This page covers insurance fraud investigation launch costs for the startup period, first month, and first operating year The researched planning assumptions include $28,800 in monthly fixed overhead, $180,000 in Year 1 marketing, and separate buckets for CAPEX, pre-opening costs, and working capital These figures are planning assumptions, not vendor quotes, revenue promises, or legal advice

Calculate Fuding Needs

Startup cost summary

Shows the main launch assets and the non-CAPEX cash buffer needed before breakeven for an insurance fraud investigation service.

Highlighted CAPEX$525,000Base planning example

Excluded cash needs$744,000Outside CAPEX total

Funding need$1,269,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

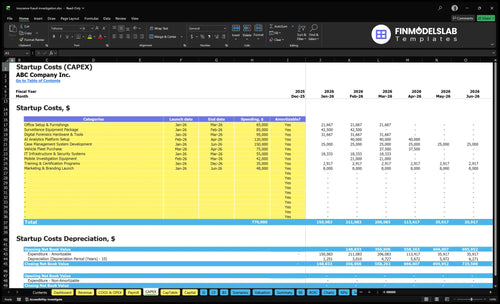

CAPEX Calculator

Case Management System Development

$150,000

Case tracking, documentation, and workflow build

Yes

AI Analytics Platform Setup

$120,000

Analytics setup for fraud detection and review

Yes

Digital Forensics Hardware & Tools

$95,000

Evidence capture and forensic analysis tools

Yes

Surveillance Equipment Package

$85,000

Field surveillance kit and monitoring gear

Yes

Vehicle Fleet Purchase

$75,000

Investigator transport for site work and stakeouts

Yes

Opening Cash Buffer

$744,000

Cash needed to bridge the month 20 trough before breakeven

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for an insurance fraud investigation firm, including field gear, vehicles, office fit-out, and evidence-security setup.

!

Scope note This calculator covers capitalized startup assets only. It excludes working capital, payroll runway, deposits, debt service, inventory runway, insurance premiums, database subscriptions, and ongoing operating expenses.

Startup costs swing a lot here because licensing, evidence security, vehicles, and staffing change fast with case volume. Lean, base, and full setups match very different carrier loads.

Lean, base, and full launch cost bands for an insurance fraud investigation firm.

Scenario

Lean LaunchLow burn

Base LaunchBalanced build

Full LaunchScale ready

Launch model

Run a lean, mostly remote model with one lead investigator, limited office space, and only the vehicles needed for licensed field work.

Use a carrier-ready small firm built around the model's $28.8k monthly fixed overhead, plus $15k marketing, $3.2k liability insurance, and $4.5k IT security.

Build a multi-investigator platform with secure office controls, more vehicles, deeper equipment, and larger working capital.

Typical setup

Use home-office or low-rent space, tighter evidence controls, and fewer vehicles if licensing and carrier onboarding permit.

Set up a small office with core case systems, standard field coverage, and enough security for carrier audits.

Set up a secured office, more field investigators, broader equipment, and larger working capital for parallel cases.

Cost drivers

Office setup

evidence security

core software

limited vehicles

licensing checks

Fixed overhead

marketing

liability insurance

IT security

core staff

Multi-investigator payroll

vehicles

advanced tools

secure office controls

working capital

Planning rangeCAPEX only

Low six figuresLean budget

Mid six figuresCore budget

Seven-figure buildScale budget

Best fit

Best for founders testing one-state demand, keeping headcount tight, and serving carriers that accept lighter field coverage.

Best for a small firm serving repeat carrier clients that need field work, digital forensics, and documented claims support.

Best for operators with signed carrier demand, multiple investigators, and the cash to fund equipment, vehicles, and compliance-heavy growth.

!

Planning note: These bands are researched planning assumptions from the model, not vendor quotes or guaranteed prices.

What hidden costs come with starting an insurance fraud investigation business?

The biggest hidden cost in an Insurance Fraud Investigation Service is working capital, not equipment, because carrier payment cycles can lag while you still pay for checks, contracts, NDAs, security reviews, and report systems. If you’re mapping the plan, see How Do I Write An Insurance Fraud Investigation Service Business Plan? for the full setup. In Year 1, budget $4,500/month for IT and security, $2,800/month for legal and compliance, $1,200/month for office supplies and communications, plus 12% of revenue for travel and client support.

