Biofeedback Therapy Clinic Owner Income: $228K Year 1 Case

Key Takeaways

Paid sessions, not booked visits, drive revenue.

Collected fee stays near $182 to $188.

Payroll and overhead set the break-even floor.

Owner pay depends on reserves and role.

Owner income$53k-$1.31MNet margin5%-39%Revenue for target pay≈$999kBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full Biofeedback Therapy Clinic model?

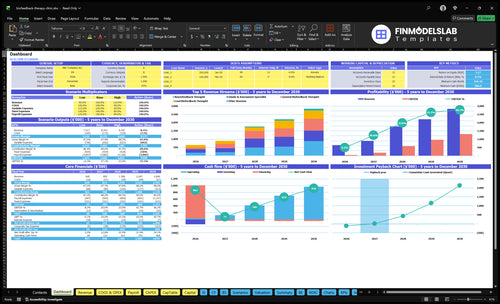

Yes — the Biofeedback Therapy Clinic Financial Model Template shows the dashboard, income outputs, assumptions, revenue build, payroll, operating expenses, startup costs, cash flow, and owner income scenarios. Year 1 revenue is $6.446M, operating profit is $1.075M, and potential owner compensation is $2.275M; open the model to test the assumptions.

What the model highlights

Owner income scenarios

Revenue, margin, cash flow

Paid sessions and runway

What profit margin can a biofeedback clinic produce?

A Biofeedback Therapy Clinic can earn solid margins, but the real driver is collected revenue and utilization, not the posted session price. For the setup math behind that, see How Much Does It Cost To Open And Launch Your Biofeedback Therapy Clinic? — the provided figures show $1.075M Year 1 operating profit on $6.446M revenue, or about 16.7%, and $158M on $284M by Year 5, or about 55.6%.

Margin drivers

Collected revenue sets profit.

Utilization drives session volume.

$3.525M Year 1 payroll weighs hard.

$84k monthly overhead stays fixed.

Cost load

80% marketing is a major drag.

25% payment processing cuts receipts.

10% consumables hit each visit.

15% equipment and software add more.

How much revenue can a biofeedback therapy clinic generate?

The Biofeedback Therapy Clinic can generate about $6,446k in Year 1 annual revenue, or $537k per month, and about $284M in Year 5 annual revenue, or $2,366k per month. That is revenue, not profit or owner income. Here’s the quick math: Year 1 assumes about 2,945 paid sessions per month at about $182 collected per session, and the real driver is room capacity, clinician schedules, packages, cancellations, and retention.

Year 1 Revenue Math

$6,446k annual revenue

$537k monthly revenue

2,945 paid sessions monthly

$182 collected per session

What Drives Revenue

Room capacity sets session volume

Clinician schedules cap bookings

Packages lift collected revenue

Retention cuts cancellation drag

Does a biofeedback clinic owner make more by treating patients or hiring clinicians?

For a Biofeedback Therapy Clinic, the owner usually keeps more cash in year one by treating patients, because less clinical revenue goes out in payroll. If the owner steps into the clinical-director role, that adds a $120k salary line, though distributions can still happen if the clinic stays profitable. Hiring clinicians helps the clinic scale, but it also raises payroll risk and makes supervision and quality control non-negotiable.

Owner treats

Year 1: 1 lead therapist

1 neurofeedback therapist

1 general therapist

1 intake specialist

Hire and scale

Year 5: 2 lead therapists

3 neurofeedback therapists

4 general therapists

2 intake staff plus 1 corporate wellness specialist

Biofeedback Therapy Clinic Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six levers that move owner income?

1

Session Volume

68-291/wk

More paid sessions lift revenue fastest; the model grows from 68 weekly in Year 1 to 291 weekly in Year 5, so this is the biggest swing in owner take-home.

2

Collected Fee

$182-$188

Each visit's collected fee sets the cash per session, and small price gains compound fast as volume rises.

3

Clinician Payroll

$353K-$890K

Labor is the largest cost block, so schedule fill and staffing mix drive margin more than almost anything else.

4

Direct Tech Cost

2.5%-2.0%

Consumables and software stay low, but every point saved here keeps more gross profit in the clinic as volume scales.

5

Fixed Overhead

$8.4K/mo

Lease, insurance, utilities, and admin set the monthly cash floor, so tight overhead is what protects owner income early on.

6

Cash Reserves

25mo

Minimum cash reaches $807K and payback takes 25 months, so owner pay needs to wait until reserves can cover the ramp.

Biofeedback Therapy Clinic Core Six Income Drivers

Paid Sessions And Utilization

Paid Sessions and Utilization

Booked visits are not the same as collected paid sessions. This model runs at about 2,945 paid sessions per month in Year 1, or 68 per week, then 1,258 per month in Year 5, or 291 per week. The source assumptions start at 650% utilization for lead biofeedback, 600% for neurofeedback, 550% for general biofeedback, and 750% for intake, so cancellations can cut revenue fast while payroll and rent still run.

