Time to Open6-9 monthsSetup window

Time to Open6-9 monthsSetup windowHow To Open An Online Currency Exchange With $10M Deposits

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Time to Open6-9 monthsSetup window  Launch Sequence5 stagesCompliance first

Launch Sequence5 stagesCompliance first Key BottleneckLicense gateApproval path

Key BottleneckLicense gateApproval path First Revenue StepFirst exchangeSpread or fee

First Revenue StepFirst exchangeSpread or fee

To start an online currency exchange in the US, define your currency corridors, form the entity, assess Financial Crimes Enforcement Network MSB registration, review state money transmitter licensing, secure banking and liquidity partners, and build KYC, AML, OFAC, and transaction monitoring workflows The timeline is not fixed because licensing, bank onboarding, processor approval, and liquidity integration can each block launch The researched planning case assumes Year 1 customer deposits of $10,000,000, regulatory capital of $5,000,000, and loan assets starting at $2,500,000 across five credit categories First revenue should come from one compliant customer exchange with a tested spread or fee, not from high-volume traffic before controls are proven

Time to Open6-9 monthsSetup windowLaunch Sequence5 stagesCompliance firstKey BottleneckLicense gateApproval pathFirst Revenue StepFirst exchangeSpread or feeLaunch timeline

Short web summary of the launch plan; the XLSX export holds the full Gantt chart.

Launch scheduleWeek 1Week 2Week 3Week 4Week 5Week 6Week 7Week 8Week 9Week 10Week 11Week 12

Legal / compliance

- MSB Review

- State License Map

- AML Policy Draft

- Sanctions Screening

- Recordkeeping Rules

Banking / rails

- Bank Shortlist

- Bank Onboarding

- ACH Setup

- Wire Setup

- Reconciliation Rules

Liquidity / pricing

- Provider Shortlist

- Rate Feed Setup

- Spread Rules

- Corridor Limits

- Funding Buffer Plan

Platform / security

- Onboarding Flow

- Quote Engine

- Payment Confirmation

- Transaction Ledger

- Security Hardening

Operations / staff

- Compliance Hire

- Support Hire

- Customer Verification

- Escalation Playbook

- Finance Controls

Launch / growth

- Sandbox Transfers

- Rate Checks

- Exception Handling

- Soft Launch

- Customer Outreach

Why test launch assumptions before taking customer funds?

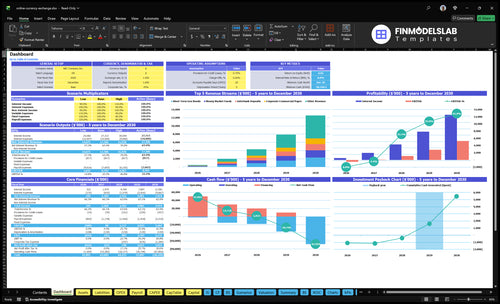

Use the Online Currency Exchange Financial Model Template to test launch timing; the screenshot shows revenue, costs, cash needs, assumptions, and break-even logic.

Key model highlights

- Year-1 deposits $10M

- Regulatory capital $5M

- Loan assets $2.5M

- Interest assets $17M

- Deposits hit $180M Year-5

- Capital reaches $8M

Use tabs for revenue ramp, liquidity, staffing, compliance costs, payment fees, bank settlement timing, cash runway, and scenario controls. It validates assumptions, but it does not replace legal or bank approval.

How long does it take to launch an online currency exchange?

Launching an Online Currency Exchange usually takes months, not weeks, because approvals move slower than code; the platform can be built in parallel, but customer transactions wait for licensing, bank partner review, payment processor approval, liquidity provider integration, compliance testing, and security review. The biggest delays are bank partner delay, money transmitter licensing, incomplete AML controls, unresolved settlement steps, and failed KYC testing. For scale planning, Year 1 customer deposits of $10,000,000 and regulatory capital of $5,000,000 mean you should not promise a fixed opening date until rails and compliance are approved.

Big delays

- Bank partner review slows launch

- Licensing varies by state scope

- AML controls must be complete

- KYC tests must pass cleanly

What can run now

- Build the platform in parallel

- Prepare compliance documents early

- Integrate liquidity providers carefully

- Wait for approval before transactions

How does an online currency exchange get first customers?

