Microlending Startup Costs for a $15M First-Year Loan Pool

You’re not just paying to open a microlending business you’re funding loans, compliance, software, staff, and runway before collections catch up This researched first-year plan includes $15M in loans, $135M in funding sources, $425K in opening payroll, and $1176K in fixed overhead Lending capital is separate from physical CAPEX, so don’t treat the loan pool like office equipment

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates the capitalized startup assets needed to launch a microlending platform, not the lending pool or operating runway.

!

What this excludes This calculator covers CAPEX only. It excludes the lending pool, loan disbursement capital, payroll runway, marketing spend, monthly legal retainers, fixed overhead, debt service, deposits, inventory, and general working capital.

Calculate Fuding Needs

Startup cost summary

This table summarizes startup CAPEX and excluded launch cash needs for a microlending platform.

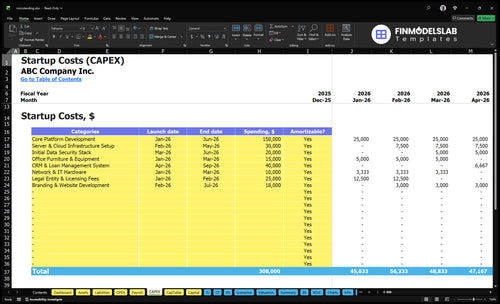

The Microlending Financial Model Template screenshot shows the CAPEX tab and startup costs by category, timing, amount, and depreciation or amortization. Review assumptions now.

Key screenshot highlights

CAPEX and startup costs

Monthly launch period

Year 1 to 5 model

Loans: $15M, then $50M

Payroll $425K; overhead $1.176M

Defaults 100%; acquisition 80%

$135M funding sources

Borrowing costs and runway

Compare 3 Startup Cost Scenarios

Scenario table

Smaller pilots stay close to the Year 1 $600K micro business loan line, while regional and full launches add more products, staff, and capital as loan volume and compliance needs rise.

Lean, Base, and Full microlending launch scenarios

Scenario

Lean Launchbest for pilot

Base Launchbest for regional proof

Full Launchbest for funded expansion

Launch model

Run one small-market test around the Year 1 $600K micro business loan line with a lean team and narrow product scope.

Launch five loan products in one region with the model's first-year plan and a larger funded book.

Scale across more geographies and build toward the Year 2 $5M and Year 3 $12M loan milestones.

Typical setup

Use light staffing, basic underwriting, and a simple tech stack.

Use the model's core team, regional compliance, and a wider lending pool.

Use a heavier risk, ops, and technology stack with broader lending coverage.

Cost drivers

Light staff

core platform build

basic compliance

small loan pool

Five loan products

payroll

regional licensing

compliance and security

funding sources

More geographies

stricter regulation

larger loan volume

extra underwriters

default reserves

Planning rangeCAPEX only

$600K - $1.5MPilot band

$15M - $135MRegional band

$12M - $50MScale band

Best fit

Best for founders testing demand before a full license and larger balance sheet.

Best for operators with capital and compliance support who want one regional proof point.

Best for funded teams that can handle slower approvals, higher oversight, and larger credit losses.

!

Planning note: These scenario ranges are researched planning assumptions from the model inputs and core metrics, not exact quotes, term sheets, or guaranteed funding offers.

How to fund a microlending business startup?

Fund Microlending with a Year 1 plan built around $15M in loan capital, $115K in other interest-earning assets, $425K in payroll, and $1.176M in fixed overhead, plus a default reserve and CAPEX. The clean funding stack is $500K angel funds, $400K development bank debt, $300K commercial bank LOC, $100K impact fund capital, and $50K crowdfunded debt. Here’s the quick math: model borrowing costs from 85% of development bank debt pricing to 150% for crowdfunded debt, then test defaults, loan growth, and monthly runway before raising.

Year 1 funding uses

$15M loan capital

$115K interest-earning assets

$425K payroll

$1.176M fixed overhead

Funding sources and checks

$500K angel investor funds

$400K development bank debt

$300K commercial bank LOC

Defaults, growth, and runway tests

What licenses do you need to start a microlending business?

Microlending usually needs a state-by-state legal review, not one national approval, because lending laws, APR limits, disclosures, servicing, collections, fair lending, and privacy rules can change by state and borrower type. Have counsel review each launch state, and budget about $2K/month for legal and advisory fees, $15K/month for data security and compliance, $1K/month for accounting and audit, and $500/month for insurance. One approval should not be assumed to cover all US operations, and scope rises as you add states, products, and pricing structures.

Launch-state checks

Check each state's lending license

Review APR and usury limits

Confirm disclosure forms and timing

Map servicing and collections rules

Budget anchors

Plan $2K monthly legal fees

Plan $15K monthly compliance spend

Plan $1K monthly audit costs

Plan $500 monthly insurance premium

What are the hidden costs of starting a microlending business?

A microlending business can look simple, but the hidden costs hit fast: loan loss reserves, borrower acquisition, servicing, compliance, and audit prep all need cash before the portfolio performs. In the source model, 100% Year 1 defaults and charge-offs equal $150K on a $15M first-year portfolio, and digital acquisition can run at 80% or $120K against first-year originations; if you want the owner math, see How Much Does The Owner Of Microlending Business Make?. Monthly tech alone can add $3K hosting, $800 software, and $15K security, before payment processing, credit data, fraud checks, collections workflows, and compliance monitoring.

Upfront cash needs

$150K loan losses in Year 1

80% digital acquisition cost load

Borrower onboarding and servicing support

Fraud checks and collections setup

Recurring operating costs

$3K monthly hosting

$800 monthly software

$15K monthly security

Compliance, accounting, audit readiness

Key Takeaways

Most setup costs are pre-opening professional expenses.

