus monthly subscriptions.

Office costs split between CAPEX and monthly overhead.

Marketing and referral spend scale with Year 1 revenue.

Bank Loan Service Core Five Startup Costs

Licensing, Legal, And Compliance Startup Expense

Legal setup

Start with entity formation, state registrations, and the right license path for your model. Requirements change by state, loan type, and whether you do referral-only or active facilitation. For budgeting, add the source model’s $400 monthly legal retainer, $300 professional insurance, and $200 cybersecurity cost. This is budgeting guidance, not legal advice.

What to budget

Cost drivers are attorney review, borrower disclosures, referral agreements, lender partner contracts, privacy procedures, and compliance policies. Use the source monthly total of $900 as your baseline, then add any state filing fees, surety bonds, or broker licensing costs where required. Consumer loans, commercial loans, and mortgages can each trigger different rules.

Map rules by state first

Separate referral from facilitation

Get contracts reviewed early

How to keep it lean

Keep the first draft tight: one counsel, one compliance owner, and one standard document set. Don’t skip disclosures or privacy controls to save cash; that mistake gets expensive fast. A clean setup can still stay near the source budget of $900 per month before any state-specific filing or bonding costs.

Reuse approved templates

Limit states at launch

Document every workflow

Risk flags

If you cross from referral-only into active facilitation, or touch consumer lending, mortgages, or broker activity, compliance scope can expand quickly. Here’s the quick math: $400 legal + $300 insurance + $200 data protection = $900/month before one-time filings, bonds, and contract work.

Loan Workflow Technology And Data Security Startup Expense

Build the Stack

$10,000 covers the one-time IT hardware and initial software licenses for CRM, intake forms, document upload, e-signature, cloud storage, credit report access, background checks, and user permissions. That is the launch layer; monthly software runs on top. If setup slips, onboarding slows and files pile up.

Run-Rate Costs

The monthly software base is $500 for CRM plus $200 for cybersecurity and data protection, or $700 a month. Over 12 months, that is $8,400 in SaaS spend, separate from the one-time build. Use vendor quotes, seat counts, and months of coverage to keep budget lines clean.

Trim Without Risk

Save by buying only the licenses you need at launch, not by skipping controls. Use role-based access, limited admin rights, and a simple intake flow first, then add tools as volume grows. The documents are sensitive: bank statements, tax returns, identification, and business records. Weak security is not a place to cut.

Protect Client Data

Use secure upload links, encrypted cloud storage, and a tracked background check workflow so every file has a clear owner and access log. Subscription onboarding should include permissions review on day one. If a vendor cannot prove secure handling of client data, do not trade that risk for a lower monthly price.

Website, Branding, And Client Acquisition Startup Expense

What it covers

The front-end spend covers the site, landing pages, local search setup, borrower education content, referral materials, branding, paid lead tests, lender outreach, and local profile setup. Budget $8,000 for website development and branding CAPEX, plus $3,000 for initial marketing collateral. This is the first trust signal for a loan service.

Budget inputs

Build the budget from scope, not guesses. Use one-time CAPEX for the website and branding, then separate launch collateral like brochures, pitch sheets, and referral packets. The model uses $8,000 for build and branding plus $3,000 for initial materials. For monthly testing, track vendor quotes, ad spend, and partner outreach hours by month.

Quote design, copy, and development separately.

Price local listings and profile setup.

Track paid tests by month.

Spend control

Keep the first version lean: one clear site, one intake path, and a small set of borrower education pages. Reuse content across landing pages and referral kits, and test paid media in small batches. Don’t cut disclosure or privacy work to save a few dollars; in loan services, fixing trust gaps later is usually more expensive.

Use one template across pages.

Reuse FAQs across channels.

Protect privacy and disclosures.

Year 1 math

The model lists performance-based marketing at 100% of revenue and referral partner commissions at 30% of revenue; with $325,000 Year 1 revenue, the quick math provided is $32,500 for marketing and $9,750 for referral commissions. That makes the launch budget front-loaded, so cash planning should separate setup cost from ongoing acquisition spend.

Office Setup And Equipment Startup Expense

Office budget

If you want a client-facing loan advisory office, plan for $27,500 in upfront CAPEX and $2,750 a month in operating costs. That covers the room, the gear, and the basics clients expect. A home office cuts the burn; a shared office sits in the middle; a polished office helps with in-person trust.

What it covers

This budget covers laptops or desktops, phones, printers, scanners, secure filing, advisor desks, a conference table, meeting-room furniture, signage, basic security equipment, and possible leasehold improvements. Use unit counts, vendor quotes, and room layout to estimate it. The model source is $15,000 for furniture and fixtures, $10,000 for IT hardware and software licenses, and $2,500 for security installation.

Laptops and phones for advisors

Secure storage for client files

Meeting space for borrower reviews

Keep it lean

Home-office setups are cheapest because they can avoid $2,500 rent, $150 utilities, and $100 supplies and maintenance. Shared offices reduce setup pain but still need a professional meeting area. Don’t skimp on security or filing; loan work handles bank statements, tax returns, ID, and business records, so weak storage is a bad trade.

Buy only needed seats first

Delay nonessential décor

Use modular furniture

Office choice by scenario

A home office fits early-stage, referral-heavy work. A shared office works when you need occasional client meetings and lower fixed cost. A client-facing office makes sense when you expect regular in-person loan reviews, because the monthly base is still $2,750 before payroll and marketing. That fixed cost matters fast.

Staffing Readiness And Training Startup Expense

Staffing Cash

Pre-opening staffing is a cash plan, not just a payroll line. For Year 1, budget $120,000 for the CEO or lead loan advisor and $80,000 for the senior loan advisor, or $200,000 total before later hires. Add founder draw planning, compliance training, sales training, background checks, and a payroll buffer before commission payouts start.

What It Covers

This cost covers hiring, onboarding, and readiness for CEO or lead advisor, senior loan advisors, processors, and admin support. Estimate it with headcount × salary × start month, plus training and checks. The key split is pre-opening setup versus ongoing payroll and commissions tied to closed loans.

Track salary by start month.

Separate training from payroll.

Keep commissions off startup cost.

Hire Timing

The later hires change the cash curve. A loan processing specialist starts in Month 13 at $60,000, and a marketing and business development manager starts in Month 13 at $70,000. An administrative assistant starts in Month 25 at $45,000. That timing keeps startup spend lower early, but it does not reduce the need for a payroll buffer.

Delay hires until loan volume justifies them.

Match staffing to closed-loan timing.

Keep admin work lean first.

Cost Control

Use pre-opening training for compliance, sales, and process quality, but keep recurring pay separate from startup CAPEX. The practical control is simple: hire the minimum staff needed to open, then add processors and admin help only after loan flow is steady. That avoids paying full teams before revenue from closed loans starts.