How Much Hangover IV Treatment Owners Make at 1,015 Visits/Month

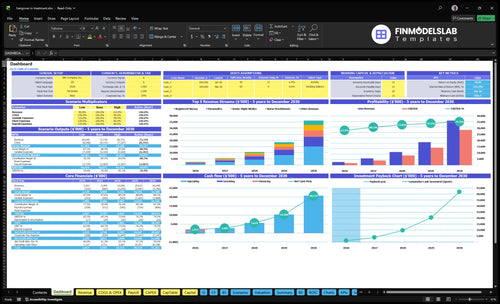

A hangover IV treatment service owner’s take-home cannot be finalized from the provided data because clinician compensation, reserves, taxes, debt service, and one telehealth cost are not provided Using the researched planning assumptions, Year 1 produces about $213,420 in monthly revenue from 1,015 treatments at a weighted average ticket near $210 After supplies, sterile logistics, merchant fees, travel stipends, and known fixed overhead, the model leaves about $148,451/month before clinician pay, reserves, taxes, and owner draw So the real owner-income question is how much of that pool survives staffing, compliance-related costs, and reinvestment

Owner income$148kNet margin64%–79%Revenue for target pay$2.56MBusiness difficultyHard

Want to see what drives owner income?

1

Treatment Volume

1.0K-11.1K/mo

This is the main revenue engine: more visits push cash left after costs and reserves.

2

Ticket Mix

$210-$270

A higher weighted ticket lifts revenue per visit without adding the same labor and travel load.

3

Clinician Capacity

28-117

The forecast staff build decides how many paid visits you can take before service bottlenecks hit.

4

Supply Costs

18.5%-22.5%

Cuts in supplies, waste, processing, and travel fees drop straight to margin.

5

Marketing Efficiency

$5.5K/mo

The fixed marketing line only helps if it fills schedules, so booking efficiency drives take-home.

6

Fixed Overhead

$18.2K+

Known fixed costs already run $16,950 a month before telehealth, so low utilization hits owner income fast.

Want to test your owner-pay number?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the forecast?

This dashboard shows revenue, margin, costs, reserves, and owner take-home; open the template. This is planning only.

Owner-income model highlights

$213,420 revenue start

$16,950 fixed costs

Owner draw stays editable

Break-even stays visible

When should a hangover IV treatment service hire clinicians?

For a Hangover IV Treatment Service, hire clinicians only when demand is already proven, your own time is maxed out, and each new clinician still adds profit after pay, supplies, travel, and oversight. In Year 1, capacity assumptions of 20% to 35% are too thin for early hiring, so it can drain cash. By Year 5, 60% to 75% utilization can support broader coverage if bookings hold, but start with dense zones, event blocks, and repeat-booking windows before widening the service radius.

Hire now

Proven demand comes first

Owner time is fully capped

Net profit still rises per visit

Dense zones beat wide coverage

Scale later

Year 1: 20% to 35% capacity

Year 5: 60% to 75% capacity

Event blocks can lift bookings

Repeat windows help fill shifts

What costs affect hangover IV treatment service profit?

For a Hangover IV Treatment Service, profit gets squeezed most by clinician pay, supplies, waste handling, card fees, and travel. Here’s the quick math: Year 1 non-labor variable costs total 225% of revenue, with 105% for infusion supplies and IV kits, 25% for biohazard waste and sterile logistics, 35% for payment processing, and 60% for practitioner travel stipends. For the full cost build, see What Is The Cost To Run Hangover IV Treatment Service? ; monthly fixed overhead is $16,950.

Big variable costs

Clinician pay drives service cost.

Supplies equal 105% of revenue.

Waste and logistics add 25%.

Payment processing takes 35%.

Fixed monthly load

Marketing: $5,500 per month.

Medical oversight: $4,500 monthly.

Dispatch rent: $3,200 monthly.

Insurance and software: $3,750 total.

Can a hangover IV treatment service support a full-time owner?

Yes, a Hangover IV Treatment Service can support a full-time owner, but only after treatment volume covers clinician payroll, fixed overhead, reserves, and local customer acquisition cost; track that with What Are The 5 KPI Metrics For Hangover IV Treatment Service?. The Year 1 model shows 1,015 treatments/month and $213,420 monthly revenue, but it also needs 28 clinicians across five roles, so staffing cost decides owner pay. Minimum non-labor break-even is about $21,871/month, or 104 treatments at $210 AOV; paying the owner $100,000/year needs at least $32,623/month before clinician payroll and reserves.

