How Much Cistern Cleaning Owners Can Make: $690K Year 5 EBITDA

You’re planning owner pay before the route is fully dense, so cash gets tight early This five-year model shows $90,000 planned founder salary, EBITDA moving from -$168,000 in Year 1 to $690,000 in Year 5, and breakeven around Month 33 It covers revenue drivers, direct costs, overhead, reserves, and owner take-home, but not taxes, guaranteed earnings, or employee wage comparisons

Owner income$90k/yrNet margin76.5%Revenue for target pay$24.2k/moBusiness difficultyHard

Want to calculate owner income from cistern cleaning?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will change with jobs, mix, staffing, fuel, fees, financing, and reserves.

Want to see the six cistern cleaning income drivers?

1

Average ticket

$79-$350

A bigger mix of $350 cleanings, $79-$250 monthly plans, and $45 add-ons lifts take-home fastest.

2

Completed jobs

765%

More cleanings push Year 1 contribution before payroll hard, so utilization is what turns revenue into cash.

3

Recurring accounts

$79-$250/mo

Monthly accounts smooth cash flow, lower CAC over time, and make owner pay less dependent on one-off jobs.

4

Labor efficiency

5 FTE

With founder pay at $90K and technicians at $55K, every idle hour cuts profit fast.

5

Route density

Rural

Rural drive time burns labor and fuel, so tighter routes protect margin without raising prices.

6

Fixed overhead

$3.35K/mo

The fixed base is small, but Month 33 breakeven and a $285K cash need mean reserves still matter.

How do you check owner income in the Cistern Cleaning forecast?

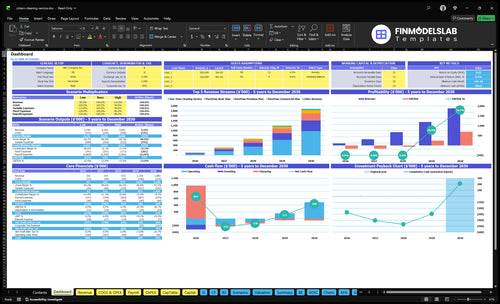

If you're stress-testing owner pay, the dashboard in the Cistern Cleaning Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions. It also runs $45, $79, $129, $250, and $350 price points, direct costs from 235% to 200%, payroll from $165,000 to $520,000, and EBITDA from -$168,000 to $690,000. Open the model.

Owner-income model highlights

Founder take-home is tracked

Revenue, margin, cash split

Assumptions: $45 to $350

Payroll ramps $165k to $520k

EBITDA: -$168k to $690k

Can a cistern cleaning business make money without the owner doing every job?

Yes, Cistern Cleaning can run without the owner doing every job, but the tradeoff is higher payroll plus training, scheduling, insurance, and quality-control costs. In this model, total payroll rises from $165,000 in Year 1 to $520,000 by Year 5, with one service technician at $55,000, a founder salary of $90,000, an operations manager at $65,000 in Year 2, and sales support at $50,000 in Year 3. Time freedom improves later, but early take-home pressure is real, and EBITDA turns positive only after route volume and pricing catch up.

Owner-off model

Field labor drops for the owner

Payroll still rises fast

Training and QA add cost

Scheduling gets more complex

Money pressure points

$165,000 payroll in Year 1

$520,000 payroll by Year 5

EBITDA turns positive later

Founder take-home is tighter early

How much revenue can a cistern cleaning business make?

A Cistern Cleaning business can generate revenue from $350 one-time cleanings, $79 basic monthly plans, $129 premium monthly plans, $250 commercial monthly plans, and $45 filter add-ons, but the real ceiling depends on route density, recurring accounts, commercial mix, and seasonal demand; start with What Is The Most Critical Metric For Cistern Cleaning's Success? before turning customer acquisition into a forecast.

Revenue Inputs

Charge $350 for one-time cleaning

Offer $79/month basic recurring service

Offer $129/month premium recurring service

Add filters at $45 per sale

Growth Math

Price commercial plans at $250/month

Grow marketing from $15,000 to $100,000

Improve CAC from $150 to $80

Separate revenue from owner income, EBITDA, and cash

How many cistern cleaning jobs do you need to pay yourself?

If you want to pay yourself a $90,000 founder salary, Cistern Cleaning needs about 28 jobs a month at a $350 one-time ticket to cover salary alone. Each job contributes about $268 before fixed costs and payroll, and Year 1 payroll, overhead, and marketing total $220,200, which points to about 69 jobs a month before capex. Add $138,000 in launch capex, and the first-year cash need goes much higher; this is planning math, not a promised paycheck.

