Owner income$4.9M

Owner income$4.9MHow Much Hops Farm Owners Make: $15K To $490K Before Reserves

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$4.9M  Net margin85.4%

Net margin85.4% Revenue for target pay$9.6M

Revenue for target pay$9.6M Business difficultyHard

Business difficultyHard

You’re estimating owner income from growing and selling hops to breweries, so this covers revenue, yields, acreage, costs, margins, reserves, and owner take-home The researched model runs from a 5-hectare first year to a 50-hectare mature year, with 75% yield loss, drying and processing costs, labor, fixed overhead, equipment needs, debt, and reinvestment treated as planning inputs This is not tax advice, a guaranteed return, or a generic farmer salary estimate

Owner income$4.9MNet margin85.4%Revenue for target pay$9.6MBusiness difficultyHardWant to test your hops farm owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

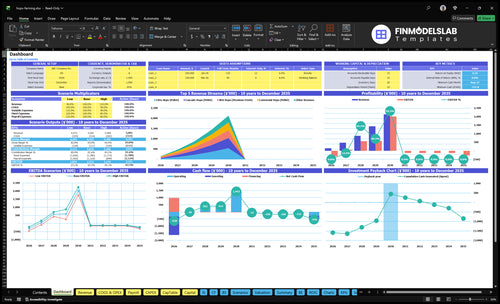

How do Hops Farming owner-income scenarios look in the model?

This screenshot in the Hops Farming Financial Model Template shows revenue, gross margin, operating profit, cash flow, and owner income scenarios. Charts compare $1.286M first-year revenue, $9.627M base-year revenue, and $28M mature-year revenue; cash flow starts negative, then base-year operating profit reaches $4.897M before owner pay and reserves. Open the model to stress-test the plan.

Owner-income model highlights

- Owner pay after reserves

- Revenue climbs to $28M

- Acreage and yield ramp-up

What risks affect hops farm owner income?

For Hops Farming, owner income is most exposed when the owner does field work, harvest coordination, quality control, sales admin, and brewery relationships directly. That can cut paid labor, but it also makes income less stable if harvest timing slips, drying quality drops, or a buyer backs out; with a 75% modeled yield loss, the downside gets severe fast. Here’s the quick math: one missed buyer commitment can turn strong revenue per acre into unsold inventory, so reserve planning has to cover crop loss, pricing, labor, and cash kept back for reinvestment.

Income risks

- 75% modeled yield loss

- Harvest timing can miss peak quality

- Drying issues can cut sale value

- Spot-price pressure can squeeze margin

Owner tradeoffs

- Owner labor can reduce paid costs

- Cold storage needs add cash pressure

- Contract gaps raise unsold-inventory risk

- Keep a reserve for reinvestment

What is the profit margin on hops farming?

Hops Farming can show a very high gross margin on paper, but the real profit margin depends on marketable yield, buyer price, and how much crop survives loss, processing, packaging, labor, water, pest control, and disease work. In the model, variable cost load falls from 180% in year one to 146% in the 20-hectare base year and 135% in the mature year; the base-year gross margin is about 854%, or $8,221K on $9,627K revenue. For startup spend, see What Is The Estimated Cost To Open And Launch Your Hops Farming Business? What this hides is fixed overhead, known payroll, debt service, reserve needs, and any crop rejected for quality.

Margin drivers

- Higher marketable yield lifts margin fast

- Better buyer price improves every kilogram sold

- Lower crop loss protects revenue

- Less processing and packaging cost helps

Margin drag

- Seasonal labor raises cash cost

- Water and pest control add steady spend

- Disease management can push costs up

- Fixed overhead can erase gross margin

How many acres of hops do you need to make money?

For Hops Farming, the model doesn’t make real money at small scale: 5 hectares equals about 12.4 producing acres and still runs negative, while 20 hectares, about 49.4 acres, supports $4.897M operating profit before owner pay and reserves; for market context, see What Is The Current Growth Rate Of Hops Farming Business?.

Acres That Struggle

- 5 hectares equals about 12.4 acres

- Revenue reaches $1.286M

- Overhead is $1.224M

- Known payroll adds $180K

Acres That Work

- 10 hectares equals about 24.7 acres

- Operating profit is only $151K

- 20 hectares equals about 49.4 acres

- Scale absorbs trellis, drying, harvest, sales

Want the six hops farm income drivers?

1

5-50 haAcreage Scale

The plan grows from 5 to 50 hectares, so more planted area is the main way to lift sellable volume and spread fixed costs.

2

1.1K-1.8K/haYield Capture

After the 7.5% yield loss, higher marketable output per hectare turns the same land into more hops sold.

3

$18-$40Hop Price

Variety pricing ranges from $18 to $40, and that spread drives revenue per pound more than small cost swings.

4

1-9 moSales Timing

Wet hops can sell in 1 month, while pellets take about 9 months, so contract mix changes cash tied up in inventory.

