How Much Mobile Laser Tag Owners Make: $60K Pay Plus Profit

You’re weighing a mobile party business where weekends, weather, and staff can make or break pay This page covers $60,000 modeled owner pay, revenue versus profit, margins, operating costs, reserves, and scenario assumptions for a US mobile laser tag rental business

Owner income$60kNet margin40%Revenue for target pay≈$30.6k/moBusiness difficultyHard

Want to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, labor, overhead, marketing, debt, reserves, and pay goals.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the six main income drivers?

1

Bookings

5 mo

More booked events spread the fixed base faster, and Year 1 demand is still 70% birthday parties.

2

Event Price

$315-$625

Birthday, corporate, and community pricing sets revenue per job at about $315, $625, and $450.

3

Event Hours

1.75-4.0h

Longer event blocks and the 0.5-hour add-on lift revenue per stop without adding a new sale.

4

Direct Costs

72.5%

Keeping equipment, fuel, and payment fees in check protects the 72.5% Year 1 contribution margin.

5

Labor Load

1.75-5.25 FTE

Labor rises from 1.75 full-time equivalents (FTE) to 5.25, so hiring too early can wipe out booking gains; the fixed base is $23,700.

6

Lead Cost

$60 CAC

A $12,000 launch budget and $60 customer acquisition cost (CAC) set how fast paid leads turn into booked events.

How many mobile laser tag bookings do I need to pay myself?

If you want to pay yourself from Mobile Laser Tag, there isn’t one universal booking count. Using target-pay math, a birthday party at $315 brings about $228 of contribution, so $4,850 of monthly overhead plus $5,000 of owner pay means about 43 birthday bookings a month. A $625 corporate event needs far fewer bookings, but the real answer still depends on weekend capacity, setup time, travel radius, cancellations, and add-ons.

Birthday booking math

$315 revenue per birthday party

$228 contribution per booking

$4,850 monthly overhead

43 bookings cover owner pay and overhead

What moves the number

$625 corporate events need fewer bookings

Weekend slots cap monthly volume

Setup time cuts booking capacity

Cancellations and add-ons change pay fast

What costs affect mobile laser tag owner income?

For Mobile Laser Tag, owner income gets squeezed fast because Year 1 direct and variable costs total 275% of revenue, so the model can lose money before fixed overhead is paid. Those costs include 8% equipment maintenance and consumables, 12% coordinator variable pay, 5% fuel and logistics, and 25% processing; see How Much Does It Cost To Open The Mobile Laser Tag Business?. Fixed overhead adds $1,975/month, and payroll includes a $60,000 owner salary plus added staff.

Year 1 cost load

275% of revenue

8% maintenance and consumables

12% coordinator variable pay

5% fuel and logistics

Fixed and startup cash

25% processing

$1,975/month fixed overhead

$60,000 owner salary

$83,000 capex

Can a mobile laser tag business become full time?

Yes, Mobile Laser Tag can support a full-time owner in the model: $60,000 owner pay starts at launch, breakeven lands in Month 5, and payback is 12 months. Growth depends on multi-event weekends, schools, camps, corporate events, and community bookings; a 0.5 FTE lead coordinator in Year 1 lifts capacity, but extra staff lowers per-event cash margin if volume doesn’t keep up.

What makes it work

$60,000 owner pay from launch

Month 5 breakeven in the model

12-month payback period

0.5 FTE lead coordinator in Year 1

What drives risk

Needs multi-event weekends

Needs schools and camps

Needs corporate and community bookings

Hiring helps capacity, but can hurt margin

Key Takeaways

More completed bookings spread the $1,975 monthly overhead.

Pricing must cover travel, duration, and add-ons.

Capacity gains come from tight routing and slot control.

Equipment, staffing, and seasonality shape owner cash.

Compare lean, base, and high-volume owner-income scenarios

Owner income

Owner income shifts fast here because booking mix, add-ons, staffing, and marketing efficiency move EBITDA. The same $60,000 salary can sit inside very different cash outcomes.

Low, base, and high owner income cases for a mobile laser tag operator.

Scenario

Low CaseLow

Base CaseBase

High CaseHigh

Launch model

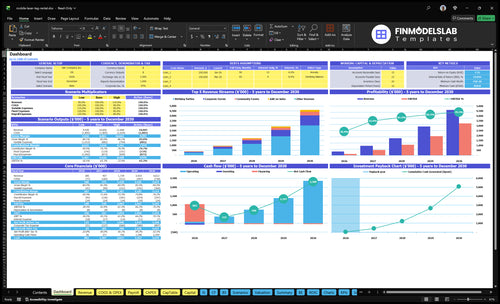

The first-year case models about $367,000 in revenue and $148,000 in EBITDA, with a $60,000 owner salary.

