How Much a STEM Summer Camp Owner Can Make: $25M Year 1 EBITDA

You’re testing whether a STEM summer camp can pay the owner after tuition, staffing, facility costs, materials, marketing, and reserves This five-year planning view uses researched assumptions, including $3736M Year 1 revenue, $2501M Year 1 EBITDA, and 65% Year 1 occupancy It is not tax advice, a guaranteed salary, or a market-specific quote

Owner income$2.5M to $30.5MNet margin67% to 84%Revenue for target pay$3.7MBusiness difficultyMedium

Want to test your STEM camp owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income will vary with enrollment, staffing, taxes, reserves, and cash needs, and this is not salary, tax, or owner distribution advice.

Want to see what moves STEM camp owner income?

1

Paid Enrollment

65%-92%

Moving occupancy from 65% to 92% is the biggest swing in revenue, because every filled seat spreads the same camp cost base.

2

Tuition Price

$1.4K-$1.8K

Monthly tuition at $1,400 to $1,800 per cohort lifts revenue fast, as long as discounts stay tight.

3

Schedule Capacity

22 days

With 22 billable days a month, more camp weeks and fuller cohorts turn fixed staff time into more billable seats.

4

Staff Ratio

$438K

Instructor FTE rises fast, so every extra child per supervisor can protect margin when payroll and fixed costs already total about $438K in Year 1.

5

Facility Load

$9.5K/mo

Facility rent, utilities, equipment, insurance, and permits set the monthly cost floor, so unused space hits take-home hard.

6

Add-On Mix

$2.5K-$8K

Extended care fees rising from $2,500 to $8,000 add high-margin income without adding a full new camp track.

Want a cleaner STEM Summer Camp Program financial model?

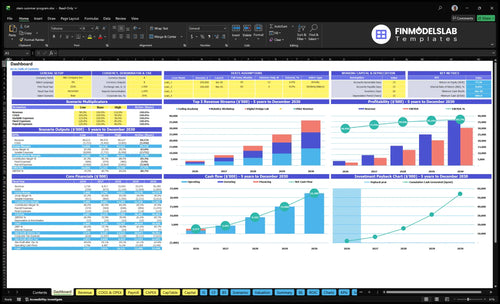

This dashboard in the STEM Summer Camp Program Financial Model Template ties enrollment, tuition, staffing, facility costs, materials, marketing, reserves, and owner income together. It also shows $3.736M Year 1 revenue vs $36.399M Year 5 and $2.501M EBITDA vs $30.483M; open the model.

Owner-income model highlights

Owner take-home output

COGS, payroll, fixed costs

Capex, cash flow, scenarios

How many campers does a STEM summer camp need to be profitable?

The STEM Summer Camp Program needs about 31 active paid camper-months to cover costs in the Year 1 model, but there’s no universal camper count because tuition, occupancy, staffing, and overhead set breakeven; see What Are The 5 KPIs For STEM Summer Camp Program Business? for the operating metrics to track.

Breakeven math

Use $1,492 weighted monthly tuition

Include $438k annual payroll

Add 20% direct and variable costs

Model reaches breakeven in Month 1

Count only paid campers

Exclude inquiries from enrollment count

Exclude waitlist names

Adjust for refunds and credits

Recheck if occupancy drops below 65%

What STEM summer camp profit margin should owners plan for?

Owners should plan for a very high margin profile in the STEM Summer Camp Program, but the real story is sensitivity: the model implies an 66.9% EBITDA margin in Year 1 and 83.7% in Year 5, so track the five core measures in What Are The 5 KPIs For STEM Summer Camp Program Business? and watch costs closely. Here’s the quick math: direct camp costs fall from 9% of revenue to 5%, and variable marketing plus processing drops from 11% to 8%.

Margin drivers

Year 1 EBITDA: 66.9%

Year 5 EBITDA: 83.7%

Direct costs: 9% to 5%

Marketing plus processing: 11% to 8%

Watch this

Staffing: $324k to $823k

Safety stays funded: don't trim it

Supervision stays funded: don't trim it

Quality stays funded: don't trim it

How much revenue does a STEM summer camp need to pay the owner?

The STEM Summer Camp Program has to cover $438k first in Year 1: $324k of payroll plus $114k of fixed overhead. After that, owner pay is a planning output, not the starting point; with a 20% direct and variable load, each $1 of owner pay needs about $1.25 of extra revenue before reserves and taxes.

Year 1 floor

$324k payroll

$114k fixed overhead

$438k before owner pay

20% direct and variable load

Owner pay test

$1 owner pay needs $1.25 revenue

Check reserve policy first

Check cash timing next

Model shows $3.736M revenue

That same model shows $2.501M EBITDA in Year 1, so the camp can support owner pay only after core costs, fees, and reserves are covered. The real question is not “Can the owner be paid?” but “How much revenue is left after the camp protects cash?”

Key Takeaways

Filled paid seats drive the biggest income lift.

