How Much Does A CRO Business Owner Make? $160K Pay Plus Upside

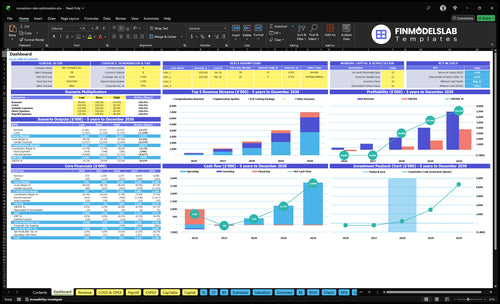

A CRO business owner can model $160,000 in annual pre-tax pay if the business funds the CEO / Lead CRO Consultant role In these researched assumptions, EBITDA is negative in Year 1 at -$244,000, near flat in Year 2 at -$4,000, then rises to $599,000 in Year 3, $1720 million in Year 4, and $3777 million in Year 5 Breakeven lands in Month 19, with payback in Month 35 and a $559,000 minimum cash point in Month 20 Any extra owner draw should come after operating expenses and reserves, not from top-line revenue

Owner income$160kNet margin89%–91.5%Revenue for target pay$180kBusiness difficultyHard

Want the six CRO income drivers that matter most?

1

Retainer Pricing

$1.8K-$9K

Higher package fees lift revenue per client fast, from $1,800-$5,400 in Year 1 to $2,800-$9,000 in Year 5.

2

Client Capacity

15-45 hrs

More billable hours per package let you serve more work per account without adding clients one for one.

3

Labor Efficiency

$385K-$1.09M

Delivery payroll is the big swing cost, so tighter staffing and faster execution protect owner take-home.

4

Retention Length

19-35 mo

Break-even in Month 19 and payback in Month 35 mean longer contracts keep cash flowing after onboarding costs.

5

Close Rate

$1.2K-$1.5K

Lower CAC improves margin before delivery starts, and every easier win leaves more gross profit in the business.

6

Owner Leverage

$160K-$3.8M

The $160K owner role and the EBITDA ramp from Year 1 to Year 5 show how delegation turns effort into profit.

Want to test your CRO owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the CRO model?

This planning model, not a promise, shows revenue, margin, costs, reserves, and owner take-home; core tabs cover dashboard, income outputs, assumptions, revenue build, staffing, software costs, marketing, reserves, scenarios, and owner pay. Open the Conversion Rate Optimization (CRO) Financial Model Template.

Owner-income model highlights

EBITDA: -$244k to $3.777M

Breakeven Month 19

Payback Month 35

Min cash $559k

Owner role $160k

Retainer and pricing tables

Payroll, overhead, capex

Can a CRO business owner make more by hiring a team?

Yes — but only if pricing, retention, and sales consistency grow faster than payroll and management overhead. In a Conversion Rate Optimization (CRO) business, an owner-operator stays lean, while a team can add retainer capacity; here payroll rises from $385,000 in Year 1 to about $1.09 million in Year 5. The math works only after volume catches up: EBITDA turns positive after breakeven in Month 19 and reaches $599,000 in Year 3.

When hiring helps

Owner-operator keeps margin high.

Contractors add delivery capacity.

Team supports larger retainers.

Volume must outrun payroll.

What can go wrong

QA risk rises with handoffs.

Recruiting adds real cost.

Meetings eat billable time.

Utilization pressure hits margins.

How much can a solo CRO consultant make?

A solo Conversion Rate Optimization (CRO) consultant can target a $160,000 owner-operator role in this model, but that pay is mostly labor income, not scalable agency profit. Before adding clients, use What Is The Current Engagement Level Of Visitors On Your Conversion Rate Optimization Business? to check whether traffic quality can support paid testing work, because solo capacity tops out at 30, 20, and 15 billable hours per Year 1 package.

Year 1 pricing

$5,400 comprehensive retainer

$3,200 optimization sprint

$1,800 A/B testing package

Implied rates: $120–$180/hour

Solo capacity cap

30 hours for full retainers

20 hours for sprints

15 hours for testing packages

Owner handles sales, testing, reporting, clients

What affects CRO agency profit margins?

For a Conversion Rate Optimization (CRO) agency, margins get squeezed fast because tool COGS alone can hit 110% of sales before labor, marketing, or overhead. If you’re pricing the business, see How Much Does It Cost To Launch Your Conversion Rate Optimization Business? because $5,800 in monthly fixed overhead and $385,000 in Year 1 payroll already put heavy pressure on take-home. The biggest drag is rework and client-facing labor, since extra analyst, developer, copy, QA, or stakeholder time cuts owner margin.

