Owner income$50.8k to $876.9k

Owner income$50.8k to $876.9kBook Publishing Company Owner Income: $51K To $877K Planning Range

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$50.8k to $876.9k  Net margin-35% to 31%

Net margin-35% to 31% Revenue for target pay$1.423M

Revenue for target pay$1.423M Business difficultyHard

Business difficultyHard

You’re planning owner pay around book sales, not a guaranteed salary In this five-year model, book sales revenue rises from $365,900 in Year 1 to $1,423,000 in Year 5, while owner income means CEO pay plus distributable profit after operating costs and reserves It is separate from author royalties, employee salaries, gross book revenue, and taxable income

Owner income$50.8k to $876.9kNet margin-35% to 31%Revenue for target pay$1.423MBusiness difficultyHardWant to test your publishing owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only; not guaranteed salary, tax advice, or owner distribution advice.

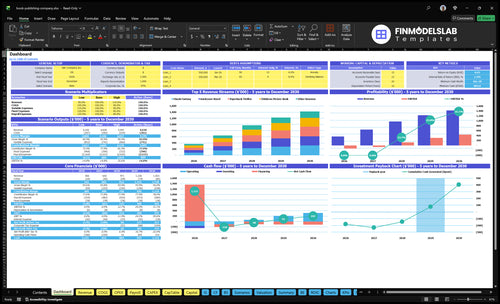

Want to check owner income in the Book Publishing model?

The dashboard shows Year 1–5 revenue, margin, costs, reserves, and owner pay; open the Book Publishing Financial Model Template.

Owner-income model highlights

- Revenue: $365.9k to $1.423M

- $353k annual overhead

- Owner pay before reserves

How can a book publishing company scale income?

Book Publishing scales by building a stronger title portfolio, not betting on one hit: volume grows from 22,000 units in Year 1 to 81,000 units in Year 5, and revenue rises from $365,900 to $1,423,000. The engine is repeat authors, backlist sales, rights licensing, direct sales, and disciplined acquisitions; the guardrails are title-level profit targets, reserve policies, channel discount tracking, and no fixed payroll growth before sell-through proves demand.

Growth drivers

- 22,000 to 81,000 units

- $365,900 to $1,423,000

- Repeat authors reduce launch risk

- Backlist builds steady sales

Risk controls

- Title-level profit targets

- Reserve policies for cash

- Channel discount tracking

- Hold payroll until sell-through

Can a book publishing company owner make a living?

Yes, a Book Publishing owner can make a living, but usually not from the first titles; in the researched case, Year 1 revenue is $365,900 with about $50,800 of owner-pay capacity before reserves. For the core metric behind that answer, see What Is The Main Success Indicator For Your Book Publishing Business?; a $120,000 CEO salary would create a roughly $69,200 operating loss.

Owner Pay Math

- $365,900 Year 1 revenue

- $50,800 owner-pay capacity

- $120,000 salary target

- $69,200 operating gap

Living Wage Path

- $641,975 Year 2 revenue

- $266,200 salary plus profit capacity

- Build deeper backlist

- Control reinvestment discipline

What affects book publishing gross margin and owner pay most?

Book Publishing gross margin and owner pay move most with format mix and unit cost, not just sales volume. For launch cost context, see What Is The Estimated Cost To Open And Launch Your Book Publishing Business?. Here’s the quick math: source unit COGS are $225 for hardcover, $121 for paperback, $0.10 for ebook, $0.38 for audiobook, and $180 for children’s picture books before fees, so small contract changes can swing owner pay fast.

Format costs

- $225 hardcover COGS

- $121 paperback COGS

- $0.10 ebook and $0.38 audiobook

- $180 children’s picture book COGS

Profit pressure

- 1-point royalty change moves profit $14,230

- $1 more print cost cuts profit $43,000

- Royalties rise from 80% to 100% of revenue

- Distribution and warehousing fall from 80% to 60%

Want to see the six owner-income drivers?

1

$366K-$1.42MPortfolio Performance

More units across the title mix lift revenue from about $366K to $1.42M, and that swing drives most owner take-home.

2

60%-80%Channel Mix

Shifting sales to lower-fee channels keeps more cash after distribution and warehousing costs, so the same revenue pays better.

3

80%-100%Rights Economics

Better royalty and rights terms change how much of each sale stays in-house, so small share changes hit income fast.

4

$0.10-$2.25Printing Costs

Unit COGS from $0.10 to $2.25 decides how much gross margin survives on every print run.

5

$275KMarketing Efficiency

Paid marketing and channel discounts are calculator inputs, so tighter acquisition protects the margin left after payroll.

6

$78KOverhead Discipline

Fixed overhead runs about $78K a year, so holding rent, software, and admin flat improves breakeven fast.

