Online Currency Exchange Startup Costs: $5M Capital Plan

Based on the researched assumptions, the cost to start an online currency exchange should be planned as a funding stack, not one setup bill The model includes at least $36,000 per month in listed fixed overhead from Month 1, plus $5,000,000 of Year 1 regulatory capital and $10,000,000 of Year 1 customer deposits as separate balance-sheet needs It also shows Year 1 credit and liquidity facilities totaling $2,500,000, including trade finance, working capital, bridge funding, hedging credit, and liquidity facilities These are planning assumptions, not vendor quotes, and total funding need can exceed startup expenses because liquidity, reserves, compliance runway, and support coverage sit outside simple CAPEX

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only for an online currency exchange, not pre-opening expense or working capital.

Limits Covers capitalized startup assets only. Excludes customer deposits, payroll runway, debt service, working capital, marketing burn, transaction reserves, licensing renewals, and Month 1 fixed overhead.

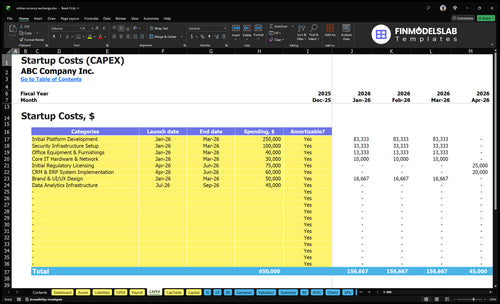

What should the CAPEX tab show?

This screenshot shows startup costs and CAPEX in the Online Currency Exchange Financial Model Template. Check categories, timing, costs, and depreciation or amortization, then review assumptions.

Key screenshot highlights

- Month 1 to 60 model period

- $36k monthly overhead

- $5M regulatory capital

What hidden costs should an online currency exchange budget include?

If you’re budgeting an Online Currency Exchange, the hidden costs are cash and risk, not just software and setup; see How Much Does The Owner Of Online Currency Exchange Make? for the revenue side, but Year 1 still needs $500,000 working capital, $500,000 liquidity facilities, $300,000 FX hedging credit, and $200,000 short-term bridge funding. $10,000,000 in customer deposits and $5,000,000 in regulatory capital sit on the balance sheet, so they are requirements, not normal startup expense.

Underfund support, compliance, or reconciliation, and churn, fraud, and regulatory risk climb fast.

Cash needs

- $500,000 working capital

- $500,000 liquidity facilities

- $300,000 FX hedging credit

- $200,000 bridge funding

Risk costs

- Reserve for payment holds and chargebacks

- Cover fraud losses and bank minimums

- Pay for compliance monitoring and support

- Plan for delayed revenue ramp and reconciliation

How should founders build an online currency exchange financial model?

Build the Online Currency Exchange model around transaction volume, currency spread revenue, payment fees, compliance costs, funding costs, liquidity needs, launch timing, and support staffing, then run it from Month 1 to Month 60. For Year 1, use 60% liquidity facility cost, 90% working capital cost, 85% trade finance cost, and 100% short-term bridge cost; also show earning assets like $5,000,000 in short-term government bonds at 45% and $3,000,000 in money market funds at 48%.

Operating drivers

- Track monthly transaction volume.

- Split spread and fee revenue.

- Include compliance and support staff.

- Map launch timing by month.

Funding plan

- Apply 60% liquidity cost.

- Apply 90% working capital cost.

- Apply 85% trade finance cost.

- Apply 100% bridge cost.

How much money do you need to start an online currency exchange?

You need far more than a website: for an Online Currency Exchange, the model shows $5,000,000 in Year 1 regulatory capital, $10,000,000 in customer deposits, $2,500,000 in credit and liquidity facilities, and at least $36,000/month fixed overhead; tie that cash plan to What Is The Primary Goal Of Your Online Currency Exchange Business?. Customer deposits and liquidity facilities are not startup expenses, but they still shape the launch plan because setup, reserves, operating runway, support coverage, and delayed volume ramp all need cash.

Core funding items

- $5,000,000 Year 1 regulatory capital

- $432,000 annual fixed overhead

- Compliance setup and monitoring

- Platform build and security

Balance sheet needs

- $10,000,000 Year 1 customer deposits

- $2,500,000 credit and liquidity facilities

- Payment rails and banking access

- Runway for slow early volume

Calculate Fuding Needs

Startup Cost Summary Table

Startup cost ranges for platform build, compliance setup, and excluded working capital needs for an online currency exchange.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Initial Platform Development | $250,000 | Product build, integrations, and launch scope | Yes |

| Security Infrastructure Setup | $100,000 | Cybersecurity, AML, and KYC controls | Yes |

| Initial Regulatory Licensing | $75,000 | Licensing, filings, and approvals | Yes |

| CRM & ERP System Implementation | $60,000 | Operations systems and payment workflow setup | Yes |

| Brand & UI/UX Design | $50,000 | Launch design, onboarding flow, and customer trust | Yes |

| Working Capital Reserve | $1,500,000 | Settlement float, regulatory capital, and liquidity needs | No |

Online Currency Exchange Core Five Startup Costs

Regulatory Licensing and Legal Setup Startup Expense

Setup Cost

For an online currency exchange, legal setup starts with entity formation, Financial Crimes Enforcement Network (FinCEN) money services business (MSB) registration, and state money transmitter analysis. The model sets $5,000/month for regulatory and compliance fees plus $2,500/month legal retainer from Month 1 to 60, or $90,000 a year before state filings, bonds, audits, or outside counsel.