The first customers for an Online Currency Exchange should come from one narrow corridor and a trusted niche, not a broad launch; start with transparent rate comparison, clear fees, and referral partners. To size the launch, compare demand against $10,000,000 in Year 1 customer deposits and $500,000 in liquidity facilities; if you need a cost benchmark, see What Is The Estimated Cost To Launch Your Online Currency Exchange Business?. First revenue comes only after a compliant exchange passes KYC, OFAC, payment confirmation, and reconciliation.

Find first users

- Pick one or a few currency corridors.

- Start with a trusted niche.

- Show live rates and clear fees.

- Use referral partners and a controlled campaign.

Protect early revenue

- Charge a spread or fee after compliance.

- Finish KYC, OFAC, confirmation, reconciliation.

- Delay volume until fraud and AML controls work.

- Trust beats discounts at launch.

Do you need a license to start an online currency exchange?

Yes—an Online Currency Exchange should assess licensing before it handles customer funds, because currency conversion, custody, transfers, stored value, and settlement can trigger FinCEN money services business registration, Bank Secrecy Act anti-money laundering duties, OFAC sanctions compliance, and state money transmitter licensing; start with What Is The Primary Goal Of Your Online Currency Exchange Business? so the regulated activity is clear. Practical launch order: legal review, entity setup, compliance program, bank onboarding, processor approval, then customer transactions; this is planning guidance, not legal advice.

License checks

- Register with FinCEN within 180 days

- Renew MSB registration every 2 years

- Review up to 50 state rules

- Map every customer fund flow

Readiness signals

- Write an AML policy

- Screen OFAC sanctions before transfers

- Keep $3,000+ transfer records

- Name one compliance owner

Confirm the platform is ready to accept real customer transactions

Launch readiness checklist

Use this go-live approval checklist to confirm an online currency exchange is ready before opening.

Regulatory setup

- Entity formedCritical

The entity must exist before licenses, accounts, and contracts.

- MSB status assessedCritical

Money services status should be confirmed before customer funds move.

- State licenses mappedCritical

State filing gaps can block launch in some jurisdictions.

Banking rails

- Bank partner approvedCritical

No settlement can start without a cleared bank partner.

- Payment processors approvedHigh

Payment rails must work before live FX trades.

- Settlement accounts liveCritical

Client money needs live accounts before go-live.

Controls

- AML program writtenCritical

The AML program sets the rules for suspicious activity.

- KYC workflow liveCritical

Identity checks must work before the first customer.

- OFAC screening enabledCritical

Sanctions checks must block restricted names before trade.

Liquidity

- Liquidity provider connectedCritical

FX trades need funding access to settle fast.

- FX pricing engine workingCritical

Live quotes must update before customers place trades.

- Trade limits setHigh

Trade caps help control exposure in the first month.

Operations

- Reconciliation process documentedHigh

Daily match-up keeps cash, trades, and ledgers aligned.

- Customer support staffedHigh

Support needs coverage before failed trades start arriving.

-

Fraud controls activeCritical Fraud blocks reduce chargeback and account-loss risk.

Finance

- Runway covers Month 18Critical

The cash trough reaches -$30.169M by Month 60.

- Year 1 model checkedCritical

The model should match $10M deposits, $5M capital, and $2.5M loan assets.

- Go-live signoff signedCritical

Open only after compliance, rails, and liquidity pass.

Which six launch drivers decide if the exchange can open safely?

1Licensing

License gateNo launch moves until policies, owner, and records clear bank review and state approval.

2Bank Rails

$10M depApproved settlement rails are the launch path; bank delays can outrun the software build.

3FX Pricing

$500KLive rates and corridor limits protect first trades from stale quotes and loss-making spreads.

4Risk Controls

WatchlistIdentity checks and watchlist screening cut fraud, frozen transfers, and bank rejection risk.

5Platform Ops

Tested flowA tested order-to-ledger flow reduces failed transfers, support tickets, and manual fixes.

6Corridor

NarrowA narrow corridor and clear fees build trust faster while keeping support and limits manageable.

Licensing And Compliance Path

Licensing and Compliance First

This is the first launch gate. If the exchange is handling customer funds before legal clearance, launch can stall fast. Banks and processors will usually review FinCEN MSB registration, state money transmitter licensing, the AML program, OFAC screening, and recordkeeping before they approve rails.