Cash timing costs

Working capital covers late carrier payments.

Background checks and legal contracts start early.

Nondisclosure agreements and compliance files add cash needs.

Travel reserves cover mileage, parking, and tolls.

Year 1 overhead load

Technology and data licensing run 85% of revenue.

IT and security cost $4,500/month.

Legal and compliance cost $2,800/month.

Office and communications cost $1,200/month.

How much money do you need to start an insurance fraud investigation service?

An Insurance Fraud Investigation Service should fund the full launch, not just equipment: the known Year 1 baseline is $83,800 per month before data analyst costs, variable costs, equipment financing, taxes, debt service, and owner distributions; see How Increase Profits For Insurance Fraud Investigation Service? for the profit side. Here’s the quick math: $28,800 fixed overhead + $15,000 marketing + $40,000 payroll from $480,000 annual salaries.

How should founders build a funding plan for an insurance fraud investigation startup?

Founders should fund the Insurance Fraud Investigation Service by tying cash to billable hours, case volume, utilization, and payment timing before they hire more investigators. Here’s the quick math: one Field Investigation case at 285 hours × $125 is $35,625, Surveillance and Monitoring is $51,750, Digital Forensics and Data Analysis is $34,225, and a Retainer Agreement is $91,800. With $300 billion in annual U.S. fraud losses, the plan should also carry the listed 270% Year 1 direct cost load and 40% variable sales, travel, and support costs before fixed payroll.

Fund the work first

Match cash to 30-60 day terms.

Protect runway for one billing cycle.

Hire after case volume is stable.

Track utilization before adding staff.

Year 1 pricing test

Test $35,625 field cases.

Test $51,750 surveillance cases.

Test $34,225 forensics cases.

Test $91,800 retainer deals.

Key Takeaways

Licensing and compliance have hefty recurring monthly costs.

Surveillance gear is a major upfront evidence expense.

Vehicles and travel need CAPEX plus monthly operating cash.

Software, insurance, and staffing drive startup working capital.

Insurance Fraud Investigation Service Core Five Startup Costs

Licensing, Registration, And Compliance Startup Expense

What it covers

Licensing and compliance setup usually starts with state private investigator licensing, agency registration, entity formation, background checks, and any surety bond a state requires. Add contracts, nondisclosure agreements, carrier onboarding files, and a clean compliance folder. Licensing rules vary by state, so treat this as planning guidance, not legal advice.

One-time setup

Use this bucket for filings and first-pass documents: entity formation, license applications, background checks, bond setup, and initial contract templates. The clean way to size it is by state count × filing steps × quoted fees. Keep it separate from monthly support so you can see launch cash needs clearly.

Count each licensed state

Price each required filing

Add first contract drafts

Recurring support

Plan monthly compliance support at $2,800 for legal and compliance fees, $800 for industry memberships, and $2,000 for training and professional development. That is $5,600 per month, or $67,200 per year. This is the cost of staying current on renewals, onboarding, and file upkeep.

Track renewals every month

Budget training before audits

Keep carrier files current

Keep it lean

Lower this cost by using one template set for contracts and NDAs, one compliance calendar for all renewals, and one document folder for licenses, bonds, and onboarding proof. The mistake to avoid is waiting for a carrier to ask for paperwork; rework gets expensive fast, and missed renewals can stop revenue.

Surveillance And Evidence Equipment Startup Expense

What it covers

This budget covers cameras, video recorders, lenses, tripods, lawful body-worn or vehicle-mounted accessories, time-stamping tools, backup devices, secure drives, and evidence storage. Treat it as documentation gear, not field flair: the point is admissible records, chain of custody, and insurer-ready reports. Year 1 mix includes 850% Field Investigation Services and 650% Surveillance and Monitoring, so this is core launch spend.

How to price it

Estimate it by investigator: units × vendor quote × months used. Split one-time gear from recurring storage and backup needs. The calculator should ask how many investigators need kits, how many backup devices are required, and how much secure storage each case uses. Without vendor quotes, avoid fixed prices.

Count one kit per investigator.

Separate gear from storage.

Use quotes, not guesses.