Tuition cuts revenue fast, but costs stay fixed.

More cohorts help only when staffing keeps up.

Add-ons boost margin best after cohorts are full.

Compare low, base, and high STEM camp owner-income scenarios

Owner income view

Owner income rises with occupancy, pricing, and campus fill. Higher enrollment lifts EBITDA (earnings before interest, taxes, depreciation, and amortization), but payroll and fixed site costs still set the floor.

Low, base, and high cases show how enrollment and cost load change owner take-home potential.

Scenario

Low CaseDownside case

Base CasePlanning case

High CaseUpside case

Launch model

This is the lower-earnings path built from Year 1 at 65% occupancy.

This is the modeled middle path built from Year 3 at 85% occupancy.

This is the stronger-earnings path built from Year 5 at 92% occupancy.

Typical setup

Revenue is $3.736M, EBITDA is $2.501M, payroll is $324k, fixed costs are $114k, and direct and variable load is 20%.

Revenue is $15.943M, EBITDA is $12.582M, payroll is $568k, and direct and variable load is 16%.

Revenue is $36.399M, EBITDA is $30.483M, payroll is $823k, and direct and variable load is 13%.

Cost drivers

65% occupancy

$3.736M revenue

$2.501M EBITDA

$324k payroll

20% direct and variable load

85% occupancy

$15.943M revenue

$12.582M EBITDA

$568k payroll

16% direct and variable load

92% occupancy

$36.399M revenue

$30.483M EBITDA

$823k payroll

13% direct and variable load

Owner income rangeBefore owner reserves

About $2.5M EBITDALow case

About $12.6M EBITDABase case

About $30.5M EBITDAHigh case

Best fit

Use this to stress-test the first operating year and early fill risk.

Use this as the planning case for steady enrollment and normal staffing growth.

Use this to test what high fill and scale can do for owner income.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Reserves are not provided and should be modeled separately.

STEM Summer Camp Program Core Six Income Drivers

Paid Enrollment And Capacity Utilization

Paid Enrollment and Capacity

This driver is the share of seats that are sold, paid for, and actually attended. In Year 1, occupancy is 65%; by Year 5 it rises to 92%. That matters because filled paid seats spread payroll, rent, insurance, software, and admin across more tuition revenue, so owner profit usually moves up faster than headcount. A filled coding cohort is worth more than a long inquiry list.

The key inputs are paid campers per cohort, refunds, scholarship seats, and waitlist conversion. Counting unpaid registrations as revenue overstates profit and can leave the owner short on cash. One line matters most: if a seat is not paid, it does not help pay staff.

Fill Paid Seats First

Track occupancy by cohort, not just total inquiries. Compare booked seats, paid seats, and attended seats each week, then close unpaid holds fast. Here’s the quick math: each extra paid camper lifts tuition revenue while fixed costs stay mostly flat, so gross margin improves and more cash can flow to owner pay.

Watch refund and scholarship rates.

Measure waitlist-to-paid conversion.

Match staffing to paid seats.

Do not count unpaid registrations.

Add-On Revenue And Program Mix

Add-On Revenue

Add-ons raise revenue per camper when the base cohort is already full. If extended care fees move from $2,500 in Year 1 to $8,000 in Year 5, that can lift cash and margin fast, but only if demand is there. The key question is attach rate, or how many enrolled campers buy the extra service. One full cohort can support a lot more owner income than a big waitlist.

This income driver includes before-care, after-care, premium robotics, advanced coding, specialty workshops, supply fees, and school partnerships. Here’s the quick math: add-on revenue = campers × attach rate × add-on price. What this estimate hides is the cost side. Extra staff, supervision, insurance review, and parent communication can absorb part of the gain, so add-ons are upside, not pure profit.

Track Attach Rate, Not Just Sales

Measure add-ons by cohort, not by total season sales. Track how many families buy each item, the price collected, and the extra labor hours needed. If premium options sell well but require more supervision, the owner may see higher revenue and only a modest profit lift. A 10% to 20% attach rate on a full camp is often more useful than a long list of optional products nobody buys.

Track add-on attach rate weekly.

Price each add-on separately.

Test demand before staffing up.

Budget for extra supervision time.

Confirm insurance coverage before launch.

Send parent emails before billing.

Use add-ons to protect take-home pay when core seats are already sold. If a cohort is full, add-ons can improve gross margin without adding another full session, but only when the extra cost stays below the fee collected. The right test is simple: incremental revenue minus incremental labor and support cost. If that spread is thin, keep the offer small.

Instructor Staffing And Supervision Ratio

Instructor Staffing And Supervision Ratio

In this model, staffing is the guardrail on safety, quality, and margin. Year 1 payroll is $324k, with one $85k program director, two $55k lead instructors, three $35k assistant instructors, and 5 marketing and admissions FTE. By Year 5, payroll reaches $823k. If paid seats do not rise with staffing, tuition dollars get eaten by labor and the owner’s draw shrinks.

