Owner income$199-$232/visit

Owner income$199-$232/visitHow Much House Call Doctor Owners Make: $103M Year 1 Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$199-$232/visit  Net margin40%-73%

Net margin40%-73% Revenue for target pay$2.2M

Revenue for target pay$2.2M Business difficultyMedium

Business difficultyMedium

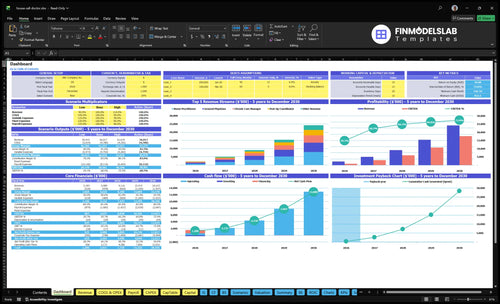

A house call doctor service owner can make strong income only if completed visit volume, collections, and staffing stay disciplined In the researched assumptions, Year 1 revenue is about $218M, with $103M operating profit after supplied variable costs, fixed costs, and a $280k Medical Director salary By Year 5, modeled revenue reaches $2421M and operating profit reaches $1962M, but that figure excludes taxes, debt service, reserves, reinvestment, and any provider payroll not included in the data Treat these as planning assumptions, not wages, guaranteed distributions, tax advice, or a substitute for a full financial model

Owner income$199-$232/visitNet margin40%-73%Revenue for target pay$2.2MBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only; not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the House Call Doctor Service model?

This dashboard shows revenue, margin, costs, reserves, and owner take-home assumptions; open the model.

Owner-income model highlights

- Owner pay split clearly

- Revenue and margin charts

- 3 to 15 physicians

- 4 to 25 nurse practitioners

- 50% to 90% utilization

- $367k monthly overhead

What are the main house call doctor business expenses?

House Call Doctor Service costs split into two buckets: visit-linked costs and fixed overhead. For a quick read, the How Much To Start House Call Doctor Service? page helps frame the setup, but the biggest operating drag is still the recurring base cost. Year 1 visit-linked costs are 20% of revenue, and fixed overhead is listed at $367k per month.

Visit-linked costs

- 20% of revenue

- 45% supplies

- 55% lab and diagnostic fees

- 60% fuel and vehicle maintenance

Fixed overhead

- $367k per month total

- $12k malpractice

- $85k vehicle fleet lease

- $65k admin hub rent

Billing and claims fees make up the rest of the variable load at 40%, so the visit margin can look healthy on paper. But owner take-home still gets squeezed after provider payroll, reserves, taxes, and reinvestment.

Other monthly overhead

- $45k marketing

- $22k software

- $18k IT

- $12k licensing

What this means

- Gross margin can look strong

- Fixed costs stay high each month

- Payroll cuts owner cash fast

- Reserves and taxes matter

Can a house call doctor business scale beyond the owner?

Yes—House Call Doctor Service can scale beyond the owner, but only if staffing, credentialing, and payer setup keep pace. Over five years, the model grows from 3 to 15 general physicians, 4 to 25 nurse practitioners, 1 to 8 geriatric specialists, 2 to 15 chronic care managers, and 1 to 10 post-op coordinators. Owner-led visits can bring more direct income early, but they also cap capacity fast.

Scale path

- 3 to 15 physicians in 5 years

- 4 to 25 nurse practitioners

- 1 to 8 geriatric specialists

- 2 to 15 chronic care managers

Main risks

- Credentialing and supervision add load

- State licensing rules vary by market

- Late payer enrollment can delay revenue

- Scheduling and quality control get harder

How much can a house call doctor charge per visit?

For a House Call Doctor Service, use net collections, not sticker price: Year 1 visits can range from $150 for chronic care management to $300 for geriatric specialist visits, and the weighted average collection is about $199 per completed visit, rising to about $232 by Year 5. What you actually keep shifts with cash-pay, concierge, Medicare, Medicaid, commercial insurance, employer contracts, and facility contracts, plus geography, coding, credentialing, medical necessity, patient responsibility, and collection rate. So the quote is only step one; the real number is the collected amount.

Year 1 to Year 5

- $150 to $300 per visit.

- $199 average collection in Year 1.

- $232 average collection by Year 5.

- Count completed visits, not billed charges.

What moves the number

- Cash-pay and concierge speed cash.

- Medicare and Medicaid change rules.

- Commercial, employer, and facility contracts vary.

- Geography and coding move collections materially.

Want the six main income drivers?

1

916-8.7k/moVisit Volume

More completed visits drive most of the revenue, scaling from 916 monthly visits in Year 1 to 8,679 in Year 5.

2

$199-$232Visit Value

A higher net collection per visit lifts take-home fast because the gain multiplies across every completed house call.

3

3-25 FTEStaffing Mix

The split between physician time, nurse practitioners, and other clinicians sets labor cost and visit capacity.

4

Cash lagPayer Timing

Insurance lag ties up cash, while faster reimbursement keeps more of each visit available for payroll and owner draws.