Keep it lean

Buy to the case mix, not to a shelf full of extras. Start with shared backups and reusable accessories, then add units as active investigators rise. The common mistake is paying for premium gear before volume proves the need. Standardize kits and match secure-drive capacity to retention rules.

Standardize one field kit.

Share backups across teams.

Scale storage with cases.

Compliance first

Use only lawful surveillance tools and keep date-stamped files, transfer logs, and storage access controls tight. That protects chain of custody and lowers the chance of challenged evidence. The equipment budget should sit beside training and file controls, because a cheap camera that weakens documentation costs more later.

Software, Databases, And Cybersecurity Startup Expense

Core Stack

The core stack covers case management, report writing, secure file sharing, encrypted email, cloud storage, background research databases, open-source intelligence tools, access controls, device management, and monitoring. Budget it as users × seats × months, plus storage and security add-ons. Keep recurring subscriptions out of capitalized spend unless a vendor contract is truly capitalized.

Run Rate

Plan for $4,500 per month in IT infrastructure and security. Here’s the quick math: monthly tools, device protection, and monitoring sit in operating spend, not one-time setup. For a lean launch, tie each subscription to a named role and a named device, then renew only what supports active cases and carrier reporting.

License Load

Technology and data licensing can get heavy fast: the model carries 85% of revenue in Year 1. That means license count, database depth, and search volume matter more than shiny bundles. What this estimate hides is overlap, so review every tool for duplicate data, unused seats, and monthly minimums before you sign.

Digital Work

Digital forensics and data analysis are material here: 350% Year 1 service allocation, 185 billable hours, and $18,500 per hour. That pushes software, databases, and cyber controls from support expense to core production cost. The budget should match evidence volume, retention needs, and secure access for every case.

Control Rules

Keep quality high by standardizing one case platform, one secure file path, and one device policy. Avoid paying for unused data feeds or open seats. If licenses and security start pushing past 85% of revenue, cut overlap before adding new tools. The main win is tight seat control and clean access rules.

Insurance, Bonding, And Staffing Readiness Startup Expense

Coverage Stack

Treat premiums and payroll readiness as working capital, not CAPEX. The model shows professional liability at $3,200 a month, or $38,400 for 12 months, before adding general liability, cyber liability, commercial auto, workers’ compensation, and any required surety bond.

Payroll Base

Known Year 1 payroll totals $480,000: $180,000 for the CEO and lead investigator, $95,000 each for two senior field investigators, and $110,000 for a digital forensics specialist. Do not include owner salary unless the founder funds it as working capital.

Hire Smart

Use quotes for limits, deductibles, recruiting, background checks, and training, then phase hires by case load. One clean rule: never cut compliance or pre-hire screening just to save cash. If onboarding slips, payroll starts before revenue, so keep a cash buffer ready.

Launch Reserve

Build a reserve for the first insurance bill and the first payroll cycle. Keep those dollars in operating cash, since they hit before collections. This model’s known payroll base is $480,000 a year, and professional liability alone is $3,200 a month.

Vehicles, Travel Readiness, And Field Mobility Startup Expense

Vehicle Setup

Treat vehicle purchase or lease, discreet upfit, and lawful dash accessories as CAPEX. Estimate it from vehicle count, quote per unit, and one-time install costs. Ask one key question first: do investigators use owned vehicles, reimbursed personal vehicles, or company vehicles?

Monthly Run Rate

Monthly mobility spend belongs in operating costs: commercial auto coverage, fuel, maintenance reserves, parking, tolls, and mileage reimbursement. The source model sets Travel and Client Support at 12% of Year 1 revenue, so size this from monthly revenue, field miles, and case volume. One line: miles drive cash burn.

Count vehicles by investigator type.

Track miles per case.

Set the reimbursement rate first.

Field Cost Split

The big risk is mixing fleet costs into overhead. Field Investigation Services carry 850% service allocation, so keep one-time vehicle upfit separate from recurring fuel, tolls, parking, and mileage in the model. If investigators use personal cars, the mileage policy becomes the control point. What this estimate hides: spread-out claims can lift travel cost fast.

Policy Check

Before launch, choose one vehicle policy and price it cleanly. Company cars push more cost into CAPEX and fixed monthly run rate; personal cars push more cost into reimbursed operating expense. Either way, tie the budget to investigator headcount, monthly miles, and whether the fleet needs discreet vehicles.