The Year 3 case models about $1.694 million in revenue and $1.062 million in EBITDA, with a $60,000 owner salary.

The Year 5 case models about $4.538 million in revenue and $3.243 million in EBITDA, with a $60,000 owner salary.

Typical setup

Birthday parties drive 70% of bookings, add-ons are 30%, average party time is 1.75 hours, CAC is $60, and staffing stays lean.

Birthday parties fall to 60% of bookings, corporate events rise to 20%, community events reach 15%, add-ons hit 40%, and staffing is more built out.

Birthday parties drop to 50% of bookings, corporate events rise to 30%, community events reach 25%, add-ons hit 50%, and support staff is fully in place.

Cost drivers

Birthday-party mix

add-on sales

CAC

coordinator pay

fuel and logistics

Corporate mix

community mix

add-on sales

coordinator staffing

payment fees

Corporate mix

community mix

add-on sales

staffing scale

marketing spend

Owner income rangeBefore owner reserves

$60,000 salarySalary only

$60,000 salary + drawsSalary and draws

$60,000 salary + larger drawsLarger draw case

Best fit

Use this to test the launch year when bookings are still birthday-led and cash is tight.

Use this as the core case once the mix shifts toward corporate and community events.

Use this to test upside only if growth, reserves, taxes, debt, and reinvestment stay covered.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; actual owner take-home depends on cash after reserves, taxes, debt, and reinvestment.

Mobile Laser Tag Core Six Income Drivers

Booking volume

Booking Volume

Booking volume is the biggest owner-income lever because most fixed costs are already committed. With $1,975/month in fixed overhead, every extra completed event helps cover the same base cost and lifts profit; weak booking volume leaves the owner paying the same overhead with less cash left to draw.

Track bookings per month, completed events, cancellation rate, and weekend slots. Here’s the quick math: a $12,000 Year 1 marketing budget at $60 CAC implies 200 acquired customers if one customer equals one booking, but only completed bookings turn demand into income.

Improve Booking Volume

Measure the funnel from inquiry to booked to completed, and split it by date, ZIP code, and weather. If rain, travel gaps, setup delays, or weak off-season demand cut utilization, the owner’s take-home falls fast because the crew and gear sit idle while fixed costs keep running.

Protect weekend slots first, then fill weekday and shoulder-season dates with schools, camps, churches, and corporate groups. One clean rule: more completed bookings spread $1,975/month of fixed overhead across more revenue, which is what raises cash available for owner pay.

Equipment costs and maintenance

Equipment Wear and Reserve

Equipment maintenance and consumables take a direct bite out of owner pay. At 8% of Year 1 revenue, then 6% by Year 5, every $10,000 in sales leaves $9,200 then $9,400 before fixed costs and profit draw. That means clean gear, working batteries, and fast resets are not just ops issues; they are cash issues.

The setup includes blasters, sensors, batteries, chargers, bunkers, bins, and cleaning. The $83,000 startup kit only supports income if bookings are high enough to spread wear across more events. More events can raise revenue, but they also push up repair and replacement spend, so the owner needs a reserve tied to usage.

Hold Back a Repair Reserve

Estimate wear from bookings, event length, player count, and hours used, then compare that to repairs, batteries, and cleaning spend. Track maintenance cost as % of revenue, damaged unit count, battery swaps, cleaning supply use, and downtime after each event. If one event type breaks gear faster, price it higher or cap it.

Reserve 8% of Year 1 sales.

Drop to 6% only with proof.

Log repairs after every event.

Replace weak batteries fast.

Retire damaged gear before failures.

Use that reserve to protect cash flow, since owner income is what’s left after repairs and consumables. If gear sits in the shop, you lose booking capacity too, so the hit is bigger than the repair bill alone.

Event capacity

Event capacity

Event capacity is how many paid events and billable hours the business can fit into a weekend after travel, setup, teardown, charging, and reset. It drives income because every filled slot turns demand into revenue, but a weak route can block a better booking. In Year 1, the mix shows 175 hours from birthday parties, 25 hours from corporate events, and 3 hours from community events.

Here’s the quick math: more usable hours raise revenue without adding much fixed cost, so capacity use affects gross margin and owner pay fast. The real risk is not just demand, it’s bad slot fit. An inquiry is worth less if it adds too much drive time or breaks a high-value weekend pattern.