Track the Paid Gap

Measure booked visits, completed visits, cancellations, and collected payments by service line. Here’s the quick math: paid sessions = booked visits minus cancellations and unpaid visits, then netted for collections. If the gap widens, gross margin and owner draw shrink even when the schedule looks full.

Track show rate by clinician.

Rebook cancellations the same day.

Hold cash for payroll and rent.

1

Average Collected Fee

Average Collected Fee

Average collected fee is the cash actually collected per paid session after discounts, insurance adjustments, denials, packages, and unpaid balances. In Year 1, the blended collected fee is about $182 per paid session across listed prices of $140 lead biofeedback, $200 neurofeedback, $120 general biofeedback, and $300 intake. That gap matters because listed price is not cash in the bank.

Here’s the quick math: if collections drop by $10 per paid session and volume is 2,945 sessions a month, monthly revenue falls by about $29,450. Year 5 only rises to about $188, so small collection leaks still hit owner pay. This driver sits between pricing and cash flow, and it decides how much room you have after payroll and overhead.

Protect Net Collections

Track gross charges, collected dollars, and collection rate by service line so you can see where denials, packages, or unpaid balances hit hardest. Measure the mix each month: lead biofeedback, neurofeedback, general biofeedback, and intake. If one service collects below plan, your blended fee slips even when booked visits stay flat.

Collected fee by session type

Denial and write-off rate

Discount and package mix

Days in receivables

Net cash collected per week

Run a simple control loop: verify eligibility before treatment, post claims fast, age receivables weekly, and review write-offs by practitioner and payer. The goal is not higher sticker price alone; it is a higher net realized fee per completed session, so more of each visit drops through to owner income.

2

Clinician Payroll And Staffing Model

Clinician Payroll Load

Hiring clinicians expands capacity, but it can shrink gross margin fast if wages or idle time outrun collected session revenue. The model states Year 1 payroll is $3,525k, while the named roles shown add to $600k ($120k + $90k + $70k + $45k + $275k). By Year 5, payroll reaches $890k. That gap matters because payroll hits cash every month, but owner pay only works when paid sessions cover it.

Track Paid Capacity, Not Headcount

Measure payroll per paid session, not just staff count. Separate owner labor from employee and contractor pay, then compare total clinician payroll to collected revenue and paid sessions. If a new hire adds idle hours faster than booked visits, margin drops and the owner’s draw gets squeezed.

Track payroll by role monthly

Match staffing to paid sessions

Flag idle time before hiring more

Split owner pay from clinic payroll

3

Equipment, Sensors, And Software

Equipment, Sensors, and Software Cost

Equipment, sensors, and software eat into cash before owner pay does. In this model, direct software licensing takes 15% of revenue in Year 1, then 14%, 13%, and 12% in Years 4 and 5, plus $300 per month for billing software. That cost tracks collected revenue, so weak utilization hurts twice: fewer dollars in and less room to cover tech.

Here’s the quick math: at 2,945 paid sessions a month and a $182 blended collected fee, revenue is about $535,990 monthly, so Year 1 licensing is about $80,399 plus billing software. If treatment rooms sit idle or the service mix shifts to lower-paid sessions, tech spend can outrun margin and cut the cash left for payroll and owner draw.

Track Tech Cost per Session

Track tech cost per paid session, not just the invoice. Use licensing % × collected revenue plus $300, then divide by paid sessions to see the real load on margin. A room that adds sessions should lower cost per visit; a room that adds hardware but stays empty raises cost per session and delays owner pay.

Paid sessions by room.

Collected fee per session.

License rate by year.

Billing software monthly fee.

Sensor uptime and maintenance days.

Service mix by treatment type.

If you add capacity, model the session count first and buy only what supports it. The goal is a lower tech cost per collected dollar, because the owner only pays themselves from what is left after licensing, software, and repairs. If sessions slow, freeze new equipment orders until utilization recovers.

4

Fixed Overhead And Admin Costs

Fixed Cost Floor

Fixed overhead is the cash floor the clinic must clear before owner pay feels safe. In this model, monthly fixed overhead is $84k, and it keeps running during slow weeks. That includes rent, insurance, software, supplies, and admin costs, so weak session volume can squeeze cash fast.

Here’s the quick math: with Year 1 payroll included, break-even is about 55 paid sessions per week. If paid sessions fall below that level, the owner has less room for draws, taxes, and reserves.

Measure the Overhead Run Rate

Track fixed costs by month, not by year. Separate the steady items like the $5k clinic lease, $800 utilities, $500 maintenance and cleaning, $12k malpractice and liability insurance, $300 billing software, $200 supplies, and $400 professional development so you can see the real cost floor.