Main margin drains

70% revenue to software licenses

40% revenue to data tools

110% tool COGS total

90% sales commissions and bonuses

Cost pressure points

80% direct marketing cost load

$5,800 fixed overhead each month

$385,000 Year 1 payroll start

Owner take-home falls with rework

Key Takeaways

Price must match hours, testing depth, and reporting load.

More clients help revenue but strain specialist capacity.

Margin depends on labor efficiency and fewer rework cycles.

Retention and lead quality protect payback and growth.

Scenario objective: Compare lean, base, and high CRO owner income scenarios using the provided cost and growth assumptions

Owner income scenarios

Owner income shifts with retainer mix, billable hours, and team build. Low stays cash-tight, base matches the modeled $160,000 pay, and high adds scale with stronger recurring work.

Three planning cases for founder pay and upside.

Scenario

LowLow case

BaseBase case

HighHigh case

Launch model

Owner draws stay light and the business remains below breakeven.

Owner pay follows the modeled case as repeat work builds.

Owner income rises fastest when the team scales and recurring work grows.

Typical setup

Year 1 EBITDA is about -$244,000, so the founder stays hands-on and keeps reserves tight.

The model uses the stated $160,000 CEO pay, Month 19 breakeven, Month 35 payback, and Year 3 EBITDA of $599,000.

By Year 4 and Year 5, EBITDA reaches about $1.72 million and $3.777 million before taxes, depreciation, debt, and discretionary distributions.

Cost drivers

Retainer mix

billable hours

sales commissions

ad spend

staffing pace

Modeled $160k owner pay

Month 19 breakeven

Month 35 payback

Year 3 EBITDA $599k

repeat retainers

Scaled team

stronger recurring mix

Year 4 EBITDA $1.72M

Year 5 EBITDA $3.777M

retention risk

Owner income rangeBefore owner reserves

Below breakeven, limited drawsCash-tight

$160,000Modeled pay

$1.72M-$3.78M EBITDAUpside ramp

Best fit

Founders who want to stress-test a lean, founder-led model with minimal owner take-home.

Small teams that expect repeat retainers and want the base planning case.

Teams testing a cash-heavy ramp with higher payroll and retention risk.

!

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Conversion Rate Optimization (CRO) Core Six Income Drivers

Average retainer pricing

Average Retainer Pricing

Retainer price drives income when the fee matches both client value and delivery load. In Year 1, a comprehensive CRO retainer at 30 hours × $180 = $5,400 sets the floor; by Year 5, 45 hours × $200 = $9,000 lifts revenue, but only if margin holds. A stronger price helps owner pay only when added hours still leave room for profit.

Package mix matters too: optimization sprints rise from $3,200 to $4,500, and A/B testing packages move from $1,800 to $2,800. If price goes up while testing cadence, analytics depth, reporting, and stakeholder work stay flat, cash flow improves. If hours grow faster than fee, you’re just selling more labor.

Price to Match Scope

Track the inputs that set the retainer: billable hours, tests per month, reporting time, and stakeholder meetings. Use them to price each scope tier so the fee covers delivery and leaves margin for owner pay. One clean rule: price the work you actually do, not the work you hope to do.

30 hours plus light reporting = base fee

45 hours needs higher price

Charge more for deeper analytics

Charge more for more test cadence

Watch margin, not just revenue

What this estimate hides: if the team adds analyst time, QA, or extra client calls without a fee reset, gross margin shrinks fast. The safest move is to review each retainer against actual hours every month and reprice when delivery load climbs.

Client retention and contract length

Client retention and contract length

For a CRO agency, client retention is what keeps owner income steady. Replacement sales are slow and costly: CAC is $1,500 in Year 1 and still $1,200 by Year 5, with breakeven in Month 19. If contracts end before that point, the business can still be paying for acquisition and payroll before the account has fully paid back.

Longer retainers lift recurring revenue and make reporting cleaner because each client gets more test cycles, more learning, and a clearer proof trail. The risk is simple: if a client leaves before enough experiments show value, owner pay gets squeezed even when sales are strong.

Track retention past payback

Measure retention by months kept, renewal rate, and how many test cycles each client sees before renewal. Tie reporting to measurable wins, not activity. If the client cannot see clear experiment results, stakeholder buy-in drops and churn rises, which hurts cash flow and delays owner draw.

Use a contract length that covers the payback window. A simple rule: if a client is likely to exit before Month 19, the agency may still be funding the account. Keep scope tight, report often, and prove value early so the retainer survives long enough to turn into profit.

Fulfillment labor efficiency

Fulfillment labor efficiency

This driver is about who does the work, how often work gets redone, and whether delivery time is priced right. In the model, direct tools cost is 110% of revenue in Year 1 and 85% by Year 5, while payroll is the bigger lever at about $385,000 in Year 1. If analyst, developer, QA, and reporting time are underpriced, gross margin gets squeezed fast.

