Owner income$692K-$14.4M

Owner income$692K-$14.4MBlockchain Consulting Owner Income: $180K–$144M Planning Range

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$692K-$14.4M  Net margin348%-751%

Net margin348%-751% Revenue for target pay$815K

Revenue for target pay$815K Business difficultyHard

Business difficultyHard

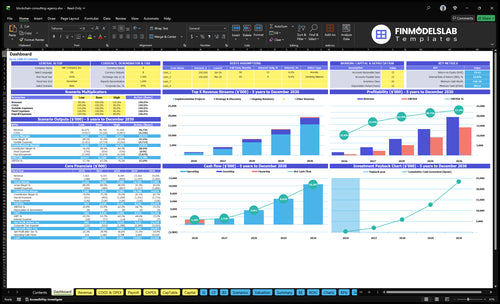

You’re planning owner pay before the agency is fully proven, so separate revenue from take-home This five-year US model shows $147M in Year 1 revenue, $512K in Year 1 EBITDA, and a $180K CEO salary, before personal taxes, reserves, debt service, or optional distributions These are planning assumptions, not guaranteed salary, tax advice, or automatic profit payouts

Owner income$692K-$14.4MNet margin348%-751%Revenue for target pay$815KBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Blockchain Consulting model?

Open the Blockchain Consulting Financial Model Template to see revenue, margin, costs, reserves, and owner take-home assumptions. Year 1 revenue is $147M, and the model is built as planning support.

Owner-income model highlights

- $512K Year 1 EBITDA

- $802K min cash, Month 2

- Breakeven in Month 5

- 9-month payback

- Pricing, retainers, mix

- Payroll, reserves, owner pay

How does scaling a blockchain consulting agency change owner income?

Scaling Blockchain Consulting can raise owner income, but only if the founder shifts from billable delivery into sales, strategy, partnerships, and quality control. In this model, senior consultants grow from 10 FTE to 40 FTE and junior consultants from 0 to 25 FTE by Year 5, with revenue rising from $147M to $1896M and EBITDA from $512K to $1423M.

Income upside

- More consultants means more delivery capacity.

- Higher revenue can lift owner pay.

- EBITDA growth supports more distributions.

- Sales-led growth reduces founder billable hours.

Key tradeoffs

- More management work replaces delivery time.

- Quality risk rises as headcount grows.

- Payroll increases before demand is proven.

- Income depends on keeping utilization high.

What revenue is needed to pay a blockchain consulting owner?

At the Year 1 cost mix, Blockchain Consulting needs about $815K of revenue before profit to cover the $180K owner salary, $460K payroll, $126K fixed overhead, and $50K marketing at a 78% contribution margin. That’s the break-even floor. If the owner wants $500K of total economic capacity, revenue rises to about $123M; for $1M, it’s about $187M before taxes, reserves, debt, and reinvestment.

Year 1 revenue floor

- $460K payroll must be covered

- $126K fixed overhead is next

- $50K marketing stays in the mix

- Need about $815K revenue before profit

Higher owner targets

- $500K capacity lifts revenue to $123M

- $1M capacity lifts revenue to $187M

- Taxes push the need higher

- Reserves and reinvestment add more

How much can a solo blockchain consultant make?

A solo Blockchain Consulting consultant’s take-home can’t be read from the agency model because Year 1 includes a $180K CEO, one senior consultant, one sales manager, and a half-time admin role. Model solo income from paid capacity; What Is The Most Important Measure Of Success For Blockchain Consulting? matters because sales or delivery gaps cut owner income fast.

Solo revenue inputs

- Strategy engagement: $3,750 in Year 1

- Implementation project: $24,000 in Year 1

- Modeled retainer unit: $1,600

- Use paid work, not agency EBITDA

Owner cash math

- Delivery and variable costs: 22%

- Strategy leaves $2,925 before overhead

- Implementation leaves $18,720 before overhead

- Retainer leaves $1,248 before overhead

Want to see what moves owner income most?

1

$250-$360/hrService Mix

More strategy work at $250 to $360 per hour lifts owner income fastest because each added billable hour brings in high-margin revenue.

2

15%-55%Retainers

Retainers rising from 15% to 55% of revenue smooth cash flow and raise lifetime value between project wins.

3

80-95hBillable Hours

Implementation hours moving from 80 to 95, plus higher retainer hours, spread team cost over more revenue.

4

12%-8%Delivery Cost

Lower software and expert fees from 12% to 8% keep more gross profit after delivery.

5

$2.5K-$1.8KPipeline Quality

Better pipeline quality and lower CAC help fill the bench with less spend, so more revenue turns into take-home.

6

$105K/moRisk Overhead

Fixed overhead near $105K a month later makes cost control critical because weak months hit owner income hard.