Readiness means more than filing forms. You need written policies, a named compliance owner, customer due diligence, monitoring rules, an escalation process, and an audit trail. That is what lowers bank friction and cuts approval resets before day one.

Build the Compliance Packet Before Funds Move

Start with a clear regulated-activity review, then lock the filing path and operating controls. If the sequence is wrong, you can burn weeks reworking the banking packet or get stopped after onboarding has already started. One clean compliance file beats three rushed fixes.

Use a simple launch checklist: license map, policy set, owner named, due diligence steps, monitoring rules, escalation tree, and retention process. Then test the evidence trail with the bank or processor review so the first approval is also the last one you need before opening.

- Map regulated activity first.

- File MSB and state licenses.

- Document AML and OFAC steps.

- Name the compliance owner.

- Keep records ready for review.

1

Banking And Payment Rails

Banking And Payment Rails

This business cannot open on time without a bank that will support ACH, cards, wires, settlement accounts, refunds, and chargebacks. If the bank or processor is still reviewing the model, the platform may be built but customers still can’t fund or receive exchanges, which pushes launch dates and blocks first-day revenue.

The hard part is not just approval. You also need processor terms, settlement timing, limits, exception handling, and daily reconciliation in place before go-live. With $10,000,000 in Year 1 customer deposits and $2,000,000 in interbank borrowing, weak controls can trigger failed transfers, holds, or account freezes.

Lock Rails Before Go-Live

Get the compliance package and business model review done first, because banking approval usually moves slower than platform buildout. Confirm the approved bank account, funding and payout rails, refund flow, and who owns daily reconciliation. One clean test is worth more than a pretty demo.

- Confirm funding, payout, and refund rails.

- Review settlement timing and cutoffs.

- Set limits for deposits and transfers.

- Write exception handling for failed items.

- Test daily reconciliation before launch day.

If those pieces are not signed off, first customers may see delayed deposits, stuck payouts, or manual fixes that slow support and create avoidable cash strain.

2

Liquidity And FX Pricing

Liquidity and FX Pricing

If the platform cannot buy and sell the launch currencies on time, it cannot open cleanly on day one. A liquidity provider must support each launch corridor and the settlement timing tied to bank rails; otherwise you get failed trades, stale quotes, or spreads that lose money. Year 1 planning calls for $500,000 in liquidity facilities, rising to $8,000,000 by Year 5, so the first corridors must fit the funded capacity.

The foreign exchange (FX) pricing engine needs live or updated rates, spread rules, customer quote expiry, corridor limits, and margin protection. Margin protection means the spread still covers fees and timing gaps. One weak price feed can turn a normal trade into a loss, so the launch plan has to prove pricing, execution, and reconciliation before customers see the first quote.

Test pricing before go-live

Before opening, verify the rate feed, order execution process, backup pricing procedure, and reconciliation to provider statements. Lock the first corridors, set quote expiry, and cap trade size by corridor. If bank settlement is slower than the pricing update cycle, tighten limits or delay that corridor. That keeps launch day from turning into manual quote fixes.

- Confirm corridor coverage first.

- Test live and fallback rates.

- Set quote expiry and limits.

- Reconcile every trade daily.

The first week should show clean quotes and matched settlements, not exception handling. If the provider statement and your ledger do not line up on day one, the team will burn time on breaks instead of serving customers. Reliable pricing is what lets the business take the first transactions without creating cash or margin surprises.

3

KYC, AML, OFAC, And Fraud Controls

KYC, AML, and OFAC Controls

KYC means confirming identity before the first FX trade. AML software watches activity, raises alerts, escalates suspicious cases, and keeps records. OFAC screening checks customers and transactions against US sanctions rules. For an online currency exchange, weak controls can trigger false approvals, frozen transfers, or a bank partner saying no before launch.

Bank reviewers will look for customer risk scoring, document checks, watchlist screening, velocity limits, a fraud review queue, and one named escalation owner. That is the day-one gate. If the controls are not live, the platform may need to open with tight transaction limits, especially when Year 1 customer deposits can reach $10,000,000.

Build the review path before the first transfer

Set the order now: verify identity, screen sanctions, score risk, then release or hold the transfer. Test the full path so a flagged user stops, not slips through, and every decision leaves an audit trail. What this hides: manual review can slow sign-ups, so opening capacity should match the size of the fraud team from day one.

