How Much Life Coaching Business Owners Make: $120K Base Pay

A life coaching business owner can model $120,000 in annual founder pay before owner taxes, with extra take-home only if the practice produces profit after expenses and reserves In the first year, the model uses $24,000 of marketing spend, $400 CAC, 45 billable hours per active customer per month, and a weighted rate near $169 per hour At a 60-active-client run rate, revenue is about $546,750 per year after 265% variable costs, $65,400 fixed overhead, and $162,500 wages, operating profit is about $174,000 before taxes, capex, debt, and reserves These are researched planning assumptions, not guaranteed salary or tax guidance

Owner income$18.0kNet margin40%Revenue for target pay$21.0kBusiness difficultyHard

Want to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see how owner income is modeled?

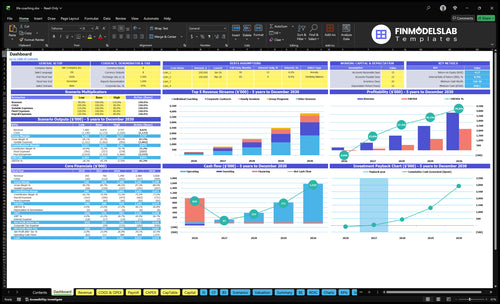

This dashboard shows revenue, pricing, CAC, expenses, reserves, and owner income. Open the Life Coaching Financial Model Template to plan, not prove income.

Owner-income model highlights

Owner take-home output

Revenue and margin view

Assumptions, CAC, and costs

Scenarios, staffing, capex

Tests each offer type

How do you scale a life coaching business income?

Scale Life Coaching income by raising revenue per coaching hour and shifting the client mix away from pure one-on-one work. In this model, group programs grow from 15% of Year 1 customer mix to 30% by Year 5, and corporate contracts rise from 10% to 22%, with hourly rates moving from $300 in Year 1 to $420 in Year 5. One-on-one coaching stays high-touch but capped by hours, while adding contractor or employee coaches expands capacity but also adds wages, commissions, training, and quality risk.

Raise revenue per hour

Group programs lift reach.

Corporate contracts pay more per hour.

One-on-one stays premium but limited.

$300 to $420 shows the rate gap.

Add capacity carefully

Contractor coaches add billable hours.

Employee coaches add fixed wage cost.

Training protects quality, but takes time.

Quality risk rises as headcount grows.

What life coaching business expenses reduce owner income?

Life Coaching owner income gets squeezed by $5,450 in monthly fixed costs before any sales costs hit, and year 1 variable costs can take another 58% of revenue. Startup cash needs are separate: $42,500 upfront for office setup, computer equipment, website development, and certifications. For the setup side, see How Much Does It Cost To Open And Launch Your Life Coaching Business?

Yes, Life Coaching can be profitable, but only after paid client volume covers $120,000/year founder pay, $65,400/year fixed overhead, and 26.5% variable costs; track the core KPI in What Is The Most Important Metric To Measure The Success Of Your Life Coaching Business?. At a weighted Year 1 rate of $168.75/hour, break-even is about $252,245/year, or 1,495 billable hours/year.

Profit Drivers

Grow paid client volume

Protect $168.75/hour average rate

Improve client retention

Control 26.5% variable costs

Break-Even Math

Fixed overhead: $65,400/year

Founder pay: $120,000/year

Required revenue: $252,245/year

Monthly target: 125 billable hours

Life Coaching Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

What changes owner income most?

1

Client Volume

60-288

At Year 1 CAC, the $24K marketing budget buys about 60 clients, and by Year 5 it can buy about 288, so volume drives take-home fast.

2

Pricing Mix

$75-$420

Shifting more hours into higher-rate work lifts the weighted hourly rate and raises revenue per billable hour.

3

Recurring Revenue

4.5-6.5h

More monthly hours per active customer lift recurring revenue and make each acquired client worth more.

4

Delivery Mix

265%-205%

The mix of one-on-one, group, and corporate work changes variable cost load, so margin can move a lot.

5

CAC

$400->$250

Lower CAC lets the same marketing budget buy more clients and shortens payback.

6

Overhead Load

$5.45K/mo

Fixed overhead plus the $120,000 founder salary set the break-even floor, so lean support costs protect profit.

Life Coaching Core Six Income Drivers

Active Client Volume

Active Client Volume

Active clients set the revenue ceiling because each one adds billable hours and monthly cash. With a $24,000 Year 1 marketing budget and $400 CAC, the model supports about 60 acquired customers if CAC holds. At about $759/month per active customer, that is roughly $45,540/month before churn, no-shows, or unpaid admin time.

The risk is capacity, not just demand. More active clients can raise owner income, but only if scheduling stays tight, outcomes stay strong, and retention holds. If sessions slip or clients drop early, revenue falls fast and referral flow weakens, so take-home pay depends on how many clients stay active, not just how many leads are bought.