Track paid sessions weekly

Watch cancellations and no-shows

Hold reserves for slow weeks

Delay owner draws until covered

If booked visits look strong but collected paid sessions lag, the same overhead is spread over fewer visits. That pushes profit down and makes owner income less stable, even before revenue drops hard.

5

Owner Pay Structure And Reserves

Owner Pay and Reserves

The owner’s take-home changes based on whether they treat patients, run operations, repay debt, or reinvest cash. If the owner serves as Clinic Director, the source model includes a $120k salary. Year 1 operating profit after payroll is $1,075k, and the model shows $2,275k as potential owner compensation before tax and reserves.

Net income is not the same as distributable cash. Keep reserves for cancellations, payroll timing, equipment replacement, and marketing tests, or the owner can overdraw the clinic even when profit looks strong on paper.

Protect the Owner Draw

Set owner pay after cash reserve checks, not just after profit. Track collected revenue, payroll timing, debt service, and planned reinvestment each month so you know what is truly available. One clean rule: pay yourself from surplus cash, not from booked visits.

Separate salary from profit draws.

Hold cash for cancellation dips.

Protect payroll and vendor timing.

Review the reserve balance before any extra draw or equipment buy. If marketing tests or replacement costs are coming up, keep that cash inside the clinic until the spend is done.

6

Biofeedback Therapy Clinic Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income rises as session volume, fees, and provider count increase. This clinic has low direct costs, so small gains in utilization can lift owner pay fast.

Compare ramp-up, scaled, and mature clinic owner pay.

Scenario

Low CaseRamp-up

Base CaseScaled multi-provider

High CaseMature clinic

Launch model

This is the lower owner-income path built on Year 1 ramp-up volume and lean staffing.

This is the modeled core case with Year 3 volume, more therapists, and steadier clinic utilization.

This is the stronger owner-income path if the clinic reaches Year 5 capacity and keeps filling sessions.

Typical setup

Year 1 ramp-up with 68 paid sessions a week at a $182 collected fee, one therapist in each core role, and the owner still covering oversight and cash control.

Year 3 uses 182 sessions a week at a $187 collected fee, a wider mix of providers, and one corporate wellness specialist on a more stable schedule.

Year 5 reaches 291 sessions a week at a $188 collected fee, with two lead therapists, three neurofeedback therapists, four general therapists, and a mature back office.

Cost drivers

Session volume

collected fee per visit

therapist mix

intake staffing

fixed clinic overhead

Higher session density

added therapists

intake and billing labor

marketing spend

low consumables and licensing

Fuller therapist schedules

added corporate wellness work

lower ad spend share

fixed overhead absorption

low consumables and licensing

Owner income rangeBefore owner reserves

$2.275MOwner pay floor

$8.679MModeled owner pay

$170MUpside pay case

Best fit

Use this to test whether the clinic can support the owner through launch and the first fill-up phase.

Use this as the main planning case for a clinic that is open, staffed, and running at a steady pace.

Use this to test upside if referrals, corporate wellness, and therapist capacity all land well.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

In the Year 1 model, potential owner compensation is $2275k before tax and reserves if the owner also takes the $120k Clinic Director role That includes $1075k operating profit after payroll The number changes if the owner hires a director, holds more cash, repays debt, or misses the 68 paid sessions per week plan

In this model, break-even is about 55 paid sessions per week in Year 1 when the $120k Clinic Director salary is included The clinic plans about 68 paid sessions per week, so the cushion is real but not huge If cancellations rise or collections slow, owner distributions should wait

Not from this model alone The assumptions use collected session revenue, not a promised payer contract Year 1 works at about $182 collected per paid session across lead biofeedback, neurofeedback, general biofeedback, and intake visits Profit depends on actual collections, denials, discounts, patient balances, and payment timing

Paid sessions, collected fee, payroll, utilization, overhead, and owner pay structure drive the result Year 1 revenue is $6446k, payroll is $3525k, and fixed overhead is $84k per month If utilization drops below plan, the clinic still carries rent, insurance, software, and staff costs

The higher-pay model is usually a disciplined multi-provider clinic, but only after demand is proven The model grows from 68 paid sessions per week in Year 1 to 291 in Year 5 That supports $284M revenue, but it also requires $890k payroll, quality control, admin systems, and cash reserves

About the author

Julian Fox

Business Idea Researcher

Julian Fox is a business idea researcher at Financial Models Lab who focuses on revenue and profit basics for simple business planning. He helps non-finance readers compare business ideas by breaking down business model overviews and explaining how small businesses operate day to day. His work is grounded in real-world decisions and makes business plans easier to understand.

Choosing a selection results in a full page refresh.