Track slot fit, not just leads

Measure events per weekend, hours sold, travel radius, and total time lost to setup, teardown, charging, and reset. Also track which event types fill prime weekend slots versus slow gaps. If a lower-price booking blocks a better one, it cuts take-home income even when it looks busy.

Score each inquiry by route fit.

Protect prime Saturday slots.

Decline long-drive low-value jobs.

Tight routing improves utilization, which means more paid hours from the same crew and equipment. The owner should price and schedule around the most valuable time blocks first, then fill leftover space with smaller events only when they do not crowd out stronger bookings.

Seasonal demand

Seasonal channel mix

Seasonal demand is mostly a mix problem: birthday parties drive Year 1 volume, but weekday channels keep cash flow steadier. The base mix assumes 70% birthday parties, 10% corporate events, and 5% community events, while add-on sales show up on 30% of bookings. That mix matters because it changes how often the owner can fill slow dates and keep pay from swinging with weekends.

By Year 5, the plan shifts to 50% birthday parties, 30% corporate events, 25% community events, and 50% add-on incidence. One clean read: more school, camp, church, fundraiser, and corporate work should smooth bookings, lift weekday utilization, and lower the marketing cost per booking.

Track weekday fill and add-on rate

Measure bookings by source, day of week, and event type, then compare that to add-on sales on each job. The key inputs are birthday, corporate, and community booking counts, plus the share of bookings that buy extras. If weekday channels rise and add-on incidence moves from 30% toward 50%, revenue gets less seasonal and gross profit becomes easier to forecast.

Track weekday bookings by channel

Measure add-on sales per event

Compare CAC by booking source

Prioritize schools and corporate groups

Watch slow months and empty dates

If schools, camps, churches, and fundraisers fill open weekdays, the owner can spread fixed labor and travel over more paid events. What this hides: weak routing or slow setup can still waste the extra demand, so the schedule has to be tight for the pay to improve.

Staffing model

Staffing mix and owner pay

Owner-led events keep more cash per booking, but labor still hits profit. The model includes a $60,000 owner/operator salary, a $35,000 lead coordinator at 0.5 FTE in Year 1, and a $20,000 part-time coordinator at 0.25 FTE. Coordinator variable pay is also 12% of Year 1 revenue, so take-home income only improves when booked events cover payroll, travel, and setup time.

The key question is capacity, not headcount. If hiring lets the business run more simultaneous events, profit rises only when added bookings beat the extra labor cost and drive time. One weak route, one long reset, or one low-margin booking can wipe out the gain. Owner pay depends on how tightly staffing matches booked hours, weekend slots, and actual event volume.

Keep payroll tied to booked hours

Track events per staff hour, labor cost per booking, and travel minutes per event. Here’s the quick math: fixed pay plus 12% variable pay must be covered before the owner draws extra cash. If a hire does not create enough added bookings in the same weekend window, the business just adds overhead.

Measure pay per completed event.

Test route density by zip code.

Limit long drives for small jobs.

Use part-time help for peak slots.

What this hides: labor only works when scheduling stays tight. If setup, teardown, or travel pushes one event into the next slot, you lose capacity and owner income falls fast. The clean win is simple: add staff only when booked demand is already there.

Average event price

Average Event Price

Average event price is the mix of hourly rate and add-ons you charge per booking. In Year 1, birthday parties can price at $180/hour, corporate events at $250/hour, community events at $150/hour, and extended time at $100/hour. A 2-hour birthday party = $360 before add-ons, while higher-rate corporate jobs lift revenue per slot and help cover fixed costs.

This driver changes owner pay fast because one underpriced trip can wipe out the margin from a full event. Use duration, player count, travel distance, night games, and add-ons to set price. The revenue examples of $315, $625, $450, and $50 show how upsells matter, but travel priced too low can erase profit.

Price by event, not just by hour

Track average price by job type, then compare it to drive time and setup time. If the booking looks good on paper but the travel is long, the hourly rate can fall below your target. One clean rule: raise price when the route gets longer or the event runs after dark.

Separate birthday, corporate, and community rates.

Quote travel before you confirm.

Add fees for night games.

Charge more for larger player counts.

Price add-ons before the event starts.

Test which package mix lifts revenue per completed booking. Corporate events at $250/hour should carry more margin than community events at $150/hour, so don’t fill prime slots with low-priced jobs unless routing is tight.