Track Capacity First

Track active clients, billable hours per client, CAC, and monthly churn every month. Forecast revenue as active clients × $759, then compare that load to the coach’s real calendar. If client count rises faster than delivery capacity, cash can improve short term, but margin and client results often slip next.

Cap clients by usable weekly hours.

Watch no-shows and renewals.

Compare CAC to monthly client revenue.

1

Pricing And Package Structure

Pricing and Package Mix

Pricing changes income fast because the same coach time can sell at very different rates. In Year 1, the model uses $150/hour for individual coaching, $200/hour for hourly sessions, $75/hour for group programs, and $300/hour for corporate contracts, which creates a weighted rate near $168.75/hour.

By Year 5, the weighted rate reaches about $237.30/hour as rates and mix improve. That raises revenue per client and helps owner pay, but only if the offer fits the niche, the proof is strong, and the schedule stays full. No single price works for every audience or service.

Track Rate Mix, Not Just Hours

Build the forecast from billable hours, client mix, and price by offer. Watch how much revenue comes from individual, hourly, group, and corporate work each month, then compare the realized rate to the $168.75 to $237.30 range.

Test package bundles and price lifts before adding more leads. If lower-priced group work fills the calendar but cuts margin, take-home income drops even when sales rise. The key control is simple: keep the best-paying mix you can sell without hurting outcomes or renewals.

2

Retention And Recurring Revenue

Retention Raises Recurring Coaching Revenue

Retention includes renewals, longer programs, and repeat sessions. Track active clients, renewal rate, average billable hours per client, and monthly revenue per active client. If average billable hours rise from 45 in Year 1 to 65 in Year 5, revenue tied to each active client rises 44% before new lead spend. That gives the owner more recurring income and less monthly pressure to refill the pipeline.

The cash-flow win is simple: $400 CAC spread over 45 hours is $8.89 per billable hour, but over 65 hours it drops to $6.15. Better retention makes CAC easier to live with, but it has to come from fit, outcomes, and clear value, not pressure-based selling. Otherwise churn just pushes the same cost back onto the next sale.

Track Renewals, Not Just New Sales

Use cohort tracking: start date, renewal rate, program length, billable hours, and revenue per active customer. The key question is whether one client turns into a second or third package, not just a first sale. When clients stay longer, recurring revenue grows faster than fixed overhead, so more of each month’s cash can cover pay, reserves, and reinvestment.

Track active clients by month

Measure renewal rate by cohort

Watch billable hours per client

Compare CAC to client revenue

If retention slips, revenue gets lumpy and the business leans too hard on paid leads. If it improves, the owner can buy fewer leads each month and keep more profit as take-home pay. That is the real upside of recurring coaching revenue: steadier cash, better margin on each client, and less pressure on sales every month.

3

Delivery Format

Delivery Format Drives Capacity

One-on-one coaching is capped by calendar hours, so revenue grows only as many sessions as the owner can deliver. Group programs and corporate contracts can lift revenue per delivery hour, but they also need better curriculum, facilitation, and client support to protect margins.

In the model, group programs rise from 15% of customer mix in Year 1 to 30% in Year 5, while corporate contracts rise from 10% to 22%. That shift can raise take-home income, but only if sales can fill the seats and service quality stays tight. If delivery breaks, refunds, churn, and rework eat profit fast.

Track Mix, Hours, and Margin

Measure billable hours, revenue per delivery hour, and client mix each month. Here’s the quick math: if more revenue comes from group and corporate work, the owner can earn more without adding as many 1:1 hours, but only when pricing covers prep time, follow-up, and admin.

Track these inputs before you scale: 1:1 share, group share, corporate share, session fill rate, and time spent on prep. If group delivery needs extra support, add that cost into the price. Otherwise the schedule looks fuller, but owner pay gets squeezed.

Watch calendar capacity weekly

Price prep time into group offers

Test corporate sales close rates

Track refunds, no-shows, and rework

4

Client Acquisition Cost

Client Acquisition Cost

CAC is the marketing spend needed to win one paying client. In this model, CAC falls from $400 in Year 1 to $250 in Year 5, while annual marketing budget rises from $24,000 to $72,000. That helps take-home income only if each new client turns into enough billable sessions and renewals.

Here’s the quick math: $24,000 / $400 = 60 clients in Year 1, and $72,000 / $250 = 288 clients in Year 5. One-liner: if CAC rises faster than client value, owner pay shrinks fast. Paid ads can fill the pipeline, but they do not guarantee profitable growth.

Track CAC by Channel

Measure marketing spend, new paying clients, and monthly revenue per active client so you can see which source pays back. Referrals, content, partnerships, and better conversion rates are the real levers here; ads alone are not a safe growth plan.

