How Much Business Scaling Consulting Owners Make At $987k Revenue

In this model, the owner earns a planned $185,000 salary, but true business scaling consulting owner income depends on whether the firm can also distribute profit Year 1 shows $987,000 of revenue, an 82% delivery gross margin, and -$334,000 EBITDA, so there is no clean profit distribution By Year 3, revenue reaches $3434 million and EBITDA reaches $1023 million, creating potential pre-tax owner economics of salary plus distributable cash if reserves allow By Year 5, revenue reaches $7803 million and EBITDA reaches $3876 million, but taxes, reserves, debt service, and reinvestment still come first

Owner income$185k baseNet margin-34% to 50%Revenue for target pay$1.1MBusiness difficultyHard

Want the six main owner income drivers?

1

Qualified Pipeline

$3.5K-$4.5K CAC

Lower CAC and a bigger marketing budget improve pipeline quality, so more sales spend turns into booked work.

2

Pricing Power

$200-$375/hr

Higher hourly rates raise revenue per engagement without adding the same amount of delivery time.

3

Retainer Growth

20%-60%

Shifting more work to retainers steadies cash and increases lifetime value per client.

4

Delivery Capacity

42-52h

More billable hours per active customer let each account produce more revenue before you hire again.

5

Gross Margin

82%-87%

A higher gross margin keeps more of each dollar after SaaS, contractor, and travel costs.

6

Cash Buffer

$474K

Holding a $474K cash floor protects owner pay when growth spending rises and the Month 14 dip hits.

Want to test your own consulting owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, reserves, and distributions. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Business Scaling Consulting Service model?

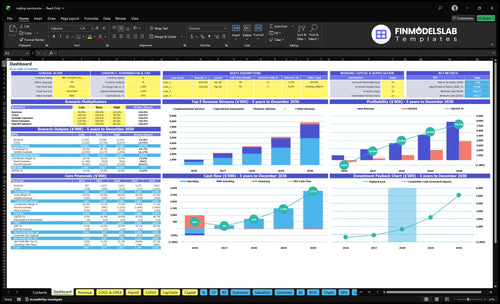

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions. Open the Business Scaling Consulting Service Financial Model Template to review the dashboard, revenue model, service mix, staffing, expenses, capex, cash flow, scenarios, and owner income outputs.

Owner-income model highlights

Owner pay and take-home

Revenue to $7.803M

82% to 87% margin

Month 10 breakeven

Month 30 payback

$474k cash need

Do retainers or project fees make more money for scaling consultants?

Project fees usually make more money near term for a Business Scaling Consulting Service, while retainers make cash flow steadier. Here’s the quick math: a Year 1 implementation project is 80 hours at $200/hour, or $16,000 per assigned client, versus a Year 1 advisory retainer at 10 hours and $300/hour, or $3,000 per assigned client; by Year 5, the mix shifts to 100 implementation hours at $250 and 15 advisory hours at $375. The catch is simple: projects lift revenue, retainers smooth utilization, and scope creep can wipe out the pricing edge.

Projects pay faster

$16,000 per project in Year 1

80 hours at $200/hour

Higher near-term revenue

Best for implementation work

Retainers stay steadier

$3,000 per client in Year 1

10 hours at $300/hour

Smoother utilization

Feed diagnostics into pipeline

How do consultant costs affect scaling consulting owner income?

Consultant costs affect owner income in two layers: they first squeeze gross margin through delivery costs, then cut net profit through payroll. For What Is Your Business Idea Name For Core 5 KPI Metrics?, external SaaS integration fees run 8% to 6% and contractor project support runs 10% to 7%, so delivery gross margin lands near 82% to 87%. The heavier scale cost is payroll, rising from $690,000 in Year 1 to $1.505 million in Year 5, so hiring helps capacity but can still reduce owner take-home if pipeline lags.

Delivery margin math

8% to 6% SaaS integration fees

10% to 7% contractor support

82% to 87% delivery gross margin

Lower delivery cost lifts cash fast

Payroll is the real drag

$690,000 Year 1 payroll

$1.505 million Year 5 payroll

2 FTE to 6 FTE senior consultants

Low utilization hurts twice

Should a scaling consulting owner hire consultants or keep delivering client work?

Keep the founder on delivery early, because it protects quality and margin, but it also caps capacity. In the Business Scaling Consulting Service, the math supports hiring only when the qualified pipeline, close rate, and billable backlog can carry the salary load. A model that starts with a $185,000 Managing Principal, adds 2 senior consultants in Year 1, and reaches 6 by Year 5 can scale revenue from $987,000 to $7.803 million, but payroll risk shows up before utilization does. If you can’t fund the $474,000 cash need by Month 14, don’t hire yet.