Gross margin improves when a senior CRO specialist, analyst, UX/UI designer, and owner strategist each stay in their lane and rework stays low. Separate direct client delivery cost from overhead and owner compensation, or the business can look healthy on paper while cash to pay the owner stays thin. Every redo cycle cuts billable output and delays take-home income.

Control rework and role mix

Track billable hours by role, rework rate, and non-billable QA. Price each client against the hours for testing, analysis, design, reporting, and meetings, then compare it to the retainer. The model’s Year 5 payroll reaches about $109 million, so small waste in delivery hours matters more than tool spend.

Use a weekly margin view by client: direct labor, tools, and redo time. If one package needs repeated test fixes, raise scope or cut service depth. One clean rule helps: if a task cannot be tied to a client deliverable, it belongs in overhead, not delivery. That keeps owner pay from getting trapped inside unpriced work.

Active client capacity

Active Client Capacity

Active client count grows monthly revenue, but it also adds delivery load. In Year 1, a comprehensive retainer takes 30 hours, an optimization sprint takes 20 hours, and an A/B testing package takes 15 hours. By Year 5, those rise to 45, 25, and 20 hours, so the same client mix can consume far more specialist and analyst time and squeeze owner pay if pricing does not rise with workload.

Here’s the quick math: 4 comprehensive retainers mean 120 hours in Year 1 and 180 hours in Year 5 before any sprints or test packages. That extra work shows up as audits, hypotheses, analytics review, reporting, and meetings. If capacity is overbooked, quality slips first, then margins, then cash flow, because the agency is busy before it is profitable.

Track Hours Before You Add Clients

Measure capacity in available specialist and analyst hours, not just client count. Track billable hours by package, time spent on audits, tests, reporting, and client meetings, plus rework time. If a package keeps creeping past the planned hour count, raise price, reduce scope, or slow sales until delivery is stable.

Use a simple rule: do not add another active client unless you can absorb the extra workload without hurting turnaround time or test quality. One clean filter is whether the team can cover the next month’s projected hours with room for reporting and review. If not, revenue can rise while owner draw stays flat.

Set monthly hours by package.

Track utilization by role.

Separate delivery hours from admin.

Watch rework and meeting creep.

Cap clients at real capacity.

Lead generation and close rate

Lead gen and close rate

For a CRO agency, lead generation and close rate set how fast billable clients replace churned ones. The model lifts annual marketing spend from $25,000 in Year 1 to $180,000 in Year 5, while CAC improves from $1,500 to $1,200. If CAC holds, that supports about 17 customers in Year 1 and about 150 in Year 5, so owner income rises only when the pipeline fills higher-value retainers.

The risk is volume without fit. Low-quality leads can close into small or short-lived accounts, which hurts cash flow because CAC payback depends on clients staying long enough to recover sales spend. Here’s the quick math: $25,000 ÷ $1,500 ≈ 17; $180,000 ÷ $1,200 = 150. More leads only help if they match comprehensive retainer work, not cheap one-off projects.

Qualify harder, not wider

Track lead source, proposal win rate, retainer size, and churn by cohort. The key input is not just lead count; it is how many leads become comprehensive retainers with enough margin to cover CAC before Month 19. If a channel fills the funnel with poor-fit prospects, cut it even if volume looks good.

Use a simple gate: qualified lead, sales call, proposal, close. Measure each step monthly and price to the work, because better close rate on the right fit improves revenue quality, cash flow, and the owner’s draw. Small fixes in targeting usually beat spending more on traffic.

Track CAC by channel.

Track close rate by package.

Track churn before payback.

Owner role and team leverage

Owner role and team leverage

If the owner does strategy, sales, analytics, and delivery, the model carries a $160,000 CEO / Lead CRO Consultant salary in every year, so early cash pay can look better than the P&L shows. The limit is capacity: one person can only sell, test, report, and manage so many client hours before quality slips and growth stalls.

When the team handles delivery, payroll rises but the owner can push more revenue through the same core process. The model’s EBITDA improves from -$244,000 in Year 1 to $3,777,000 in Year 5, which shows the payoff after fixed team costs are covered. One clean rule: if utilization falls, owner income falls fast.

Track owner hours, utilization, and margin

Measure three things every month: owner billable hours, team utilization, and EBITDA after the $160,000 owner salary. If the owner is still doing delivery, track how many client accounts can be served before response time or test quality drops. For a CRO agency, the inputs that matter most are client count, delivery hours, analyst time, and sales time.

Use a simple staffing rule: keep strategy and sales with the owner, and move repeatable testing, reporting, and QA to the team as soon as workload becomes predictable. That protects margin and makes take-home pay less tied to the owner’s own hours. If the team can absorb delivery, the business can scale; if not, revenue grows but cash stays tight.