Owner Pay Math

Reach 104 treatments before non-labor break-even

Protect $32,623/month before owner salary

Fund reserves before taking full pay

Watch clinician payroll every week

What Decides It

Build repeat customers, not one-time spikes

Pack weekends with dense route volume

Keep pricing near $210 AOV

Measure local acquisition cost by zip

Key Takeaways

More visits spread fixed costs and improve margin.

Ticket size rises with add-ons and service mix.

Clinician staffing shapes both capacity and profit.

Overhead needs enough monthly volume before owner pay.

Compare lean, base, and high-demand owner-income scenarios

Owner income scenarios

Owner income scales fast as treatment volume, average price, and clinician capacity rise. The pool before clinician payroll is strongest in the high-demand case, but take-home still depends on staffing, reserves, and taxes.

Low, base, and high cases show how much income can shift as the service fills capacity.

Scenario

Low CaseLow case

Base CaseBase case

High CaseHigh case

Launch model

This is the early ramp-up income case with the lightest volume and the smallest pre-clinician pay pool.

This is the modeled operating case with proven demand and a much larger pre-clinician pay pool.

This is the stronger earnings path with dense demand and the largest pre-clinician pay pool.

Typical setup

Year 1 assumptions drive about 1,015 treatments a month at a $210 average selling price, with $213,420 revenue and a $148,451 pre-clinician-pay pool before fixed overhead and payroll.

Year 3 assumptions reach about 3,717 treatments a month at a $238 average selling price, with $882,996 revenue and a $683,266 pre-clinician-pay pool.

Year 5 assumptions reach about 11,145 treatments a month at a $270 average selling price, with $3,008,164 revenue and a $2,434,703 pre-clinician-pay pool.

Cost drivers

Treatment volume

average selling price

non-labor margin

fixed overhead

clinician payroll

Treatment volume

average selling price

capacity use

variable costs

clinician payroll

Treatment volume

premium pricing

dense routing

clinician mix

overhead leverage

Owner income rangeBefore owner reserves

$148,451Early ramp-up

$683,266Proven demand

$2,434,703Dense market upside

Best fit

Use this to stress-test the first operating year when demand is still building.

Use this as the core planning case once the service has repeat demand and steady routing.

Use this to test upside in a dense multi-clinician market with strong execution.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Hangover IV Treatment Service Core Six Income Drivers

Monthly treatment volume

Monthly Treatment Volume

Monthly treatment volume is the first income lever because every paid visit spreads fixed overhead across more revenue. Here’s the quick math: volume rises from 1,015 treatments a month in Year 1 to 11,145 in Year 5, or about 11x more visits after capacity assumptions.

Open slots are not revenue. Travel time and clinician availability cap daily capacity, and weekend spikes, events, and repeat bookings only help if the schedule stays full. Missed density hurts margin because travel stipends equal 60% of Year 1 revenue, so thin routes can crowd out owner pay fast.

Measure and Pack More Visits

Track booked visits, completed visits, and available slots by day. The key test is simple: how many paid treatments does each clinician finish after travel? One clean number matters more than a pile of leads.

Watch treatments per day

Track travel minutes per visit

Fill weekend and event blocks

Push repeat bookings fast

Compare booked vs. completed visits

If travel time keeps rising, route density is too thin. Build schedules around clusters, not one-off calls, so more of each shift turns into paid treatment volume and better cash for the owner draw.

Clinician labor model

Clinician Labor Cost

Clinician labor is the swing factor between a busy schedule and real owner pay. With 28 clinicians in Year 1 growing to 117 by Year 5, the mix of registered nurses, paramedics, nurse practitioners, senior flight medics, and lead clinicians decides how much revenue turns into contribution. Owner-operated delivery protects margin, but it also caps capacity.

Here’s the quick math: more staffed coverage means wider service hours and better reliability, but it usually lowers margin per visit. Contractor-heavy coverage can help fill spikes, yet the model only works if labor cost stays below the cash generated per treatment. Legal scope and licensing are separate from this financial model, so track them as compliance risk, not margin math.

Track Cost Per Visit

Measure labor by cost per completed treatment, not just headcount. Start with clinician count, role mix, utilization, and the share of visits covered by the owner versus contractors or staff. If open slots are not filled, labor still sits on the books, and owner draw gets squeezed. One clean rule: empty coverage does not pay rent.

Track visits per clinician shift

Track labor cost per completed visit

Track owner-covered versus paid coverage

Track hours open for service

Track no-show and idle time

If you need longer service hours, test contractor coverage first, then compare it to owner-delivered margins. The right model is the one that keeps enough capacity without letting clinician cost outrun the cash left after each treatment.