Keep delivery tight

Founder keeps client quality high

Early margin stays stronger

Capacity stays limited, though

Burnout risk rises fast

Hire with proof

Hire when backlog can pay salary

Watch close rate and pipeline

Onboarding drag can hurt delivery

Small firms can still win

Key Takeaways

Qualified leads and close rate drive first-year revenue.

Better packaging raises fees without equal workload.

Retainers smooth cash and lift lifetime value.

Utilization, margin, and cash reserves protect scale.

Compare lean, base, and high owner income scenarios

Owner income scenarios

Owner income changes fast as this consulting firm adds billable hours, raises rates, and shifts from project work to retainer work. The low case stays salary-only, while the base and high cases show where pre-tax owner economics can scale.

Low, base, and high owner-income cases for a scaling consultancy.

Scenario

Low CaseLean ramp

Base CaseScalable base

High CaseHigh-retainer upside

Launch model

Revenue stays in Year 1 territory, so EBITDA is still negative and owner income is limited to salary.

The Year 3 model reaches scale, with stronger margin and enough EBITDA to support pre-tax owner economics.

The Year 5 model pushes into mature, retainer-heavy scale, with the highest pre-tax owner economics.

Typical setup

Year 1 uses $987,000 revenue, 82% gross margin, $690,000 payroll, $45,000 marketing, $192,600 fixed overhead, and a $334,000 EBITDA loss.

Year 3 uses $3,434,000 revenue, 85% gross margin, 75.5% contribution, $1,055,000 payroll, $85,000 marketing, and $1,023,000 EBITDA.

Year 5 uses $7,803,000 revenue, 87% gross margin, 79% contribution, $1,505,000 payroll, $140,000 marketing, and $3,876,000 EBITDA.

Cost drivers

Price per hour

billable hours

payroll load

fixed overhead

marketing spend

More billable hours

better pricing

richer retainer mix

payroll growth

margin expansion

Retainer mix

higher hourly rates

more billable hours

scale efficiency

lower support costs

Owner income rangeBefore owner reserves

$185,000 salary onlySalary only

Up to $1,208,000Modeled upside

Up to $4,061,000Top-end upside

Best fit

Use this to stress-test a slow ramp, heavier staffing, and no supported distribution.

Use this as the main planning case for a growing firm with steady project flow and rising advisory revenue.

Use this to test upside if the firm keeps adding retainers, holds pricing, and uses staff well.

!

Planning note: Scenario figures are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or distributions.

Business Scaling Consulting Service Core Six Income Drivers

Qualified pipeline and close rate

Qualified Pipeline and Close Rate

If the pipeline is thin, revenue stalls before margin work even starts. With annual marketing at $45,000 and $4,500 CAC, the math points to about 10 acquired customers in Year 1 if that CAC holds.

That matters because poor-fit clients soak up senior time, drag out the sales cycle, and delay higher-margin retainers. Better lead quality lifts revenue without forcing discounting or over-hiring, so owner pay has a cleaner path up.

Track Lead Quality, Not Just Lead Count

Measure marketing budget, qualified leads, close rate, CAC, sales cycle, and win quality by source. The source values matter: marketing rises from $45,000 to $140,000, and CAC falls from $4,500 to $3,500.

Budget by source

Lead-to-close rate

Sales cycle days

Customer fit score

Here’s the quick math: $140,000 ÷ $3,500 = 40 customers if the assumption holds. Use that only if those leads still match the right project size and can convert without extra handholding.

Retainer retention and expansion

Retainer retention

Retainers turn lumpy project revenue into a steadier cash base. In this model, advisory retainers grow from 20% of the mix in Year 1 to 60% in Year 5, so the owner can plan staffing and pay with less guesswork. Here’s the quick math: 10 hours × $300 = $3,000, then 15 hours × $375 = $5,625 per advisory engagement.

The risk is churn. If a retainer ends, the firm has to replace revenue before it can grow it, and that burns senior sales time. Strong retention raises lifetime value and smooths consultant utilization, which helps protect gross profit and the owner’s draw.

Track renewals and upsells

Watch retainer revenue share, renewal rate, and the path from assessment to implementation to advisory to follow-on support. When a client moves up that ladder, revenue improves without a full new sale, and the owner gets more income from each account. The more the mix shifts to advisory, the more predictable the month becomes.

Price the next step before the current one ends, and tie it to the higher $375 advisory rate instead of the lower diagnostic work. Also track hours used versus hours sold. That shows whether the retainer is expanding cleanly or leaking margin through extra work that never gets billed.