5

5%-6%Route Efficiency

A tighter service area lets each clinician fit more visits into a day and keeps fuel and vehicle costs near the 5% to 6% range.

6

$36.7K/moOverhead Reserve

Fixed overhead totals $36.7K a month, and the $832K cash trough in Month 2 means reserve discipline protects owner pay.

House Call Doctor Service Core Six Income Drivers

Completed visit volume

Completed Visit Volume

Completed visit volume is the main revenue capacity lever here, because the model counts capacity-adjusted visits, not theoretical appointment slots. It runs from 916 visits per month in Year 1 to 8,679 per month in Year 5, so the business can scale only if providers actually finish more house calls. Each completed visit adds collected revenue, so missed visits hit owner pay fast.

What can shrink volume: travel gaps, documentation delays, complex cases, no-shows, a wide service radius, and provider burnout. More visits help income only if clinical quality stays safe. If the schedule gets tighter but care gets rushed, you can lose revenue later through rework, complaints, and churn. One clean rule: more completed visits should mean more cash, not more risk.

Track and Protect Visit Capacity

Track completed visits per provider per day, not booked slots. Break it down by ZIP code, visit type, no-show rate, drive time, and documentation time, so you can see where capacity leaks. Here’s the quick math: moving from 916 to 8,679 monthly visits is about a 9.5x jump, so small process gains matter a lot.

Use routing, reminder calls, and same-day charting to keep visits moving. If one provider is carrying too many complex cases or too much windshield time, volume drops and owner income follows. The target is simple: keep the schedule full, keep care safe, and keep the visit actually closed out.

1

Net collections per completed visit

Net collections per completed visit

Net collections per completed visit is the cash you actually keep for each house call, not the charge on the claim. In year 1, the weighted average is about $199 per completed visit, with service prices from $150 to $300. By year 5, the average rises to about $232 as higher-priced visit types take a bigger share.

This drives owner income because every collected dollar lifts gross margin and pay. Use collected cash, not billed charges, because denials, patient balances, payer contracts, and claim timing all change what lands in the bank. A $10 move across 916 monthly visits changes annual revenue by about $109,920 before costs.

Track cash, not charges

Measure cash collected ÷ completed visits each month, then split it by payer, visit type, denial rate, patient responsibility, and days to cash. That tells you whether pricing, payer mix, or billing lag is hurting take-home income. If collections per visit drift down, the owner's draw usually follows.

- Completed visits by visit type

- Collected cash by payer

- Denials and patient balances

- Days to cash

- Price mix across visit types

Push higher-priced visit types only when the billing team can collect cleanly. The year 5 benchmark of $232 depends on a richer mix, not wishful pricing. If claims slow down, keep more working capital before increasing owner pay.

2

Payer mix and reimbursement timing

Payer Mix and Cash Timing

Payer mix changes both revenue per visit and cash timing. Cash-pay and concierge visits usually collect faster, but they can narrow demand. Medicare, Medicaid where applicable, and commercial plans may widen volume, but they add coding, medical necessity proof, credentialing, denials, and billing lag.

For the owner, this driver changes how fast visits turn into take-home pay. Model collections per visit, days to cash, denial rate, and patient responsibility, not billed charges. Employer or facility contracts can improve scheduling density, but payer mix should stay a sensitivity, not a promise.

Track Collections, Not Charges

Split visits by payer bucket and compare collected cash, days to cash, and denials each month. That shows whether a higher-volume payer is actually improving owner income or just delaying it.

- Measure collections by payer monthly.

- Track denial reasons and appeals.

- Watch patient balances by visit type.

- Test contract terms before scaling.

If billing lag grows, cash flow tightens even when visit volume looks fine. More visits do not equal more pay unless the money clears fast enough to cover payroll, overhead, and owner draw.

3

Clinical staffing model

Clinical staffing mix

Staffing is the main cap on owner income here. The model scales nurse practitioners from 4 to 25 and general physicians from 3 to 15 over five years, so each hire can raise completed visits and collections. But pay only improves if each clinician is fully loaded and the schedule stays tight; empty travel time or slow credentialing turns payroll into drag.

Early owner-physician delivery can keep payroll lean, but it also caps visits. Once employed clinicians come in, model provider payroll, supervision, licensing compliance, scheduling support, and quality checks separately from owner draw. The supplied $280k Medical Director salary is one input; it does not replace the rest of clinical labor costs.

Track clinician capacity fast

Track visits per clinician per day, paid travel time, no-shows, and case mix. Here’s the quick math: if more staff do not lift completed visits faster than payroll grows, owner income falls. Use one schedule view for demand, one for capacity, and one for credentials so you can see when the next hire actually adds margin.

Before adding staff, test whether the role will improve cash, not just volume. Watch collections per visit, labor as a share of revenue, and days to fill the schedule after hiring. If onboarding takes too long, the practice can look busier and still pay the owner less.

- Model payroll by role.

- Separate medic al director cost.

