Performing Arts Startup Costs: Plan For $450K CAPEX And $707K Cash

The researched performing arts startup cost estimate includes $450,000 of CAPEX plus pre-opening expenses and working capital, with minimum cash reaching $707,000 in Month 6 That CAPEX includes $150,000 for seating, $80,000 for sound, $70,000 for lighting, $60,000 for HVAC, and other launch assets The first operating year revenue plan assumes 15,000 tickets at $65, 1,000 season subscriptions at $300, 500 workshop enrollments at $150, and $140,000 of added income Estimates vary by market, seating capacity, venue condition, union or contractor needs, and whether the business rents stages or operates its own venue

Calculate Fuding Needs

Startup cost summary

This table breaks down startup CAPEX and excluded cash needs for a live performing arts venue.

Highlighted CAPEX$450,000Base planning example

Excluded cash needs$707,000Outside CAPEX total

Funding need$1,157,000CAPEX + excluded cash needs

Cost Category

Base Estimate

Main Cost Driver

CAPEX Calculator

Theater Seating Upgrade

$150,000

Auditorium seating scope and install complexity

Yes

Sound System Installation

$80,000

Audio rig size and integration work

Yes

Lighting Rig Upgrade

$70,000

Lighting spec and rig installation scope

Yes

HVAC System Upgrade

$60,000

Mechanical upgrade size and venue condition

Yes

Stage and Back-Office Setup

$90,000

Stage equipment, office furniture, software, and website scope

Yes

Month 6 Minimum Cash Reserve

$707,000

Payroll, rent, and overhead funding gap

No

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only for a performing arts venue, not ongoing operating cash.

!

Excluded from CAPEX This covers capitalized startup assets only. It excludes inventory, payroll runway, deposits, debt service, working capital, marketing spend, rehearsal labor, rights, insurance premiums, and other operating costs.

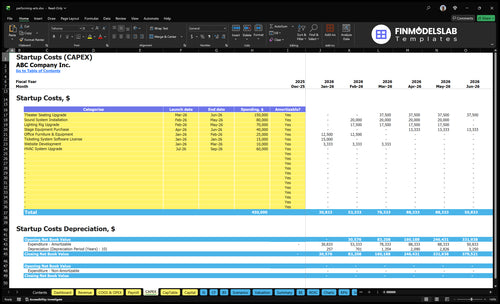

How does the Performing Arts CAPEX tab read?

This screenshot shows the Performing Arts Financial Model TemplateCAPEX/startup tab launch timing, costs, depreciation/amortization are listed. Open it and review assumptions.

Key screenshot highlights

$450k asset plan

Startup expense schedule

Ticket sales, subscriptions, workshops

Payroll and working capital

Month 1-60 model

Month 2 breakeven

18-month payback

Month 6 cash

Year 1 EBITDA $353k

Compare 3 Startup Cost Scenarios

Scenario table

Lean keeps costs down by renting stages and trimming staff. Base assumes a dedicated venue with the model's $450,000 CAPEX and $707,000 month 6 cash floor. Full adds larger spaces, HVAC, and heavier staffing.

Lean, base, and full launch cost comparison

Scenario

Lean LaunchTest-demand launch

Base LaunchDedicated venue

Full LaunchLarge venue build

Launch model

Use rented stages and a lighter production plan to test demand before committing to venue ownership.

Use a dedicated venue with the model's core build-out and steady year-round operations.

Use a larger multi-use venue with more seats, more systems, and a fuller team.

Typical setup

Keep the space rented, own only the basics, and staff the minimum needed for shows.

Build the dedicated venue and carry the model's $450,000 CAPEX plus the month 6 cash trough.

Add more seating, HVAC, sound, lighting, backstage space, and added staff.

Cost drivers

Venue rental

artist fees

basic production gear

marketing

ticketing fees

Seating upgrade

sound and lighting

rent

Year 1 payroll

working cash

More seating

HVAC upgrade

sound and lighting

backstage build-out

larger payroll

Planning rangeCAPEX only

$250,000 - $500,000Lower cash need

$1.1M - $1.2MModel base case

$1.5M - $2.2MHighest cash need

Best fit

Best for founders testing demand, pricing, and show mix before locking in a venue.

Best for operators ready to open a dedicated venue with predictable monthly spend.

Best for experienced teams that can fund a bigger build and manage more moving parts.

!

Planning note: These ranges are planning assumptions from the model, not exact vendor quotes or bids.

What are the biggest startup costs for a performing arts business?