Salary math

$90,000 salary equals $7,500/month

$350 ticket adds about $268

28 jobs/month covers salary only

More jobs help spread fixed costs

First-year cash

Year 1 costs total $220,200

That needs about 69 jobs/month

$138,000 capex raises cash need

Plan for cash, not just revenue

Key Takeaways

Higher average ticket lifts revenue only if bookings hold.

Empty calendar slots do not pay the owner.

Dense routes cut drive time and protect margins.

Recurring work stabilizes volume, but reserves still matter.

Compare lean, base, and high cistern cleaning owner-income scenarios

Owner income scenarios

Owner income here depends on route density, staffing, and the shift from one-time jobs to recurring service plans. Early cash burn is heavy, then margins improve as breakeven nears Month 33.

Compare launch, breakeven, and mature-case owner income.

Scenario

Low CaseCash-heavy launch

Base CaseBreakeven build

High CaseScaled route density

Launch model

This is the slower ramp case, where the founder pay stays fixed but business earnings stay negative through the early build.

This is the modeled operating case, with the founder pay intact and the business moving toward breakeven around Month 33.

This is the stronger earnings path, where higher route density and recurring work support a much better Year 5 result.

Typical setup

The model is still in launch mode, with $165,000 payroll, $15,000 marketing, 235% direct cost load, and $138,000 launch capex while service volume is still thin.

The model is past launch, with $410,000 payroll, $50,000 marketing, 218% direct cost load, and breakeven approaching Month 33.

The model is scaled, with $520,000 payroll, $100,000 marketing, 200% direct cost load, and Year 5 EBITDA of $690,000.

Cost drivers

Founder salary $90,000

payroll $165,000

marketing $15,000

direct cost load 235%

launch capex $138,000

Founder salary $90,000

payroll $410,000

marketing $50,000

direct cost load 218%

breakeven near Month 33

Founder salary $90,000

payroll $520,000

marketing $100,000

direct cost load 200%

scaled route density

Owner income rangeBefore owner reserves

$90,000Launch burn

$90,000Near breakeven

$90,000Upside case

Best fit

Use this to stress-test early cash needs and a slower-than-planned sales ramp.

Use this for a working plan if you expect steady growth and breakeven near Month 33.

Use this to test a larger route network and stronger recurring demand.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Cistern Cleaning Core Six Income Drivers

Average Ticket

Average Ticket

Average ticket is the revenue earned per completed stop. In this business, that runs from $79 for basic recurring service to $350 for a one-time cleaning, with $129 premium recurring, $250 commercial recurring, and a $45 filter add-on. If labor hours and close rate hold, a higher ticket lifts revenue and owner pay.

Here’s the catch: bigger tanks, harder access, sanitation add-ons, and commercial accounts can raise the ticket, but only if the extra work is priced in. If setup time, wastewater handling, or callbacks stretch the job, the higher price may not improve margin. The clean rule is simple: price only helps when time stays in line.

Raise Ticket Without Hurting Margin

Track revenue per stop, labor hours per stop, and ticket by service type. Split pricing by tank size, access difficulty, sanitation work, and add-ons so a bigger job actually pays for the extra time. If a $45 add-on or a premium plan adds too much labor, it can lower owner income even when the invoice looks better.

Log ticket by job type

Price for setup and access

Count callbacks as extra labor

Test raises against booking rate

Use the mix on purpose: one-time cleaning at $350 can pull revenue fast, while recurring plans at $79, $129, or $250 build steadier cash flow. The goal is not just a higher sticker price; it’s a higher gross profit per stop.

Labor Efficiency

Labor Efficiency Drives Owner Pay

Labor efficiency is the gap between who does the cleaning and what the business can keep for the owner. If the founder does tank cleaning and supervision, payroll stays lower and the $90,000 founder salary is easier to support; once technicians are hired at $55,000 per FTE, margin has to cover more cash payroll. One line says it all: more crew only helps if jobs fill the schedule.

The model grows from 1 FTE in Year 1 to 5 FTEs in Year 5, so the key inputs are labor hours per job, jobs per tech, travel time, callback rate, and owner time spent cleaning versus managing. Owner-operated work can save payroll early, but it also caps scale. Crew-based growth can free the founder’s time, but only if training, safety controls, and quality checks keep rework low.

Track Labor Hours, Not Just Headcount

Measure labor cost per completed job, jobs per technician per month, and callback rate. If labor hours creep up on large tanks, hard access, or sanitation add-ons, owner take-home drops fast because payroll rises before revenue does. The useful question is simple: does each added technician create enough completed work to pay for their $55,000 salary and still leave profit?

Set a standard service time for each tank type, then compare it to actuals every month. If the owner is still cleaning most jobs, keep cash focused on margin and schedule density. If technicians take over, document steps, test quality, and watch safety. Empty crew time is expensive; paid, repeatable work is what turns labor into owner income.