Software needs separate implementation, SaaS, and transaction fees.

Year 1 lending capital far exceeds startup overhead.

Weak screening can drive severe default losses.

Microlending Core Five Startup Costs

Microlending Licensing and Compliance Startup Expense

Launch Fees

This is a pre-opening professional expense, not CAPEX. It covers entity formation, license research, state applications, borrower disclosures, fair-lending and usury review, privacy review, servicing contracts, collections policies, and outside counsel. Budget $18.5K a month combines $2K legal, $15K data security/compliance, $1K accounting/audit, and $500 insurance.

What It Covers

Estimate it from number of states, loan products, borrower type, and online vs. local setup. Year 1 pricing at 280% to 350% lifts disclosure, fair-lending, and usury work. This spend belongs in launch overhead, because it has to be in place before the first loan closes.

Count state filings first.

Map each loan product.

Use one disclosure set.

Keep It Lean

Keep the stack lean by filing only where you plan to lend, standardizing disclosures, and using one policy set for servicing and collections. Coordinate outside counsel through one internal owner so reviews do not repeat. The common miss is adding states before the core forms are signed off.

Avoid duplicate reviews.

Lock templates early.

Delay extra states.

Cost Drivers

Online lending usually adds more privacy and data-security work than a local model, so the $15K monthly compliance line can move fast as scale grows. Treat these fees as ongoing operating support, not equipment spend. If onboarding takes longer, legal rework eats runway.

Initial Capital for Microlending Loans Startup Expense

Loan Pool First

For microlending, the startup cost is the loan pool, not equipment. Year 1 planned loans are $15M, so that cash has to sit as working capital before overhead, reserves, or growth spend.

Year 1 Mix

The table’s loan mix adds to $1.5M: $600K micro business, $400K agri finance, $200K education, $150K emergency household, and $150K women entrepreneur loans. Use this mix to size funding by product, term, and collection cycle.

$600K micro business loans

$400K agri finance loans

$200K education microloans

$150K emergency household loans

$150K women entrepreneur loans

Funding Setup

Year 1 pricing assumptions run from 280% to 350%, and the source funding line shows $135M. Founders need to confirm how much is deployable, how much is reserved, and whether the lending pool is fully funded before opening.

Reserve Cash

The model carries a 100% Year 1 default assumption, shown as $150K on the planned portfolio. Keep that reserve separate from the loan pool, because charge-offs and collections lag hit cash before interest income does.

Microlending Insurance and Marketing Costs Startup Expense

Insurance

For a microlender, professional liability and cyber coverage are pre-opening costs, not CAPEX. The source budget shows $500 a month in premiums, or $6K a year, plus related compliance and data protection spend. That matters because lending workflows handle borrower data, payments, and disputes from day one.

Launch spend

Build the budget around website setup, borrower outreach, local partnerships, and launch marketing, plus credit bureau and data tools and fraud prevention. If Year 1 originations are $15M and digital acquisition is 80% of spend, marketing equals $120K. These are early operating costs, so separate them from lending capital.

Cost control

Keep this spend tight by using fixed quotes for insurance, then scaling digital ads by funded-loan volume, not by impressions. The mistake is skimping on screening tools to save cash up front. Here’s the quick math: weak borrower review can push the 100% Year 1 default and charge-off assumption higher, so fraud checks protect both revenue and capital.

Risk tools

Put credit bureau, fraud, and data tools in the same budget line as marketing because they work together. Better screening lowers bad approvals, which matters when Year 1 charge-offs are assumed at 100%. If screening is thin, every extra dollar spent on outreach can feed losses instead of originations.

Microlending Software Costs Startup Expense

What it funds

This cost pays for the loan platform, not just a site. It covers the borrower application portal, underwriting workflow, loan servicing, payment processing integration, document storage, reporting dashboards, security setup, and audit trails.

Monthly run rate

Separate one-time implementation from recurring fees. The source budget shows $3K monthly hosting, $800 software subscriptions, and $15K data security and compliance, or $53K monthly before payment and credit data fees. This belongs in operating cash, not equipment.

Cost drivers

Use vendor quotes, months of coverage, and expected loan volume to price it. The biggest drivers are loan volume, integrations, user permissions, document retention, reporting depth, and support for all five first-year loan categories.

Keep scope tight

Start with the workflows you need on day one and add extras later. Limit permissions, keep reports lean, and avoid overbuilding audit features before launch. The usual mistake is buying every module upfront; that raises burn without improving underwriting or collections.

Microlending Staffing Costs Startup Expense

Core team

This cost covers underwriting, compliance administration, borrower support, collections coordination, finance, accounting, and outsourced specialists. Year 1 payroll is $425K, made up of a CEO at $160K, Head of Technology at $120K, Head of Risk and Underwriting at $100K, and a Customer Support Specialist at $45K. That is about $35.4K a month before benefits and taxes.

Budget build

Build the budget as pre-opening hiring and training plus ongoing payroll runway. Start with role count × salary, then add months of coverage for launch lag. Year 2 scale pressure adds a Senior Software Engineer at $90K, 0.5 FTE Data Scientist on an $85K salary, Operations Manager at $75K, and Customer Support at 20 FTE.

Runway watch

Keep early hiring lean and use outsourced specialists for legal, accounting, and compliance until loan volume is stable. Staff to underwriting volume, servicing complexity, and collections intensity, not hope. If borrower support or collections keeps rising, add headcount in steps, not all at once.

Scale trigger

Use pre-opening training to tighten underwriting rules, borrower scripts, and collections handoffs before launch. The payroll line gets dangerous when loan reviews slow down, because every extra manual check pulls time from support and finance. If the team can’t clear funded loans fast enough, staffing, not demand, becomes the bottleneck.