5

$265K-$430KPayroll Load

Known wage load rises fast as the team fills out, so staffing discipline is key to getting EBITDA above zero.

6

-$758KCash Trough

The model bottoms at about -$758K in Month 20, so reserve control matters if you want to avoid funding gaps before payback.

Hops Farming Core Six Income Drivers

Producing Acres

Producing Acres

Producing acres set the revenue ceiling. In this model, revenue rises from $1.286M at 5 hectares in year one to $9.627M at 20 hectares in the base year, then $28M at 50 hectares in the mature year. That is about $257K, $481K, and $560K per producing hectare, so every productive hectare matters.

Planted land is not the same as mature producing land. New acres still carry trellis, irrigation, harvest access, drying capacity, leases, insurance, and repairs, so small acreage can feel just as capital-heavy as larger acreage. If hectares stay immature, revenue lags while fixed field costs keep coming, which squeezes cash available for owner pay.

Track Mature Hectares First

Build the forecast from fully producing hectares, not total planted land. Here’s the quick math: revenue = producing hectares × marketable yield × price per pound. If a block is planted but not yet in full production, treat it as a ramp asset, not full revenue.

- Track hectares by age and block

- Separate planted from producing land

- Test harvest and drying capacity

- Compare land cost per productive hectare

What this estimate hides: if harvest access, drying space, or labor lags acreage growth, cash gets trapped in the field. Keep leases, insurance, repairs, and field infrastructure aligned with the hectares that can actually sell hops, or the extra land will not translate into owner income.

1

Marketable Yield And Quality

Marketable Yield and Quality

Revenue comes from sellable pounds, not harvested biomass. This driver covers harvested biomass, moisture, disease pressure, drying quality, and buyer specs. With 75% yield loss across the plan, only 25% becomes marketable, or about 1,096 lb/ha in year 1, 1,827 lb/ha in the base year, and 2,012 lb/ha in the mature year.

Quality hits income twice: rejected pounds and weaker pricing on accepted lots. If drying runs wet, disease shows up, or the lot misses buyer specs, gross margin drops and owner draw shrinks even when field yield looked fine. The business only gets paid on what the buyer accepts at spec.

Protect Sellable Yield

Measure harvested biomass, dry-down loss, and accepted pounds by lot. Compare each harvest to the 1,827 lb/ha base-year benchmark, because the gap shows fast if moisture or disease is eating revenue before cash hits.

Use moisture checks, scouting, and drying logs before harvest peaks. Keep lots clean and sorted to buyer grade, since better quality protects volume, price, and the cash left for payroll, debt service, and owner pay.

2

Price Per Pound And Contracts

Price Per Pound and Contracts

Price per pound turns sellable hops into revenue: $18 to $35 per pound in year one and $22 to $40 per pound in the mature year, based on the product mix. The owner’s income moves with the realized price, not the top quote, so every pound sold at spot rates can swing monthly cash flow and take-home pay.

Contracts matter because they smooth revenue and make lender and payroll planning easier. Spot sales can pay more in a strong market, but they also raise cash-flow risk if demand softens, quality slips, or freshness misses buyer specs. Local brewery ties help, but premiums still depend on variety, quality, demand, freshness, and buyer commitments.

Lock Price Mix Early

Track the share of pounds under contract versus spot, then model each crop at its expected realized price. Use realized price per pound = contracted pounds × contract price + spot pounds × spot price. Don’t assume every pound clears at the top of the range; that overstates revenue and can hide a weak cash year.

- Contracted pounds by variety

- Spot pounds left unpriced

- Buyer commitments before harvest

- Freshness and quality specs

- Realized price by batch

One clean rule: more contract coverage means steadier owner pay. If a crop leans too hard on spot sales, cash swings get wider and profit becomes harder to draw reliably, even when yield is strong.

3

Harvest And Processing Efficiency

Harvest and Processing Efficiency

When post-harvest work is sloppy, the owner keeps less cash from every sale. Modeled processing and packaging costs are 95% of revenue in year 1, then 80% in the base year and 75% in the mature year, so gross margin improves from 5% to 20% and 25% before labor, overhead, and debt.

Harvest hits in late summer, so picking, drying, pelletizing, packaging, cold storage, and freight must be ready before volume lands. Here’s the risk: delays or poor drying can raise shrink and wipe out premium pricing, which cuts owner take-home even if acreage and yield look strong on paper.

Control Post-Harvest Cost Per Pound

Track cost per processed pound, shrink rate, and time from harvest to dry. The key inputs are harvested pounds, accepted sellable pounds, drying capacity, packaging throughput, cold storage space, and freight cost. If drying or packing backs up, revenue quality falls and cash comes in later.

- Book capacity before late-summer harvest.

- Measure shrink by lot and variety.

- Reject wet or under-dried product fast.

- Match packaging runs to buyer specs.