Book Publishing Core Six Income Drivers

Title Portfolio Performance And Backlist Depth

Backlist Depth Drives Owner Pay

The catalog is the revenue base. In the model, annual units rise from 22,000 to 81,000 across hardcover, paperback, ebook, audiobook, and children’s picture book formats, so owner pay becomes less tied to one launch month. Strong backlist depth matters because slow sell-through can leave payroll ahead of revenue, which hurts cash and pre-tax take-home.

This driver includes active titles, backlist age, format mix, and sell-through speed. The key input is units moving per title over time. When older books keep selling, gross profit arrives after launch costs, and income stays steadier. When they do not, the next release has to fund both overhead and the owner draw.

Measure Sell-Through By Title

Track units per active title by month, split by format and by title age. That shows whether revenue is coming from the front list or the backlist. If one title fades early, the catalog loses durability, and the owner’s pay becomes more volatile even if launch sales look fine.

Use a simple cohort report: launch month, months 2 to 6, and 6+ months. Flag titles that miss plan, then push price, merchandising, or format mix only where sell-through justifies it. A stronger backlist lowers the odds that $275,000 of payroll and $78,000 of fixed overhead outrun cash receipts.

1

Channel Mix And Net Publisher Revenue

Net Publisher Revenue by Channel

Owner income tracks net publisher revenue, not list price. If distribution and warehousing costs move from 80% of revenue to 60%, that frees up 20 percentage points before overhead. Here’s the quick math: the same title can look strong on paper but still leave thin cash if returns, fees, and channel cuts stay high.

Direct sales can lift take-home pay only when fulfillment and payment costs stay below the margin gained. Online marketplaces, bookstores, wholesalers, distributors, ebooks, and audiobooks all pay out differently, so the owner should judge each channel by cash left per sale, not by gross sales alone.

Measure Net Cash per Channel

Track net receipts by channel and compare them to the same title’s list price. Use units sold, average selling price, returns, fulfillment cost, and payment fees to find true contribution. If direct-to-reader orders leave more cash after shipping and card fees, shift more volume there.

- Compare net per unit by channel.

- Watch returns and fee drag monthly.

- Test direct sales on top titles.

Keep the rule simple: if a channel adds volume but cuts net receipts too hard, it can lower owner pay. A stronger mix is the one that keeps more cash after discounts, fees, and returns, then leaves room for editing, marketing, and profit draw.

2

Royalty And Rights Economics

Royalty and rights economics

Author royalties and advances sit on the publisher cost side, while rights licensing can add upside revenue if rights stay in-house and sell well. The model puts royalties and advances at 80% of revenue in Year 1 and 100% in Year 5; on $1,423,000 of Year 5 revenue, that line equals $142,300.

This line hits owner income directly because it changes publisher profit before overhead and therefore the cash available for distributions. The main risk is a large advance paid before sell-through shows up. One strong book can still strain cash if the advance lands months before sales do.

Track advance payback, then protect rights

Track advance size, sell-through, royalty accruals, and rights kept by title and format. If a book earns out faster, cash for owner pay arrives sooner; if it does not, that cost can hold distributions back for months.

Use bigger advances only when forecast sell-through supports them, and keep a clear list of rights that can be licensed later. Rights sales are clean upside when retained, but only if the contract, timing, and buyer list are in place.

- Check title-level royalty burn monthly.

- Match advances to sell-through pace.

- Retain rights with resale value.

3

Production And Printing Cost Control

Production and Printing Cost Control

Production and printing set title-level contribution margin before overhead. Source unit COGS are $225 hardcover, $121 paperback, $10 ebook, $38 audiobook, and $180 children’s picture book, plus small revenue-based fees. Every dollar cut from these costs lifts gross margin and leaves more cash for owner pay after overhead.

Print-on-demand can protect cash because you print after the order lands, but it usually raises unit cost. Offset printing can lower unit cost only when volume sells through. The risk is simple: if books do not move fast enough, low print cost is less useful than cash tied up in unsold inventory.

Track Unit COGS by Format

Measure units sold by format, net revenue per unit, and production plus printing cost on every title. Use this formula: title contribution margin = net revenue - unit COGS. If the margin on a title is thin, the owner’s take-home falls fast because less cash is left after editing, design, rights, and overhead.

- Track sell-through by title and format.

- Compare POD versus offset monthly.

- Watch revenue-based fees on each channel.

- Test price changes before adding volume.

Use offset only when planned volume is likely to clear, and use print-on-demand when cash protection matters more than unit cost. That tradeoff changes owner income directly: lower COGS improves gross margin, but excess inventory or weak sell-through can wipe out the gain.