Blockchain Consulting Core Six Income Drivers

Service Mix And Deal Size

Deal Size and Mix

Short discovery work caps revenue. The modeled gap is stark: 15 hours at $250 produces $3,750, while implementation work at 80 hours at $300 produces $24,000. By Year 5, implementation rises to 95 hours at $360, or $34,200. That is where owner pay grows, but only if delivery stays tight.

Mix matters too: attach rates, meaning the share of clients that buy each service, move from strategy-heavy at 85% to implementation-heavy at 80%. So the owner sells more high-value work, but each deal also brings more review time, scope control, and delivery burden. Revenue rises only when those extra hours are priced in.

Price the Full Build

Track revenue by service type, not just closed deals. Separate strategy hours, implementation hours, and review time so you can see whether the added scope is lifting gross margin or just filling the calendar. If implementation work needs senior oversight, charge for it up front.

- Hours by work type

- Effective hourly rate

- Scope-change requests

- Unbilled review time

The rule is simple: bigger deal size should raise owner income, not hidden labor. If a project needs extra meetings, rework, or enterprise-readiness checks, bake that into the quote or the profit disappears.

1

Recurring Retainer Revenue

Recurring Retainer Revenue

Retainers smooth cash flow and cut empty-calendar risk, but they only help owner pay if the work stays tight. In this model, retainer attach rises from 15% in Year 1 to 55% in Year 5, while one unit moves from 8 hours at $200 or $1,600 to 11 hours at $240 or $2,640. That is more revenue per unit, not automatic profit.

Here’s the quick math: recurring work can add steady billings, but support hours, account management, and senior review can eat the margin fast. If a retainer needs unpaid fixes or heavy founder oversight, the owner’s take-home falls even when top-line revenue looks better. Clear service limits protect the draw.

Track Scope, Not Just MRR

Measure retainer attach rate, hours per client, and effective rate each month. The key inputs are active clients, retainer pricing, support hours, and senior review time. If a client is paying monthly but needs more than the plan allows, the work is no longer recurring profit. One clean contract can save many hours.

Set hard limits on revisions, calls, and turnaround time, then price overages before the work starts. Watch whether retainer hours stay near the modeled 8 to 11 hours per unit and whether the billed rate stays near $200 to $240. If scope creeps, raise price or reduce service depth so cash flow helps owner income instead of masking labor leakage.

2

Billable Utilization And Pricing

Billable Yield and Pricing

Owner income rises when paid strategy and delivery hours stay high at $250–$290 for strategy, $300–$360 for implementation, and $200–$240 for retainers. In the model, implementation grows from 80 to 95 hours per project while strategy drops from 15 to 12, so revenue improves only if those hours are truly billed and not crowded out by sales or admin time.

The key metric is effective billable yield: billed revenue after unpaid proposal, coordination, research, and review time. A project with 95 paid hours can still underpay the owner if 10–15 more hours slip out of scope. That gap cuts take-home income even when the posted rate looks strong.

Track Realized Rate, Not Just Rate Card

Measure billable utilization as paid hours divided by total work hours, then split it by strategy, implementation, and retainer work. Track nonbillable time for proposals, client calls, and rework too. If those hours rise, the same calendar produces less cash, and owner pay gets squeezed.

Test pricing against scope drift. If strategy is $250–$290 and implementation is $300–$360, raise rates when senior review, cleanup, or coordination increases. One underpriced project can erase the gain from a higher hourly rate.

- Track paid hours by service type.

- Log unpaid proposal time weekly.

- Compare quoted vs. realized rate.

- Flag scope creep before delivery.

3

Delivery Leverage And Subcontractor Costs

Subcontractor Cost Control

Specialists can raise delivery capacity, but they only help owner income when their cost is baked into the fee. In this model, third-party expert consulting sits at 7% of revenue in Year 1 and 5% in Year 5, while specialized software licenses drop from 5% to 3%. That moves combined COGS from 12% to 8%, so gross margin lifts from 88% to 92%.

Here’s the catch: if scope is loose, partner review, rework, and quality control eat the gain. Track revenue per project, subcontractor hours, rework rate, and software spend. If a $100,000 project needs $12,000 of COGS, gross profit is $88,000; at 8% COGS, it rises to $92,000. Owner pay improves only when pricing covers that extra delivery work.

Price Review Time Into Scope

Build the model from the bottom up: client revenue, subcontractor fees, license costs, internal review hours, and rework. Don’t treat specialists as free capacity. Use a clean scope sheet that names what the expert does, what gets reviewed by the owner, and what counts as out of scope. That keeps gross margin near the 88% to 92% band instead of leaking into unpriced labor.

- Track subcontractor cost as revenue %.

- Separate review from delivery hours.

- Cap rework by written scope.

- Test pricing against quality control time.

