Healthcare Real Estate Developer Owner Income: $220K Salary Plus Upside

A healthcare real estate development owner can plan around a $220K salary in this researched model, but true take-home depends on when cash is available for distributions The model shows EBITDA of -$18080M in Year 1 and -$18597M in Year 2, then $36107M in Year 3 as sales start to clear Breakeven lands in Month 21, payback in Month 30, and minimum cash falls to -$21749M in Month 20 Those figures are planning assumptions, not guaranteed healthcare property developer earnings

Owner income$220KNet margin4.4%Revenue for target pay$92.8MBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the model?

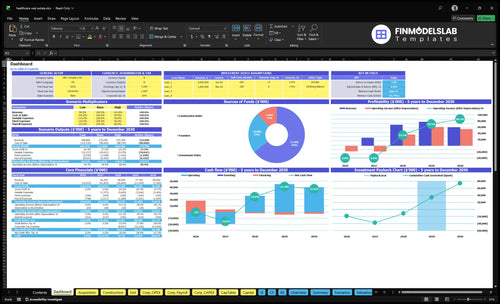

The dashboard in Healthcare Real Estate Development Financial Model Template shows owner pay, cash trough, payback, IRR, ROE, and EBITDA by year, plus assumptions, budget, timing, expenses, financing, and reserves. Open the model to see the full payout path.

Owner-income model highlights

Owner pay is visible

Cash trough by month

Scenario tabs drive returns

How do healthcare real estate development companies make money?

Healthcare Real Estate Development companies make money mainly by selling completed medical properties, not by recurring salary-like income. In this model, upside comes from seven assets with $243M of purchase cost and a $685M construction budget, with sales planned from Month 21 through Month 50; for startup cost context, see How Much To Start Healthcare Real Estate Development Business?. Development management fees can smooth cash before sale if contracted, but the provided model shows no separate fee revenue line.

Revenue streams

Sell completed healthcare properties

Earn project profit at closing

Charge acquisition fees if contracted

Collect development fees if separately agreed

Cash timing

Sales start in Month 21

Final planned sale in Month 50

Lease-up supports buyer pricing

Financing and reserves protect liquidity

How many healthcare real estate projects does an owner need to make a good income?

There’s no magic project count here. In Healthcare Real Estate Development, the source case uses 7 owned projects, with acquisitions from Month 3 to Month 24 and sales from Month 21 to Month 50, so early income depends on the $220K owner salary while project cash stays negative. More projects can lift fee opportunities and upside, but they also raise payroll, guarantees, cash troughs, and execution risk.

Lean owner-led pipeline

7 projects can work in the case.

Acquisitions run Month 3 to 24.

Sales lag to Month 21 to 50.

$220K owner pay bridges early losses.

Staffed platform tradeoff

More projects mean more fee upside.

Payroll can reach $710K to $13M.

Cash troughs get deeper with scale.

Payback lands around Month 30.

What salary can a healthcare real estate development owner pay themselves?

If the owner is filling the Principal Developer role in Healthcare Real Estate Development, the model points to a $220K annual salary as the target pay level. But cash is tight early: EBITDA is -$18,080M in Year 1, -$18,597M in Year 2, and minimum cash bottoms at -$21,749M in Month 20, so pay has to stay separate from draws, distributions, and reinvested profit.

Target owner pay

$220K fits the Principal Developer role.

Use salary first, then draw or distribution.

Test pay against recurring fees and debt service.

One line: pay the role, not the equity.

Cash risk checks

Monthly overhead is $283K plus payroll.

Minimum cash hits -$21,749M in Month 20.

Check pipeline quality before raising pay.

Keep reserves ahead of owner distributions.

Want the six income drivers?

1

Project Margin

7.45x ROE

Tighter build costs get the model to Month 21 breakeven and support the 4.4% IRR path, so more Year 3 EBITDA becomes distributable cash.

2

Capital Stack

-$21.7M

The -$21.7M cash trough makes financing terms decisive, because structure decides how much distributable cash survives before revenue scales.

3

Deal Pipeline

$92.8M

A cleaner pipeline keeps the $92.8M basis moving, which shortens idle time and brings distributable cash in sooner.

4

Tenant Credit

Y4 $61.0M

Creditworthy tenants support steadier rent and help Year 4 EBITDA reach $61.0M, which lifts distributable cash.