Cost Drivers

This is not one fixed license fee. US cost depends on how many states you touch, whether each state needs an application, the surety bond quote, policy drafting, board approvals, and pre-launch legal review. Build the budget from filing fees, counsel hours, and months of coverage; a 60-month plan equals $450,000 on the baseline retainer model.

- State count changes filing work

- Bond quotes vary by state

- Counsel hours rise with scope

Keep It Tight

Keep the first pass tight: form the entity, finish MSB registration, map every state before filing, and use one counsel stream for policies and board materials. Don’t guess on bonds or skip review; weak paperwork slows banking and can force rework. One line item can't cover every state, so update the budget as licensing scope expands.

- File after state mapping

- Reuse one policy package

- Refresh the budget often

Plan for Spikes

State filings, bond premiums, audits, and outside counsel can swing the spend fast, so hold a contingency outside the baseline. The $90,000 annual planning number is the floor, not the ceiling, and it excludes jurisdiction-specific spikes. For launch readiness, pay for clean approvals before volume starts.

Platform Development and Technology Build Startup Expense

Build scope

The platform budget covers the web app, mobile experience if needed, rate engine, user accounts, transaction flows, admin dashboard, API architecture, reconciliation, customer alerts, cloud setup, testing, and release controls. The source model sets $15,000 a month for hosting and maintenance plus $3,000 for software subscriptions, so the recurring tech run rate starts at $18,000 a month.

Base budget

Here’s the quick math: $18,000 per month times 12 months equals $216,000 a year. That baseline is for listed technology operating costs, not one-time build work. To estimate the true startup load, add the months of coverage, cloud usage, and any extra release or support hours needed before launch.

- Use monthly run rate first

- Add launch-month support hours

- Watch cloud and testing scope

Build path

A custom build costs more because you pay for each feature and integration. A white-label path lowers upfront build work but limits control. A phased MVP keeps spend tighter by launching the rate engine, accounts, and transaction flow first, then adding mobile, alerts, and admin depth after real usage starts.

- Ship the core flow first

- Delay nonessential mobile features

- Avoid duplicate admin tools

Release control

Testing and release controls are not optional in currency conversion. Bugs in pricing, reconciliation, or notifications can create failed transfers and support load fast, so budget for pre-launch checks, rollback steps, and monitoring from day one. The goal is simple: protect live transactions before volume grows.

AML, KYC, Fraud Prevention, and Compliance Operations Startup Expense

AML and KYC Base

AML means anti-money laundering controls, and KYC means know-your-customer identity checks. For an online currency exchange, the baseline Month 1 cost is $5,000 in regulatory and compliance fees plus $3,000 in software subscriptions, or $8,000 total before staff review time and case handling.

What It Covers

This budget covers identity verification, sanctions screening, transaction monitoring, fraud rules, documentation, suspicious activity workflows, exception queues, audit prep, and staff review time. If both monthly lines stay flat, the run rate is $96,000 a year. That is an operating cost, but it also starts with setup work before launch.

- Verify users before funding

- Screen names against sanctions

- Review exceptions every day

How To Keep It Lean

Start with the controls that banks and regulators expect first, then add automation where alerts are noisy. The goal is fewer false positives, faster review, and cleaner audit trails. Do not cut sanctions screening or case notes to save a few thousand dollars; weak process usually costs more in manual work later.

- Use one clear review queue

- Keep rules simple at launch

- Train staff before volume rises

Why This Cost Matters

Weak controls can trigger fraud losses, payment reserves, and slower banking approval. For a currency exchange, that means more rejected activity, more manual follow-up, and more friction with partners. Spend early on clean documentation and review workflows so the platform looks bank-ready, not risky.

Payment Rails, Banking Relationships, and Integration Startup Expense

Rails and setup

Bank partner onboarding, ACH, card, wire, and liquidity provider integrations sit here. The build is separate from transaction fees, customer balances, and reserve balances. For Year 1 planning, carry $500,000 liquidity, $500,000 working capital, $300,000 FX hedging credit, and $1,000,000 trade finance as funding context.