Recurring Customers

Recurring Customers

Recurring residential, farm, commercial, and property-management accounts make income steadier because they smooth job volume and lower customer acquisition cost (CAC). In the model, CAC improves from $150 in Year 1 to $80 in Year 5, while the mix shifts toward recurring and commercial work and one-time cleaning share falls from 250% to 120%. That supports cash flow, payroll, and the owner’s draw.

Do not treat every plan as a monthly job. Cleaning frequency still depends on tank use, water quality, and local conditions, so the real inputs are active accounts, service scope, renewal rate, and booked visits. If the scope matches the system, recurring work reduces sales pressure and makes profit less jumpy month to month.

Track Repeat Work by Segment

Track active recurring accounts, visit cadence, CAC, and cancellations. Compare booked visits with billed visits, because the plan only helps if it converts into paid service. One clean line: recurring work is cash flow, not a guarantee.

Price by customer type and service scope. Commercial and property-management accounts should cover extra admin, scheduling, and documentation. Test which accounts stay on plan after 90 days, then keep the ones that support margin and owner pay.

Equipment, Overhead, And Reserves

Equipment, Overhead, and Reserves

$138,000 in launch capex and $3,350 in monthly fixed overhead eat into early owner pay before the business has steady cash flow. That total includes cleaning gear, service vehicles, office and IT setup, lab equipment, safety gear, and software, so this driver is really about how much cash stays inside the company, not how much the owner can draw.

Here’s the quick math: if repairs, insurance, chemicals, protective gear, and marketing are not built into job pricing, margin gets thin fast. The model’s minimum cash need reaches $285,000 around Month 38, so reserve cash is not take-home income. Cash in the bank keeps the crew working; it does not pay the owner twice.

Price for Reserves, Not Just Service Time

Track each job’s full cost stack: labor, drive time, chemicals, PPE, insurance, repairs, and marketing. Then test prices against actual gross margin, not just the cleaning bill. If a job looks profitable only before overhead, it is not helping owner income.

Set a reserve target tied to monthly overhead: $3,350 plus growth cash, then hold it separate from owner draws. Watch cash runway each month and compare it with the $285,000 minimum cash need by Month 38. What this estimate hides: one bad quarter can wipe out pay if reserves are too thin.

Price recurring jobs with overhead included.

Ring-fence reserve cash from draws.

Review repair and insurance spend monthly.

Completed Jobs Per Month

Completed Jobs Drive Cash

Completed jobs are the real income driver because leads only matter if they turn into paid cleanings. In the Year 1 model, about 69 one-time jobs a month at $350 each means roughly $24,150 in monthly revenue, enough to cover payroll, fixed overhead, and marketing before capex break-even around Month 33.

Capacity is not just booking volume. Travel, setup, tank access, cleaning time, testing, documentation, and gaps in the schedule all cut utilization. Empty calendar slots don’t pay the owner. Missed appointments and long drive times hit take-home income fast because they lower the number of paid stops per month.

Track Paid Stops, Not Leads

Measure booked jobs, completed jobs, and no-shows each week, then compare them with drive time and service time per stop. If completion rate slips, revenue drops even when lead flow looks healthy. The key question is simple: how many paid cleanings can one crew finish in a month without wasting hours between jobs?

Track jobs per route zip.

Track miles and drive minutes.

Track no-shows and callbacks.

Track service time by tank type.

If one-day routes fill but completion falls, tighten scheduling, cluster stops, and confirm tank access before dispatch. That keeps labor productive, protects margin, and helps the owner turn more of each booked day into cash they can actually pay themselves.

Route Density

Dense Routes

Route density is how many paid jobs you can complete in a tight area without wasting time in windshield time, fuel, and vehicle wear. In this model, fuel and per-service maintenance are 60% of revenue in Year 1 and improve to 50% by Year 5, so every scattered stop cuts the cash left for payroll, overhead, and owner pay.

The inputs are simple: paid stops per route, drive miles, service area mix, and job spacing by zip code, property type, and water system need. Rural and semi-rural demand can be strong, but if jobs are spread out, the ticket price can look good while margin leaks away in unpaid drive time.

Cluster Every Stop

Track drive minutes per paid job and fuel plus maintenance as a percent of revenue. Here’s the quick math: if route costs stay near 60% of revenue early on, only 40% is left before fixed overhead and owner draw. Denser routes push that spread the right way.

Price distant work carefully, or skip it. Cluster jobs by zip code, tank type, and service need, then schedule same-day stops together. That cuts dead miles, reduces callbacks from rushed timing, and protects the owner’s take-home income when demand is there but the map is messy.