4

Labor, Overhead, And Owner Involvement

Labor and Overhead

Paid labor, fixed overhead, and owner hours decide whether hop sales become cash the owner can actually take home. Known payroll is $180K in year one and $210K after the processing lead turns full-time, while fixed overhead runs $102K per month or $1.224M per year. Unpaid owner work is not income, so it should sit outside profit and draw.

Here’s the quick math: with year-one revenue at $1.286M, fixed overhead alone is about 95% of sales. Add seasonal labor at 35% of revenue and the cost base gets heavy fast, so the business only pays the owner if staffing, processing time, and management hours stay tight.

Track Labor, Then Pay Yourself

Measure payroll, seasonal labor as % of revenue, and overhead per month before setting owner draw. In year one, seasonal labor at 35% can crush margin; in the base year, with revenue at $9.627M, it falls to 28%, which leaves more room for profit. The target is simple: keep labor from rising faster than harvest volume and sale price.

Separate owner labor from owner draw. Track hours spent on planting, harvest, drying, and sales, then decide what part is unpaid management work and what part is true cash pay. If the farm cannot cover $1.224M of annual overhead plus payroll, owner time in the field is not free income.

5

Capital Costs And Reserves

Capital Costs And Reserves

This driver covers trellis systems, irrigation, tractors, harvest gear, drying space, land, loan payments, and replacement reserves. It matters because these costs come off cash before owner pay. In this model, land is 20% owned, with purchase price moving from $20K to $25K per hectare and lease cost from $250 to $300 per hectare per month.

Here’s the quick math: strong hop sales can still feel tight when debt service and equipment replacement hit after harvest. Reserves should be deducted before owner pay, or the business can look profitable on paper but leave too little cash for the next season. One line says it all: revenue is not take-home pay.

Track Cash Before Owner Pay

Build a cash forecast that separates operating profit from distributable cash. Track owned hectares, leased hectares, monthly lease per hectare, loan payment timing, and reserve funding for trellis, irrigation, tractors, harvest equipment, and drying space. If you don’t reserve for replacement, the first big repair can wipe out the owner draw.

Test pay scenarios after harvest, when cash is usually under the most strain. Use a simple rule: owner pay comes after debt service and replacement reserves. That keeps the business from overpaying the owner in a strong sales year and then scrambling for cash when equipment wears out or land costs rise from $20K to $25K per hectare.

- Track lease cost per hectare.

- Set reserve per harvested hectare.

- Forecast debt payments by month.

- Separate owner draw from reinvestment.

6

Compare lean, base, and high hops farm income scenarios

Owner income scenarios

Owner income swings hard with acreage, harvest loss, and contract volume. Small scale can stay cash negative, while larger planted area only works if buyers, reserves, and labor stay tight.

| Scenario | Low CaseScale risk | Base CaseContract need | High CaseReserve discipline |

|---|---|---|---|

| Launch model | This is the lower earnings path, with small acreage and tight pricing power. | This is the modeled path, with mid-scale acreage and enough volume to cover core costs. | This is the stronger earnings path, with large acreage and much higher output. |

| Typical setup | About 5 hectares, about $1.286M revenue, 180% variable costs, $1.224M fixed overhead, and $180K payroll leave owner income negative unless contracts improve. | About 20 hectares, about $9.627M revenue, 146% variable costs, and about $4.897M operating profit before owner pay and reserves set the middle case. | About 50 hectares, about $28M revenue, 135% variable costs, and about $209M operating profit before owner pay, debt, taxes, and reserves create the upside case. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Negative owner incomeCash negative | Positive owner incomeModerate upside | Strong positive incomeHigh upside |

| Best fit | Use this to stress-test a thin start where reserve cash and buyer contracts are not yet stable. | Use this as the working plan if buyer demand holds and the farm can sell through pellet and fresh hop channels. | Use this only if contracts, labor, and reserve cash can support a much larger operating footprint. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Hops Farming Porter's Five Forces Analysis

- Hops Farming BCG Matrix

- Hops Farming Business Model Canvas

- 7 Core Financial and Yield Metrics for Hops Farming

- Hops Farming Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Hops Farming Profitability

- Calculating the Monthly Running Costs for Hops Farming

- Hops Farm Startup Costs: 5-Hectare Launch Budget Guide

- Hops Farming Financial Model Template in Excel

- How to Start a Hops Farm With a 9–18 Month Launch Plan

- How to Write a Hops Farming Business Plan: 7 Steps to Financial Clarity

- Hops Farming Marketing Mix

- Hops Farming Marketing Plan

- Hops Farming Business Proposal

- Hops Farming PESTEL Analysis

- Hops Farming Pitch Deck Example Editable PPTX

- Hops Farming Business SWOT Analysis

- Hops Farming Value Proposition Canvas

Frequently Asked Questions

A hops farm owner can make nothing in early years and much more at scale In the researched model, 5 hectares produces $1286K revenue but negative operating profit after $1224K fixed overhead and $180K known payroll At 20 hectares, operating profit before owner pay, debt, taxes, and reserves is about $4897K