For Performing Arts, the biggest startup cost is the room itself: a $150,000 seating upgrade, plus $80,000 for sound, $70,000 for lighting, and $60,000 for HVAC. Add $40,000 in stage equipment and a $15,000 ticketing software license, because code compliance, acoustics, backstage flow, dressing rooms, restrooms, accessibility, and control systems all push the buildout higher. The quick rule: the room costs more than the show if it isn’t performance-ready.

Venue costs first

$150,000 seating upgrade

Audience capacity drives revenue

Code compliance adds cost fast

Accessibility changes the layout

Systems and gear

$80,000 sound system installation

$70,000 lighting rig upgrade

$60,000 HVAC upgrade

$40,000 stage equipment

Backstage flow

Backstage flow affects turnaround

Dressing rooms need real space

Restrooms affect audience comfort

Rigging must match the show

Operations tech

$15,000 ticketing software license

Control systems need clean setup

Acoustics shape the audience experience

Performance-ready rooms cost more

How should founders fund a performing arts business?

Founders should fund Performing Arts with a Month 1 to Month 60 source-and-use plan tied to launch timing, ticket volume, subscriptions, workshops, facility rentals, concessions, sponsorships, payroll, and working capital. Here’s the quick math: the model hits breakeven in Month 2, pays back in 18 months, and shows $353,000 of Year 1 EBITDA, but cash still bottoms at $707,000 in Month 6. Test the plan against 15,000 Year 1 ticket units at a $65 average ticket price.

Funding plan

Match funding to launch timing

Use ticket sales as core revenue

Add subscriptions and workshops

Track facility rentals and concessions

Cash check

Breakeven lands in Month 2

Payback takes 18 months

Cash bottoms at $707,000

Validate CAPEX and working capital

How much does it cost to open a performing arts venue?

For Performing Arts, budget by model: a lean rented-stage launch can avoid most of the $450,000 venue capital spend (CAPEX), while a dedicated venue needs about $450,000 upfront and a $707,000 Month 6 cash need. Year 1 revenue math is 15,000 tickets × $65 = $975,000, plus 1,000 subscriptions × $300 = $300,000 and $140,000 added income, so track the demand driver behind that spend here: What Is The Most Critical Indicator For The Success Of Performing Arts Events?.

Cost Scenarios

Rented stage: lower buildout cash

Dedicated venue: $450,000 CAPEX

Month 6 cash need: $707,000

Multi-use space: higher operating load

Revenue Base

Tickets: $975,000 Year 1

Subscriptions: $300,000 Year 1

Added income: $140,000

Total assumed revenue: $1,415,000

Key Takeaways

CAPEX comes first; rent hits after opening.

Lighting and sound need heavy upfront cash.

Show mix drives sets, costumes, and royalties.

Payroll, marketing, and ticketing fees move break-even.

Performing Arts Core Five Startup Costs

Venue, Lease, And Stage-Readiness Startup Expense

Venue fit

The biggest check here is the venue itself: lease deposit, code-compliant build-out, and stage-ready fixes for audience flow, backstage space, dressing rooms, restrooms, accessibility, HVAC, acoustics, and storage. This model already carries $150,000 for seating and $60,000 for HVAC, so ask early about venue condition, capacity, landlord allowance, and fire and occupancy approvals.

Build-out CAPEX

Price the space by venue type: black box, theater, concert room, or mixed-use. A clean one-line budget is $210,000 in modeled CAPEX for seating plus HVAC, before any other improvements. The faster the room is close to code and stage-ready, the less you spend on demolition, rework, and delays.

Lease load

After opening, keep $15,000 rent out of CAPEX and treat it as operating cost. Add $2,500 monthly utilities and $1,500 maintenance, so fixed venue cash outflow is $19,000 per month before staffing and shows. A longer lease only works if ticket demand covers that base.

Approvals first

Lower cost by negotiating a landlord allowance, using the existing shell where possible, and deferring noncritical finishes until after approvals. Don’t cut the basics: accessibility, restrooms, acoustics, and HVAC affect both permits and patron experience. One weak inspection can delay opening and add carrying cost fast.

Sets, Costumes, Props, And Production Assets Startup Expense

Show Mix Costs

The cost changes with the season mix. Plays need sets, props, costumes, scenic materials, storage, and repair supplies. Concerts may need instruments, backline, monitors, stands, and risers. Dance may need flooring, mirrors, costume care, and rehearsal gear. In the model, carry show production costs at 50% of Year 1 revenue and artist fees and royalties at 70%.

Budget Inputs

Build this line from number of productions, unit quotes, and timing. Separate durable items from show-only spend: durable assets can be CAPEX, while sets, props, costumes, and consumables are operating or pre-opening costs. Ask how many productions open before ticket cash arrives, because that cash gap drives the working capital need.