Supply cost and gross margin

Supply Cost per Treatment

Each hangover IV visit carries direct supply cost from saline, vitamins, tubing, needles, PPE, any general meds, plus waste handling and sterile logistics. In the model, Year 1 supply-related costs are 105% for infusion supplies and IV kits plus 25% for biohazard waste and sterile logistics, improving to 85% and 20% by Year 5. That line sets gross profit before overhead and owner pay.

If supply cost per treatment stays high, every booked visit leaves less cash for rent, marketing, and the owner’s draw. Expired stock and over-ordering hurt twice: they raise cash tied up in inventory and turn usable margin into write-offs. The key test is simple: does each treatment leave enough gross profit after supplies to support the rest of the month?

Track Kit Cost and Waste

Measure supply cost per completed treatment, not just total purchases. Break it into kit cost, waste handling, and sterile logistics, then compare it to treatment volume and the revenue per visit you actually collect. If one package uses more product than planned, fix the protocol fast.

Track expired items every month.

Count kits used per treatment.

Review supplier pricing quarterly.

Order to forecast, not fear.

Cut waste before you cut price. Small changes in inventory control, pack-out accuracy, and supplier terms move gross margin fast because this business sells a high-touch service with real consumable cost on every call.

Customer acquisition efficiency

Customer Acquisition Efficiency

For this service, customer acquisition efficiency is the gap between the $5,500/month marketing bill and the cash each booked IV visit brings in. If ads, hotel referrals, event leads, local search, and reviews do not turn into enough paid bookings, revenue can rise while owner take-home stays thin.

The key check is cost per booked visit, not clicks or calls. Track booked visits, conversion rate, repeat rate, and revenue per customer. If repeat guests and event bookings are weak, every new visit has to carry more of the marketing load, and that pushes profit down fast.

Measure Cost Per Booking

Measure each channel by booked visits, then divide spend by bookings. That means paid ads, hotel relationships, bachelor and bachelorette events, local search, reviews, and repeat customers all need separate tracking. One channel can look busy and still lose money if it brings low-value or one-time bookings.

Use a simple funnel: lead → booked visit → repeat visit. If conversion drops or repeat rate slips, raise follow-up, tighten targeting, or shift spend to channels with better return. The goal is not more traffic; it’s more paid treatments per dollar of marketing.

Booked visits per channel

Conversion rate from inquiry

Repeat rate by customer type

Revenue per customer

Average ticket and add-ons

Average Ticket

Revenue here lives or dies on weighted AOV, the blended average price per visit. It’s about $210 in Year 1 and $270 in Year 5, based on a mix of $180 to $550 services. With 1,015 visits, that lift adds about $60,900 a month before any cost change, so higher ticket size can directly boost owner draw.

The ticket includes the base IV, vitamin add-ons, group bookings, event packages, and travel fees. But upsells only help if they fit local competition, conversion rate, and medical protocols. One clean rule: if the add-on is not clinically right or does not cover extra labor and supply use, it should not be sold.

Price and Add-On Control

Track realized price per booked visit, not just posted menu price. Split out base treatment, add-ons, travel fees, and group pricing, then test changes in small steps so conversion does not fall faster than ticket size rises.

Measure add-on attach rate by clinician

Compare conversion by price point

Log protocol-based upsell refusals

Recover travel costs on every route

Review revenue per booked appointment

Fixed overhead and utilization

Fixed overhead load

Monthly fixed overhead is $16,950 before the owner takes home pay. That includes $4,500 for medical director oversight, $3,200 for dispatch office rent, $2,800 for malpractice and general liability insurance, $5,500 for marketing, and $950 for HIPAA-compliant software. HIPAA means the Health Insurance Portability and Accountability Act, so data handling adds a real cost.

This load creates a hard break-even gate: monthly visits × contribution per visit must clear $16,950 before draws make sense. Marketing is about 32% of fixed overhead, so weak booking efficiency hits cash fast. The telehealth platform cost is listed but not priced, so true fixed overhead may be higher than shown.

Track break-even utilization

Utilization means paid visits divided by available service slots. Track that weekly, because empty slots do not help cover fixed costs. If clinician time, dispatch, or travel leaves gaps, the same $16,950 gets spread over fewer visits, and owner income gets pushed out. Here’s the quick math: the lower the visit count, the higher the fixed cost per treatment.

Paid visits per month

Contribution per visit

Open slots by daypart

Set a monthly break-even visit target from those inputs before you plan any owner draw. Then watch whether marketing spend, booked visits, and clinician coverage hold that target. If bookings dip while fixed overhead stays flat, cash gets tight even if revenue looks active on busy weekends.