4

Marketing Efficiency And Launch Payback

Launch Payback

Marketing only helps if it buys sell-through at a profit. With a $70,000 marketing manager on payroll and no separate paid ad budget, launch cost sits in publicity, reviews, email promotion, and reader acquisition. Payback means the title’s incremental gross profit covers those costs fast enough to lift owner draw.

Watch units sold per title, net revenue, and gross margin by channel. If a book’s conversion is weak, scaling spend can raise revenue but still cut contribution margin, so the owner ends up with less cash after launch. That’s the core risk.

Track Gross Profit, Not Rankings

Measure launch payback by comparing incremental gross profit against campaign spend for each title. The key inputs are sell-through, average net receipt per book, and title-level marketing cost. If gross profit does not exceed launch cost, the spend is buying noise, not income.

- Track title-level sell-through

- Log publicity and review spend

- Price reader acquisition cost

- Stop weak-converting ads fast

- Protect contribution margin

5

Fixed Overhead And Owner Workload Discipline

Fixed Overhead Discipline

Overhead sets the floor under owner pay. Here the annual cost base is $353,000: $78,000 fixed expenses plus $275,000 payroll, including $120,000 CEO pay. That is about $29,417 a month before any extra owner draw, so title profit has to cover that load first.

The key inputs are title contribution, staffing level, and pay timing. If sell-through is slow, payroll lands before revenue does, and Year 1 profit capacity turns into an operating loss. If contribution rises above $353,000, the excess can fund owner income and a reserve for the next launch.

Gate Hiring To Cash

Track overhead per title, monthly burn, and cash runway. A simple rule: do not add staff unless the new role has a clear link to more units sold, better rights income, or lower rework. Professional spend on legal and accounting at $14,400 is part of quality control, not a place to cut blindly.

- $78,000 fixed expenses

- $275,000 payroll total

- $120,000 CEO pay included

Separate the CEO salary from profit draw so the owner can see the real gap. If the model cannot support the full $353,000 cost base, hold hiring and keep workload tight until backlist sales and launch cash are stable.

6

Compare lean, base, and high-performing publishing income scenarios

Owner income scenarios

Owner income changes fast with unit mix, pricing, and royalty load. Year 1 is tight, Year 3 supports steady pay, and Year 5 gives room for stronger draws and reserves.

| Scenario | Low CaseEarly reinvestment | Base CaseSustainable payroll | High CaseReserve discipline |

|---|---|---|---|

| Launch model | This is the tight earnings path, where the business is still absorbing fixed overhead and building volume. | This is the modeled middle path, where the business starts paying the owner from steady volume and margin. | This is the stronger earnings path, where higher volume and better mix push owner pay capacity much higher. |

| Typical setup | Year 1 reaches about 22,000 units and $365,900 of revenue, with about $283,800 of contribution, $353,000 of overhead, and negative $69,200 operating profit after CEO salary. | Year 3 reaches about 57,000 units and $970,930 of revenue, with about $756,300 of contribution and about $523,300 of owner salary plus profit before reserves. | Year 5 reaches about 81,000 units and $1,423,000 of revenue, with about $1,109,900 of contribution and about $876,900 of owner salary plus profit before reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $50,800Cash tight | $523,300Payroll works | $876,900Strong cash |

| Best fit | Use this to stress-test launch year pay, cash burn, and how much owner income can exist before reserves get squeezed. | Use this as the core plan for budgeting, hiring, and owner draw decisions once the catalog is producing consistent sales. | Use this to test upside, but keep reserve discipline so higher pay does not outrun cash needs or growth investment. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Book Publishing Porter's Five Forces Analysis

- Book Publishing BCG Matrix

- Book Publishing Business Model Canvas

- 7 Essential KPIs for Book Publishing Success

- Book Publishing Business Plan Template in Pre-Written Word

- Increase Book Publishing Profitability: 7 Strategies for Founders

- Running Costs for Book Publishing: How to Budget Monthly Expenses

- How Much To Start A Book Publishing Company: $63K+ CAPEX

- Book Publishing Financial Model Template in Excel

- How To Open A Book Publishing Company In 3 To 9 Months

- How to Write a Book Publishing Business Plan: 7 Steps to Financial Clarity

- Book Publishing Marketing Mix

- Book Publishing Marketing Plan

- Book Publishing Business Proposal

- Book Publishing PESTEL Analysis

- Book Publishing Pitch Deck Example Editable PPTX

- Book Publishing Business SWOT Analysis

- Book Publishing Value Proposition Canvas

Frequently Asked Questions

In the researched model, Year 1 supports about $50,800 of pre-tax owner-pay capacity before reserves if the $120,000 CEO salary is not already paid By Year 5, the model supports about $876,900 of owner salary plus operating profit before reserves, taxes, and debt service, based on 81,000 units and $1,423,000 revenue