Here’s the quick math: adding one lead instructor costs $55k a year before taxes and benefits. That only works when the added cohort or supervision load lifts revenue enough to cover it. Understaffing is risky too; it can hurt parent trust, retention, and compliance, which can hit cash flow faster than the wage savings help.

Staff to paid campers, not inquiries

Measure paid campers per instructor, assistant coverage by cohort, overtime, substitute use, refund rate, and any safety or complaint events. Tie each cohort to a staffing plan before you open seats. A filled seat supports payroll; an empty inquiry does not.

Track payroll as tuition share.

Watch attendance by cohort.

Log incidents and parent complaints.

Keep backup coverage ready.

If attendance drops or a cohort runs below plan, delay the next hire or split the schedule before cutting supervision. The goal is not the lowest wage bill; it is the best profit per safe, well-run seat.

Camp Weeks, Cohorts, And Schedule Capacity

Camp Weeks And Cohort Count

More camp weeks or cohorts only raise income when paid seats and staff keep pace. The model uses 22 billable days per month, so adding schedule blocks without filling them can lift payroll, supervision, and facility costs faster than tuition. Capacity also rises by track: Robotics Workshop from 40 to 120, Coding Academy from 50 to 130, and Digital Design Lab from 30 to 90.

Here’s the quick math: more sessions increase revenue only if occupancy stays strong. Empty added cohorts still use staff time, rooms, materials, and admin support, so owner take-home can drop even while the schedule looks bigger. The key inputs are paid enrollment per cohort, staffing per session, and billable-day utilization; unpaid registrations do not pay rent.

Track Seats Before You Add Weeks

Start with the fill rate on each track, not the wish list. Measure paid campers, waitlist-to-paid conversion, cancellations, and the cost of opening one more cohort. If a new week cannot be sold before staffing is locked, it usually weakens margin instead of helping it.

Track paid seats by week.

Test demand before adding cohorts.

Match staff to paid enrollment.

Watch empty-session cost drag.

Use the schedule as a cash flow tool. When added weeks push revenue, they spread fixed costs over more tuition; when they do not, they dilute marketing focus and add overhead. The clean control is simple: open only the cohorts you can fill, then scale the tracks with proven demand.

Tuition Pricing And Discounts

Tuition Pricing

Tuition sets revenue per camper before cost control matters. Year 1 monthly tuition is assumed at $1,600 for robotics, $1,400 for coding, and $1,500 for digital design; by Year 5, that rises to $1,800, $1,600, and $1,700. If parents accept the higher rate, owner income rises without adding more seats.

Discounts cut revenue right away. An early-bird, sibling, or scholarship discount lowers net tuition per camper, but instructor and facility costs may stay flat, so margins can shrink fast. Pricing has to match local market, parent willingness to pay, and program quality, or the camp may fill seats but still miss profit targets.

Protect Net Tuition

Track gross tuition, discount rate, and net tuition per enrolled camper by track. Use these inputs in every forecast: seats sold, full price, discount mix, and scholarship seats. That tells you whether higher pricing is lifting take-home income or just masking weak demand.

Measure full-pay vs discounted seats.

Cap scholarships by cohort.

Test pricing by program track.

Watch margin after fixed staff.

Here’s the quick math: if coding tuition is $1,400 and a discount cuts it by 10%, revenue drops to $1,260 before any cost falls. If enrollment does not rise enough to offset that drop, owner pay falls too. Keep discounts tied to a clear fill-rate goal, not habit.

Facility, Equipment, And Program Materials

Facility and Equipment Burn

STEM camps need classrooms, lab setup, tech, consumables, software, insurance, and compliance. In this model, facility rent and utilities are $6,500/month, insurance is $800, and compliance checks are $250, so recurring overhead starts at $7,550/month before kits and software. That cost stays even when seats are empty, so low enrollment cuts owner pay fast.

Year 1 also carries 6% project consumables and kits plus 3% curriculum licensing and software. The launch equipment pack totals $152,000 across robotics kits, laptop stations, 3D printers, smart boards, curriculum development, and lab setup. Here’s the quick math: if tuition cash comes in slowly, this equipment-heavy setup can squeeze operating cash before the owner can draw profit.

Track Cash per Cohort

Build the model around paid campers, session count, and kit use per cohort. Measure each class against $7,550/month of fixed facility overhead, then add the 6% consumables load and 3% software/licensing cost. A filled cohort spreads those costs better; a half-full one leaves the lab expensive and underused.

Track paid seats, not registrations.

Log consumables per camper.

Schedule software renewals.

Stagger kit replacement buys.

Protect cash by tying purchases to enrollment, not hope. If robotics kits, laptops, and printers arrive before tuition is collected, owner income gets delayed even when demand looks strong. One clean rule helps: buy only what the next cohort needs, then review whether each program still covers its share of fixed costs.