Budget inputs

Estimate this cost with partner quotes, integration scope, and months of support. Include bank onboarding, ACH, card, and wire links; settlement workflows; reconciliation tools; reserve setup; processor due diligence; and exception handling. The budget should cover technical build work only, not cash held for customers or reserves.

- Quote each rail separately

- Map each workflow step

- Keep balances off-build

Cut the burn

Start with the rails you need now, then phase the rest. Don’t mix fee forecasts with build cost. On funding, 60% interest on $500,000 liquidity equals $300,000 in Year 1, and 90% on $500,000 working capital equals $450,000. That operating drag can outrun the build fast.

- Phase noncritical integrations

- Track fees apart from build

- Watch interest burn monthly

Treasury context

Treat $300,000 FX hedging credit and $1,000,000 trade finance as balance-sheet support, not setup cost. They affect how much volume you can clear and how much cash you must hold for settlement, but they do not change the software budget. This line belongs in treasury and operating planning.

Cybersecurity, Insurance, and Launch Readiness Startup Expense

Risk shield

Before launch, spend on penetration testing, security audits, encryption, cloud security, access controls, incident response planning, and go-live readiness checks. For a platform holding $10,000,000 in Year 1 customer deposits and $5,000,000 in regulatory capital, this is risk control, not IT polish.

Insurance cost

The model includes $1,500 per month or $18,000 per year in insurance premiums. That budget should cover cyber liability and errors and omissions coverage, since security failures can lead to fraud losses, chargebacks, downtime, and banking partner concerns. Price it by policy limits, scope, and launch date.

Go-live check

Use a launch readiness review to verify controls, incident steps, and owner sign-offs before go-live. Here’s the quick math: if annual premiums are $18,000, then each month of delay adds $1,500 in insurance cost before launch. The bigger cost is a weak control gap at the moment funds start moving.

Control plan

Do not treat this as routine post-launch maintenance. The budget should map to pre-launch risk reduction, with launch support, vendor quotes for testing and review scope, policy limits for insurance, and board approval for the control plan. If onboarding or review drags, the launch date slips and the bank partner may ask for more proof.

Compare 3 Startup Cost Scenarios

Scenario table

Costs rise fast as you add states, rails, compliance, and liquidity. Lean, Base, and Full show the gap between a narrow pilot and a broader regulated rollout.

| Scenario | Lean LaunchPilot ready | Base LaunchControlled launch | Full LaunchMulti-state scale |

|---|---|---|---|

| Launch model | Start with a pilot in a few states, limited rails, and low launch volume. | Launch with stronger compliance, bank integrations, admin workflows, and support coverage. | Build for broader state coverage, deeper custom software, more security review, and more rails. |

| Typical setup | Keep staffing tight, use the minimum Month 1 overhead near $36,000, and defer custom features. | Plan around the Month 1 overhead plus the Year 1 regulatory capital, customer deposits, and credit needs tied to a controlled rollout. | Assume heavier build work and larger liquidity planning, including the Year 1 $5,000,000 regulatory capital anchor and $2,500,000 in credit and liquidity facilities. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $500,000 - $1,000,000Pilot band | $1,500,000 - $3,000,000Control band | $4,000,000 - $7,500,000Scale band |

| Best fit | Best for a founder-led pilot that wants to prove demand before widening coverage. | Best for teams ready to serve real users with tighter process control and reporting. | Best for multi-state scale plans that need more control, more funding, and more operating cushion. |

Planning note: These scenario ranges are researched planning assumptions, not exact quotes, and they should be used as launch-planning bands rather than fixed bids.

Related Products

- Online Currency Exchange Porter's Five Forces Analysis

- Online Currency Exchange BCG Matrix

- Online Currency Exchange Business Model Canvas

- 7 Core KPIs to Scale Your Online Currency Exchange

- Online Currency Exchange Business Plan Template in Pre-Written Word

- Increase Online Currency Exchange Profitability: 7 Strategies

- How Much Does It Cost To Run An Online Currency Exchange Monthly?

- Online Currency Exchange Financial Model Template in Excel

- How Much Online Currency Exchange Owners Make With $38K Monthly Fixed Costs

- How To Open An Online Currency Exchange With $10M Deposits

- How to Write an Online Currency Exchange Business Plan

- Online Currency Exchange Marketing Mix

- Online Currency Exchange Marketing Plan

- Online Currency Exchange Business Proposal

- Online Currency Exchange PESTEL Analysis

- Online Currency Exchange Pitch Deck Example Editable PPTX

- Online Currency Exchange Business SWOT Analysis

- Online Currency Exchange Value Proposition Canvas

Frequently Asked Questions

The researched model points to a funding plan, not one simple startup bill Listed Month 1 fixed overhead is at least $36,000, or $432,000 annualized Separate balance-sheet needs include $5,000,000 in Year 1 regulatory capital and $10,000,000 in Year 1 customer deposits, plus $2,500,000 in credit and liquidity facilities