Spend ÷ new clients = CAC

Watch CAC by channel

Compare to client revenue

Cut weak channels fast

If a channel brings leads but not paid clients, it hurts cash flow and delays profit. Keep marketing tied to booked sessions, renewals, and repeat packages so growth supports owner draw instead of draining it.

5

Overhead And Support Costs

Overhead And Support Costs

Overhead is the money that keeps coaching running before you pay yourself. The model shows $5,450/month in fixed operating expenses before payroll, plus $800 for tech and software, $400 for insurance, and $500 for accounting. That’s a $1,700 support stack in the named lines alone, and it still doesn’t include payroll or owner draw.

The cash trap is simple: Year 1 variable costs are 265% of revenue, and reserves and reinvestment come before owner pay. So profit on paper is not spendable cash. If overhead stays high while client volume is still thin, the owner can look busy and still take home very little.

Track Burn Before Draw

Measure fixed burn, variable cost ratio, and monthly cash left after reserves. The key inputs are revenue, client count, software, insurance, accounting, payroll, and any reinvestment plan. One clean test: if monthly overhead plus variable costs outrun collections, owner pay has to wait.

Keep a simple cash order: collect revenue, cover overhead, fund reserves, then set owner draw. Watch the gap between gross income and spendable cash, not just profit. If software, admin, and professional fees keep rising without higher active clients or retention, take-home income will lag even when sales look decent.

Track overhead monthly by category.

Separate reserves from owner pay.

Review software, insurance, and accounting spend.

Test revenue against the 265% variable-cost load.

6

Life Coaching Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Compare low, base, and high owner-income scenarios

Planning cases

Owner income shifts with client mix, billable hours, and staff load. More group and corporate work can lift margin; a slow ramp keeps founder pay under pressure.

Compare downside, base, and upside owner pay cases.

Scenario

Low CaseDownside case

Base CaseBase case

High CaseUpside case

Launch model

This case models a slower ramp where founder pay outruns cash early on.

This case models the main operating plan, where revenue grows enough to support the founder role but cash stays watched.

This case models a stronger mix where pricing, volume, and margin push owner income higher.

Typical setup

The business stays heavy on individual coaching and hourly sessions, with limited client volume, thin reserves, and $120,000 founder pay under strain.

It assumes about 60 active clients, about $45,563 monthly revenue, 26.5% variable costs, $5,450 fixed overhead, and $162,500 Year 1 wages.

The mix shifts toward group programs and corporate contracts, CAC falls to $250, billable hours rise to 6.5 per active customer, and cash reserves build faster.

Cost drivers

slow client ramp

lower billable hours

founder pay pressure

fixed overhead

weaker reserves

60 active clients

$45,563 monthly revenue

26.5% variable costs

$5,450 fixed overhead

$162,500 Year 1 wages

stronger pricing

more group and corporate mix

lower CAC

higher billable hours

faster reserve build

Owner income rangeBefore owner reserves

Founder pay under strainCash strain

Founder pay partly coveredSteady base

Above founder salaryUpside room

Best fit

Use this to test how long reserves hold if sales lag and pay stays fixed.

Use this for the core plan and to check if the model can carry the founder role.

Use this to test upside if premium pricing and higher-value contracts land faster than plan.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Part-time income depends on active clients, rates, and fixed costs In this model, each Year 1 active customer produces about $759 per month from 45 billable hours at a $16875 weighted hourly rate If you keep overhead below the modeled $5,450 monthly fixed cost, part-time take-home can improve faster

Income stabilizes when recurring clients cover fixed overhead, marketing, and owner pay The model starts with $24,000 annual marketing, $400 CAC, and 60 acquired customers if CAC holds Stability usually depends less on the first sale and more on retention, repeat purchases, and whether client acquisition stays below revenue per client

No, but employees change the math The model includes a $120,000 founder salary and adds a senior coach at 05 FTE in Year 1, equal to $42,500 of annual wage cost Extra coaches can raise capacity, but wages, commissions, training, and quality control reduce profit before owner distributions

Client volume, payment timing, CAC, and fixed overhead drive cash flow Year 1 fixed expenses are $5,450 per month, and variable costs equal 265% of revenue Startup items such as $15,000 office setup, $12,000 website development, and $7,500 certifications also pull cash before revenue is steady

Raise take-home by improving revenue per active client without bloating overhead In the model, billable hours per active customer grow from 45 to 65, CAC falls from $400 to $250, and higher-value corporate contracts grow from 10% to 22% of mix Keep reserves before taking extra draws

About the author

Henry Walsh

Small Business Educator

Henry Walsh is a small business educator at Financial Models Lab, where he helps aspiring founders make sense of pricing and margin basics, especially in the first months after launch. He focuses on the numbers behind everyday business ideas, from common business costs to realistic profit expectations. His practical approach helps readers compare opportunities clearly and build a stronger plan from the start.

Choosing a selection results in a full page refresh.