If senior review takes longer than planned, raise the fee or narrow the task. Otherwise, the firm can look busy while owner draw stays flat. The key test is simple: after subcontractor pay, software, and rework, does each project still leave enough gross profit to cover overhead and pay the owner?

4

Sales Pipeline Quality And Close Rate

Pipeline Quality And Close Rate

Client acquisition is a direct hit to owner income before it turns into growth. With $50K of annual marketing spend in Year 1 and $250K by Year 5, and CAC falling from $2,500 to $1,800, the modeled acquisition capacity is about 20 customers in Year 1 and 139 customers in Year 5.

The real driver is not lead count, it’s qualified proposals and close rate. Enterprise sales cycles also use non-billable founder time, so weak pipeline quality raises selling cost and pushes out profit. Here’s the quick math: if proposals don’ t close, marketing spend becomes overhead instead of revenue, and owner draw gets squeezed.

Track Qualified Leads, Not Raw Leads

Measure the funnel from lead to qualified proposal to closed deal, then compare that with CAC and founder hours spent per win. If close rate improves, each $1 of marketing buys more revenue and less wasted sales time. That protects gross margin and cash flow, which is what funds owner pay.

Track these inputs each month:

- Qualified proposals by source

- Close rate by segment

- CAC versus target

- Founder hours per deal

- Sales cycle length in days

If close rate slips, cut low-fit leads fast and tighten qualification before proposals go out.

5

Compliance, Insurance, And Risk Overhead

Risk Overhead

Compliance, insurance, and risk controls protect the firm, but they also cut into cash the owner can take home. Here, fixed overhead is $105K per month, including $500 for business insurance and $1,200 for legal and accounting. Add $92K of initial capex, and the business starts with a heavy cash load before owner pay.

The key input is whether billed work, collections, and utilization can cover that burn. With $802K minimum cash in Month 2, the firm needs a tight reserve plan. One missed client payment, slow close, or scope creep can turn “safe” controls into lower distributable profit fast.

Track Burn Before Paying Yourself

Watch fixed overhead, cash runway, and 13-week cash flow every week. Split out insurance, legal, accounting, security, and training so you can see which control is worth the cost. If billings slip, owner draws should wait until the forecast stays above the $802K Month 2 floor.

Use simple rules to keep risk spend from bloating. Tie security and compliance work to client needs, document scope early, and review each control against fewer incidents, less rework, or faster client approval. If a control does not protect revenue or reduce loss, it is just overhead eating take-home income.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with billable hours, staffing, and the mix of strategy, implementation, and retainers, so the spread from launch to mature year is wide.

| Scenario | Low CaseSetup risk | Base CaseHiring complexity | High CaseReserve discipline |

|---|---|---|---|

| Launch model | This is the lean launch path with one founder salary and limited surplus after early costs. | This is the core growth path with a larger consultant bench and stronger recurring work. | This is the scaled delivery path with the widest owner-income pool and the most moving parts. |

| Typical setup | Year 1 keeps staff light, runs a 22% variable load, and depends on early strategy work and setup reserves. | Year 3 uses a deeper team, a 19% variable load, and more implementation and retainer work to support income. | Year 5 runs a larger team, a 16% variable load, and a heavier retainer mix, but reserve discipline is still key. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $180K - $692KLean case | $180K - $5.36MBase case | $180K - $14.41MUpside case |

| Best fit | Use this to stress-test the business if sales ramp slowly or reserves need to stay high. | Use this as the main planning case for staffing, pricing, and cash reserve decisions. | Use this to test upside if hiring goes well and retainers carry more of the work mix. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Blockchain Consulting Porter's Five Forces Analysis

- Blockchain Consulting BCG Matrix

- Blockchain Consulting Business Model Canvas

- 7 Core KPIs to Scale Your Blockchain Consulting Practice

- Blockchain Consulting Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Blockchain Consulting Profitability

- How to Calculate Monthly Running Costs for Blockchain Consulting

- Blockchain Consulting Startup Costs: $92K CAPEX And $802K Cash

- Blockchain Consulting Financial Model Template in Excel

- How To Start A Blockchain Consulting Agency In 6 To 12 Weeks

- How to Write a Blockchain Consulting Business Plan: 7 Essential Steps

- Blockchain Consulting Marketing Mix

- Blockchain Consulting Marketing Plan

- Blockchain Consulting Business Proposal

- Blockchain Consulting PESTEL Analysis

- Blockchain Consulting Pitch Deck Example Editable PPTX

- Blockchain Consulting Business SWOT Analysis

- Blockchain Consulting Value Proposition Canvas

Frequently Asked Questions

In this researched model, the owner has a $180K CEO salary and possible distribution capacity only after reserves and reinvestment Year 1 shows $147M revenue, $512K EBITDA, and a 348% EBITDA margin Salary plus all EBITDA would equal about $692K before personal taxes, but that is not guaranteed take-home