- Stress-test staffing ramp.

4

Route efficiency and service area density

Route Density

When house calls are spread across a wide area, the service can look full but still pay poorly. In the model, fuel and vehicle maintenance run at 60% of revenue in Year 1, which means only 40% is left before fixed overhead; by Year 5, that falls to 50%, so margin improves if routes stay tight.

Here’s the quick math: every $100,000 of revenue leaves about $40,000 in Year 1 and $50,000 by Year 5 before overhead. The inputs are completed visits, miles per stop, paid windshield time, ZIP code mix, visit type, and provider skill. Dense routes raise cash by fitting more billable care into the same day.

Cluster by ZIP and visit type

Track visits per route hour, miles per completed visit, and % of stops in the same ZIP. Group appointments by ZIP code first, then by visit type and provider skill. That cuts drive time, lowers empty miles, and helps patients get seen on time. Dense routing only helps if it does not stretch clinical quality or create rushed visits.

- Measure windshield time daily.

- Cluster stops before booking.

- Match visit type to skill.

- Test tighter service zones.

What this changes is owner pay: less time driving means more completed visits and less variable cost, so more cash is left after visit labor and vehicle costs. Broad geography can hide weak economics until fuel, maintenance, and late arrivals start eating the month.

5

Overhead, reserves, and reinvestment

Overhead Before Owner Draw

In this house call model, overhead is the cash wall between collected revenue and owner take-home. Fixed costs total $367k per month, led by $85k for vehicle fleet lease, $65k for admin hub rent, $45k for marketing, and $12k for malpractice. Owner pay only works after working capital, reserves, taxes, debt service, software, compliance support, supplies, and reinvestment are covered.

This matters because cash timing can break the link between profit and spendable income. Claims lag and vehicle repairs can hit in the same month, so a strong revenue month can still leave the owner short if reserves are thin. The real test is not just profit on paper; it’s whether collected cash clears the $367k fixed base and still leaves room for delay and downtime.

Protect Cash Before Paying Yourself

Track the monthly fixed-cost base, days of claims outstanding, fleet repair spend, and reserve balance. If the practice cannot cover the full $367k plus near-term timing gaps, owner draw should wait. That keeps one bad billing month or one broken vehicle from turning into a cash crunch.

- Forecast overhead by line item monthly.

- Separate reserves from operating cash.

- Set owner draw after taxes and debt.

- Watch claims lag and repair spikes.

- Reinvest before increasing personal pay.

6

Owner income scenario table objective

Owner income scenarios

Owner income moves fast here because visit volume, collections per visit, staffing load, and fixed overhead all rise and fall together.

| Scenario | Low CaseStaffing and payer risk | Base CaseModeled run rate | High CaseScale with timing risk |

|---|---|---|---|

| Launch model | This is the downside case, with fewer visits, weaker collections, and thinner route productivity. | This is the source Year 1 case, with 916 monthly visits and $199 average collections. | This is the Year 5 scale case, with 8,679 monthly visits and higher collections. |

| Typical setup | Visits run below Year 1 capacity, collections slip, marketing rises, and payroll stays heavy for the volume. | The model runs 3 General Physicians, 4 Nurse Practitioners, 1 Geriatric Specialist, 2 Chronic Care Managers, and 1 Post Op Coordinator at Year 1 capacity. | Staffing expands to Year 5 capacity, collections improve, and the model pushes more volume through the same service mix. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Below $867kPressure case | $867kCore plan | $17.7MUpside case |

| Best fit | Use this to test weak referrals, slower claims, and underused clinicians. | Use this for budget, hiring, and lender planning. | Use this to test expansion upside, staffing depth, and payer timing strain. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- House Call Doctor Service Porter's Five Forces Analysis

- House Call Doctor Service BCG Matrix

- House Call Doctor Service Business Model Canvas

- What Are The 5 KPI Metrics For House Call Doctor Service Business?

- House Call Doctor Service Business Plan Template in Pre-Written Word

- How Increase House Call Doctor Service Profits?

- What Are Operating Costs For House Call Doctor Service?

- House Call Doctor Service Startup Costs: $85K CAPEX Plus Runway

- House Call Doctor Service Financial Model Template in Excel

- How To Start A House Call Doctor Service In 90 To 180 Days

- How Do I Write A Business Plan For House Call Doctor Service?

- House Call Doctor Service Marketing Mix

- House Call Doctor Service Marketing Plan

- House Call Doctor Service Business Proposal

- House Call Doctor Service PESTEL Analysis

- House Call Doctor Service Pitch Deck Example Editable PPTX

- House Call Doctor Service Business SWOT Analysis

- House Call Doctor Service Value Proposition Canvas

Frequently Asked Questions

In the supplied model, the owner-pay pool starts from about $103M Year 1 operating profit before taxes, debt service, reserves, and distributions That sits on $218M revenue, 916 monthly visits, and a $199 average collection per visit Actual take-home depends on whether the owner takes the $280k Medical Director salary and how much cash the practice retains