Delivery capacity and utilization

Delivery Capacity and Utilization

When average billable hours per active customer rise from 42 to 52 per month, the same team can support more revenue without a matching jump in overhead. That is a 24% gain in billable output per customer, so utilization decides whether payroll creates profit or drag.

This matters because staffing grows from 2 to 6 senior consultants, 1 to 3 project managers, and 1 to 2 business development managers, while the Managing Principal stays at 1 FTE and $185,000. Overbooking hurts quality; underbooking crushes margins.

Track Billable Load, Not Headcount

Measure utilization by role each month: billable hours, active customers, and non-billable rework. If senior consultants are full but project managers are not, delivery slows and owner pay gets squeezed. The quick check is simple: more staffed hours should show up as more billable hours, not just more payroll.

Track billable hours per active customer.

Set a quality guardrail for overload.

Watch unbilled time by role.

Forecast payroll against booked work.

Use those numbers to staff before burnout starts. If utilization stays balanced, revenue capacity rises and the owner keeps more of each dollar after payroll, instead of funding idle time.

Delivery gross margin

Delivery Gross Margin

Delivery gross margin is the share left after direct delivery costs, or cost of goods sold (COGS). Here that means contractor project support, implementation partners, delivery tools, and non-billable rework. In this model, COGS improves from 18% of revenue in Year 1 to 13% in Year 5, so gross margin rises from 82% to 87%.

That is profit before overhead, owner salary, taxes, and distributions. Here’s the quick math: every 1 margin point equals 1% of delivery revenue kept by the business. So when revenue scales, even small cost leaks matter more and directly reduce the cash left for payroll, reserves, and owner pay.

Hold Delivery Costs Tight

Track gross margin by project, not just in total. Compare billable hours to contractor hours, partner fees, and rework hours each month. If delivery work needs more hand-holding than planned, the margin should show it fast. The goal is to keep delivery COGS inside the built-in 13%–18% band.

Protect margin by tightening scope, pricing extra changes, and moving repeat tasks into standard steps. If delivery stays custom-heavy, the owner feels it first in slower cash buildup and weaker draw capacity. Better control of support labor and rework usually matters more than chasing a slightly higher top-line rate.

Overhead, reserves, and reinvestment

Overhead, reserves, and reinvestment

Even with positive EBITDA (earnings before interest, taxes, depreciation, and amortization), owner pay can stay thin because $16,050 per month of fixed overhead comes out first. That bucket includes office lease, insurance, tech subscriptions, accounting and legal, utilities, and content production. Add payroll from $690,000 in Year 1 to $1.505 million in Year 5, and cash can tighten fast.

The business also plans $132,500 of capex and a $474,000 minimum cash need in Month 14. So even when the income statement looks fine, reinvestment and reserves are not distributable cash. If billings slip or hiring runs ahead of revenue, owner draws should slow before cash does.

Track cash before taking profit

Measure monthly overhead run rate, payroll load, capex timing, and reserve coverage against the $474,000 Month 14 need. Keep a simple cash forecast that shows what is left after fixed costs, not just after EBITDA. That tells you when reinvestment is building capacity and when it is just reducing take-home income.

Use a rule for owner draws: only pay yourself from cash above the reserve floor. If you add staff, systems, or content work, tie each dollar to either more billable capacity or better retention. Otherwise, reinvestment becomes a drag on income instead of a growth engine.

Average engagement value and pricing model

Average engagement value and pricing model

Average engagement value is the revenue you earn per project, and it moves owner income fast because this firm sells senior time. At 25 hours for assessments at $250-$310 per hour, revenue is about $6,250-$7,750 per engagement before costs.

Implementation is bigger: 80-100 hours at $200-$250 per hour means roughly $16,000-$25,000. Advisory is the highest rate, at $300-$375 per hour, but only 10-15 hours, or about $3,000-$5,625. The trap is simple: premium pricing only holds when scope is tight and outcomes are clear.

Price by outcome, not by hope

Track hours sold, hours billed, and change orders by engagement type. Those three inputs tell you whether pricing is lifting profit or just hiding extra labor. One clean line: if scope creep rises, take-home pay drops even when revenue looks strong.

Set a fixed outcome for each scope.

Separate assessment, implementation, advisory.

Bill senior work at the top rate.

Cap revision rounds in writing.

Watch revenue per delivered hour.

Use the model to forecast cash and margin. A $6,250 assessment and a $25,000 implementation do not create the same owner pay, especially if the larger job needs more rework or senior review. What this estimate hides: vague scope can erase the benefit of higher prices fast.