- Document the KYC steps.

- Assign one escalation owner.

- Set velocity limits by risk.

- Test hold, review, and release.

- Keep records ready for bank review.

If the queue is not staffed, delays show up fast: slower onboarding, more support tickets, and more failed first transfers. Start with smaller limits, prove the controls work, and only expand once the bank partner is comfortable with the approval flow and the record trail.

4

Platform Security And Transaction Operations

Secure Transaction Flow

Platform security and transaction operations decide whether the exchange can open on time and handle real money on day one. The launch gate is a tested flow from customer signup to settlement and ledger entry, with KYC, quotes, payment confirmation, exchange records, and support handling all working together. If one step breaks, the team ends up doing manual fixes instead of serving customers.

This matters most when the first transactions hit live rails. Failed transfers, mismatched records, unresolved tickets, or weak access controls can slow opening, freeze customer activity, and trigger extra review from banking or compliance partners. With $10,000,000 in Year 1 customer deposits and $2,000,000 in interbank borrowing in the source plan, clean reconciliation is not optional; it is the control that keeps cash and records aligned.

Test the full money path

Before launch, run one transaction end to end and prove the system posts the same result in the customer view, operations log, and finance ledger. The team should verify quote expiry, payment status, exchange record storage, ticket routing, access rights, logging, and security review sign-off. One clean test is worth more than a stack of build notes.

- Map signup to settlement.

- Assign a reconciliation owner.

- Set exception rules before launch.

- Review access controls and logs.

- Prepare support for failed transfers.

If these steps are not tested before go-live, opening month volume usually creates manual work, slower replies, and delayed cash close. The practical readiness signal is simple: the first transaction should clear, record, and reconcile without a special fix from engineering or finance.

5

Corridor Strategy And First-Customer Acquisition

Corridor Focus

Start with one corridor, not a broad map. A narrow launch lets compliance, liquidity, and support stay in control on day one, which matters because the source plan already assumes $10,000,000 in Year 1 customer deposits and $300,000 in FX hedging credit. If the corridor is too wide, quotes slip, onboarding slows, and bank review gets harder.

Launch marketing should match the first limit set, not chase volume. Use clear rate comparison, transparent fees, referral partners, and trust signals so customers know what they get before they fund. The ready signal is simple: one approved corridor, one customer segment, fee disclosure, support scripts, and a compliance-approved onboarding path.

Prelaunch Control List

Verify the corridor against liquidity and bank rail capacity before you spend on demand. Here’s the quick math: if support, AML review, and settlement are built for one corridor, they can handle cleaner first trades and fewer manual fixes. If you launch broad and thin, you risk stale quotes, delays, and extra exception handling.

- Pick one corridor and one segment.

- Publish fees before first ad spend.

- Approve support scripts in advance.

- Test onboarding with compliance sign-off.

- Match limits to rail and liquidity capacity.

6

Related Products

- Online Currency Exchange Porter's Five Forces Analysis

- Online Currency Exchange BCG Matrix

- Online Currency Exchange Business Model Canvas

- 7 Core KPIs to Scale Your Online Currency Exchange

- Online Currency Exchange Business Plan Template in Pre-Written Word

- Increase Online Currency Exchange Profitability: 7 Strategies

- How Much Does It Cost To Run An Online Currency Exchange Monthly?

- Online Currency Exchange Startup Costs: $5M Capital Plan

- Online Currency Exchange Financial Model Template in Excel

- How Much Online Currency Exchange Owners Make With $38K Monthly Fixed Costs

- How to Write an Online Currency Exchange Business Plan

- Online Currency Exchange Marketing Mix

- Online Currency Exchange Marketing Plan

- Online Currency Exchange Business Proposal

- Online Currency Exchange PESTEL Analysis

- Online Currency Exchange Pitch Deck Example Editable PPTX

- Online Currency Exchange Business SWOT Analysis

- Online Currency Exchange Value Proposition Canvas

Frequently Asked Questions

Start by defining the currency corridors, customer type, and transaction flow Then form the entity, assess FinCEN MSB registration, review state money transmitter licensing, and line up bank, payment, and liquidity partners The planning case assumes $10,000,000 in Year 1 customer deposits, $5,000,000 in regulatory capital, and $500,000 in liquidity facilities