5

Fee Terms

30 mo

Fee timing controls the 30-month payback, so weak development fees delay owner distributable cash.

6

Owner Load

$220K

The $220K principal salary and fixed overhead pull cash out each month, so lean staffing leaves more EBITDA available to distribute.

Healthcare Real Estate Development Core Six Income Drivers

Deal pipeline and project volume

Deal Pipeline

The owner’s income here depends on how many projects are live and when each one sells, not just raw deal count. This model has 7 owned projects, with acquisitions starting from Month 3 to Month 24, construction lasting 10 to 22 months, and sales landing from Month 21 to Month 50.

That timing drives fee chances, sale proceeds, and capital recycling. One clean rule: more volume only helps if the timeline stays staggered. If tenant demand, financing access, or execution slips, cash comes in later, and owner pay gets pushed out even if the pipeline looks full.

Track Start-to-Sale Timing

Measure each deal by acquisition month, construction length, and sale month. Here’s the quick math: a project that starts early but slips on build or lease-up can delay cash by months, while a steady pipeline keeps proceeds rolling in across Month 21 to Month 50.

Watch pipeline count, tenant demand, financing access, and execution timing. The best signal is not more deals; it’s more on-time closings. If one project stalls, the rest of the stack has to carry owner income until sale cash resets the cycle.

1

Development fees and revenue structure

Development Fee Revenue

Development fees can smooth owner income before a project stabilizes or sells. The source model does not give a separate fee rate, so treat it as an editable input, not a fixed benchmark. Test fee revenue against the $928M development basis, milestone timing, and staff capacity, because slower draws delay cash and raise pressure on working capital.

Here’s the quick math: if fees are tied to basis, every 1 percentage point on $928M equals $9.28M in gross fees before overhead. That does not equal owner pay. The owner’s take-home is fee revenue minus payroll, consultants, insurance, travel, legal, marketing, and reserves.

Track Fee Yield and Cash Collection

Measure fees by project, milestone, and delivery type: owned deals versus third-party work. Third-party projects can bring steadier fee cash, while owned projects may defer cash until sale. Track fee percent on basis, billed vs. collected, and monthly overhead so you can see what is left for owner draws.

Use a simple control list: fee rate, $928M basis, billing dates, payroll, consultant spend, and reserve target. If overhead rises faster than collections, gross fees can look strong while owner income stays thin. That gap matters most when project timing slips and fee cash lands later than planned.

Fee rate on basis

Milestone billing dates

Collected cash vs billed

Overhead by month

Reserve balance

2

Project margin and cost control

Margin Discipline

For healthcare real estate, owner income rises when purchase price, construction budget, tenant improvements, soft costs, contingency, and schedule stay on plan. The disclosed base is $243M of purchase cost plus $685M of construction, or $928M before other project costs. Every overrun hits distributable cash first, then reserves, so budget control is profit control.

The biggest jobs carry the most pressure: Surgery Block ($180M), Health Plaza ($150M), and Medical Hub ($125M). If scope changes or delays stack up, carry costs rise and the sale gets harder to time, which pushes owner pay out later and can shrink the cash available at close.

Control the Variance

Track budget vs. committed vs. paid every week, plus months slipped on each project. Use the disclosed $928M base to size risk: a 1% miss is about $9.28M on the disclosed base alone. Budget misses do not wait for sale day; they show up first as weaker cash flow.

Measure these inputs on every deal:

Purchase price

Construction budget

Tenant improvements

Soft costs

Contingency

Schedule delay

One clean rule: if committed cost is rising faster than expected exit value, owner draw gets squeezed before the project is sold.

3

Leasing and healthcare tenant credit

Healthcare tenant credit and lease-up

Lease-up and tenant credit shape value, loan terms, and sale timing more than they shape day-to-day owner income. In this owned development model, rent is not direct owner pay unless the company keeps the asset or earns value-based fees, so the real income driver is how fast strong medical tenants support a better exit between Month 21 and Month 50.

Here’s the quick math: stronger leases can lower hold risk and help close sooner, while weak credit can delay sale proceeds and push owner distributions beyond the Month 30 payback point. What this hides is simple: if the rent roll looks good but the tenant is weak, the exit can still slip and tie up cash longer than planned.