Reduce Waste

Keep reuse high and buy only for the season. Rent special items, share risers or stands across shows, and track repair cost by title. The mistake is overbuying scenic stock too early; that ties up cash fast. If one item works in more than one production, it usually earns its keep.

Cash Timing

Ticket sales usually lag setup spend, so the first question is timing. If you mount several productions before the first box office cash comes in, this cost can front-load a big share of the Year 1 budget. That is why the production calendar and deposit dates matter as much as the design list.

Rights, Licensing, Permits, Insurance, And Compliance Startup Expense

Core checks

Business registration, local permits, occupancy approvals, and legal review are the gatekeepers. Budget the fixed stack at $2,200 a month: $1,000 insurance plus $1,200 legal and accounting. Then add quotes for play rights, music licenses, and workers’ compensation based on city, venue use, staffing model, and whether concessions are sold.

Music rights

Live music can trigger American Society of Composers, Authors and Publishers (ASCAP), Broadcast Music, Inc. (BMI), and SESAC licenses, depending on the program. Add play rights, performance approvals, and occupancy sign-off to the estimate. Size it by venue type, number of shows, and months of coverage, because U.S. rules change with the city and with concession sales.

Check city permit list first

Match rights to each show

Quote workers’ comp early

Year 1 load

Artist fees and royalties equal 70% of Year 1 revenue, so this line can outrun the fixed compliance budget. Here’s the quick math: if revenue is $100, $70 goes out before rent, payroll, or marketing. What this hides is programming mix; plays, concerts, and dance do not carry the same rights stack.

Permit risk

Don’t treat this like a filing fee. A missed permit or insurance proof can delay opening and add holding costs. Keep one checklist for registration, permits, liability insurance, workers’ compensation, and legal review, then update it when the lineup, staffing model, or concessions plan changes.

Stage Lighting And Sound Equipment Startup Expense

What It Covers

This startup cost covers lighting fixtures, a lighting rig, consoles, dimmers, microphones, speakers, monitors, cabling, projection, rigging, control booth gear, and installation. The model uses $80,000 for sound installation, $70,000 for the lighting rig upgrade, and $40,000 for stage equipment purchase. Build it from unit counts, install quotes, and room size.

Buy Or Rent

For early shows, buy the gear used every night and rent the specialty pieces tied to one-off productions or touring riders. That keeps cash free while you learn the real show mix. One line: buy repeat use, rent rare use. The decision hinges on show type, room size, and how often the setup changes.

Rent for one-off productions

Buy recurring core gear

Keep backup mics and cables

What Drives Cost

Price moves with show type, room size, touring artist needs, acoustic treatment, electrical capacity, technician setup time, and redundancy needs. A concert room often needs more speakers and monitors; a play may need more lighting control. Estimate each line from venue specs, rider demands, and install hours, not from a blanket per-seat number.

Match gear to room acoustics

Check power before buying

Plan for spare channels

Budget Fit

This is front-loaded CAPEX, so it hits cash before ticket sales do. Bigger rooms usually push up cabling, rigging, and install time, and thin redundancy can turn into a costly show delay. Keep the budget tied to the actual programming mix, because a dance night, a concert, and a touring act do not need the same system.

Pre-Opening Staffing, Rehearsal, Ticketing, And Launch Startup Expense

Launch team cost

Year 1 payroll is $515,000 for the artistic director, executive director, production manager, marketing, box office, administration, technical director, and education roles. That covers rehearsals, front-of-house training, ticketing setup, and opening-week operations. It is the biggest launch cash need, so staffing dates and first performance timing drive the burn rate.

Setup and systems

Pre-opening ticketing and web build need $15,000 for the ticketing software license and $10,000 for website development. Ongoing ticketing adds $500 per month, and ticketing fees take 20% of revenue. The estimate depends on months of setup, sales volume, and how much automation the box office needs.

Count setup months before opening

Price website build separately

Model fees on ticket revenue

Launch spend control

Launch marketing is sized at 40% of Year 1 revenue, so the fastest savings come from a tighter opening window and focused outreach. Use a short press list, local media first, and one clear opening-week plan. Don’t cut rehearsal or front-of-house training; weak opening nights cost more than the savings.

Use one launch calendar

Prioritize local press first

Protect rehearsal time

Opening-week cash plan

Here’s the quick math: $515,000 payroll, $25,000 in ticketing and website CAPEX, plus $500 monthly ticketing subscription, 20% ticketing fees, and 40% launch marketing against Year 1 revenue. What this hides is timing risk: if rehearsal and outreach slip, payroll starts before ticket cash does.