Track lease quality, not just rent

Measure signed lease rate, tenant credit, lease term, and how many units are still unleased. The owner should care about the part that changes valuation and financing, not just headline rent. A clean lease-up profile can support a faster sale and better cash return; a weak one can stall distributions and keep capital trapped.

Track lease-up by project monthly.

Flag weak tenants early.

Stress-test sale timing past Month 30.

Document rent roll and credit support.

Use tenant quality as a gate before assuming exit cash. If lease-up is thin or credit is shaky, forecast a later sale and slower owner draw. That keeps the plan honest and protects income from being built on rent that may not convert into sale proceeds.

4

Financing and equity participation

Financing Terms

In healthcare real estate development, debt terms, investor splits, equity contribution, guarantees, interest costs, and promote structure decide how much of the sale proceeds reach the owner. More leverage can lift upside, but it can also delay or block distributions if debt service and lender controls absorb the cash first.

The source model shows a negative cash trough in Month 20, so timing is part of the economics, not a side note. The reported 44% IRR and 745% ROE are investor-return measures after financing and timing assumptions, not simple company earnings. Here’s the quick math: financing can raise return on equity, but it can also turn a paper gain into a cash squeeze.

Track the Capital Stack

Model the full waterfall before you start: purchase cost, construction draws, debt amount, interest rate, equity split, guarantee cap, exit month, and promote hurdle. If the sale slips by 3 to 6 months, or the reserve runs short, owner pay can move from profit draw to waiting on lender paydown.

Track monthly cash balance.

Test sale delay sensitivity.

Cap guarantees where possible.

Protect an interest reserve.

One clean rule: don’t read project profit as owner income until the debt and investor waterfall is clear. If financing costs or preferred returns consume early cash, the owner may get paid last, even on a strong exit. That’s why capital structure has to be managed with the same care as site selection and construction.

5

Overhead, reserves, and owner role

Overhead, reserves, and owner pay

In healthcare real estate development, fixed overhead of $283K per month is what turns project profit into cash the owner can actually keep. With payroll rising from $710K to $13M per year, the business needs enough spread after staff, legal, travel, and financing work. The $220K principal developer salary is pay for active work, not passive profit.

Here’s the quick math: if overhead stays heavy and projects slip, owner draw gets pushed out even when gross profit looks fine. Reserves matter because the model shows a Month 20 cash trough of -$21749M, so cash has to cover due diligence, site visits, legal work, and gaps before the next sale closes.

Track overhead before owner draw

Measure monthly fixed overhead, payroll run rate, and cash reserve days before taking distributions. The owner should separate salary for development work from profit share, then forecast cash after each project close. If overhead rises faster than project fees or sale timing slips, take-home pay falls even when the pipeline looks strong.

Track cash after each project close.

Cap travel, legal, and diligence spend.

Keep reserve cash for sale delays.

Pay salary only for active work.

6

Build lean, base, and high healthcare property developer income scenarios

Owner income scenarios

Owner income shifts with sale timing, fee load, and how fast the seven owned projects reach breakeven. Early losses are heavy, so delays cut take-home first.

Low, base, and high views show how timing and overhead change owner take-home.

Scenario

Low CaseLow Case

Base CaseBase Case

High CaseHigh Case

Launch model

The low case keeps owner income thin while projects slip and cash stays tied up.

The base case follows the modeled path with owner pay improving as the portfolio clears breakeven.

The high case lifts owner income if sales close faster and overhead stays controlled.

Typical setup

Sales run late, reserves stay high, and the seven owned projects absorb cash before distributions start.

Seven owned projects move through the plan, Month 21 reaches breakeven, and the owner draws the $220k salary with limited early distributions.

Projects sell sooner, fees run leaner, and stronger EBITDA supports larger distributions after the salary base.

Cost drivers

sale timing

reserve build

payroll growth

fixed overhead

legal and brokerage fees

seven owned projects

Month 21 breakeven

$220k owner salary

fixed overhead

payroll ramp

faster sales

lower fee load

controlled overhead

stronger EBITDA

earlier cash recovery

Owner income rangeBefore owner reserves

Under $220kLow case

$220k salaryBase case

$220k plus distributionsHigh case

Best fit

Use this to stress delays and a longer wait for distributions.

Use this as the main planning case for lender, investor, and cash-flow work.

Use this to test a fast-exit path where higher revenue still has to beat delays and project costs.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.