You’re weighing resort ownership against the cash it can actually put in your pocket Using the researched five-year model, this 140-room resort produces $234M to $378M in annual revenue and $165M to $284M in operating profit before debt, taxes, and reserves

Owner income$18.7M-$32.4MNet margin70.6%-75.3%Revenue for target pay$26.5M-$43.1MBusiness difficultyHard

Want to test your resort owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on occupancy, ADR, payroll, debt, taxes, and reserve policy.

Want the six resort income drivers?

1

Occupancy

58%-82%

Occupancy rising from 58% to 82% spreads fixed costs across more paid nights, which lifts owner take-home fastest.

2

Rate Mix

$452-$729

Blended ADR runs about $779 to $889 and RevPAR about $452 to $729, so better pricing lifts cash from each filled room.

3

Room Capacity

51.1K nights

With 140 rooms and 51,100 annual room nights, physical capacity sets the ceiling on room revenue and owner income.

4

Ancillary Sales

$275K-$515K

F&B, spa, events, retail, and activity fees add $275K to $515K a year, and most of that drops through to margin.

5

Labor Load

$1.49M-$2.37M

Annual wages rise from $1.49M to $2.37M, so staffing discipline matters if you want EBITDA to reach the owner.

6

Fixed Burden

-$2.77M

The model bottoms at -$2.773M in Month 3, so fixed costs and reserve needs can block cash from reaching the owner.

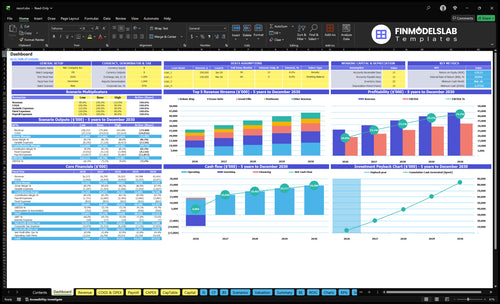

Want to see the Resort income model?

This screenshot in the Resort Financial Model Template is a planning bridge, not a sales pitch: it shows assumptions, occupancy, ADR, RevPAR, ancillary revenue, wages, fixed costs, COGS, variable costs, capex, debt, reserves, scenarios, and owner income. Charts show revenue growth from $234M to $378M and operating profit from $165M to $284M before debt, taxes, and reserves. Open the model.

Owner-income model highlights

Owner take-home output

Revenue and margin charts

Scenario and reserve checks

Which resort costs reduce owner take-home most?

The biggest hit to owner take-home is wages: annual wages rise from $149M to $237M, which dwarfs the $685k monthly overhead stack, so labor is the first place cash gets squeezed. For startup cost context, see How Much Does It Cost To Open, Start, And Launch Your Resort Business? The other take-home drag is debt service and reserves, because they cut cash after operating profit.

Biggest cash drains

Wages: $149M to $237M

Overhead: $685k per month

Utilities: $25k monthly

Insurance: $15k monthly

Landscaping: $10k monthly

Security: $8k monthly

Other cost drags

Travel agent commissions: 30% to 26%

Housekeeping supplies: 15% to 11%

COGS assumptions: 150% to 126%

Debt service cuts owner cash

Reserves also cut owner cash

Admin supplies: $25k monthly

How much profit can a resort owner make?

A Resort owner can make about $165M in Year 1 to $284M in Year 5 in operating profit before debt, taxes, reserves, and reinvestment in the researched model. That assumes 140 rooms, 51,100 annual available room nights, and revenue rising from $234M to $378M; for KPI context, see What Is The Most Important Indicator Of Success For Your Resort?.

Profit Drivers

140 rooms available for sale

51,100 annual room nights

Occupancy and ADR set lodging revenue

Spa, dining, events add upside

Owner Reality

$234M Year 1 revenue

$378M Year 5 revenue

70.5% Year 1 operating margin

Take-home falls after lender payments

How does owner role change resort income?

Owner role changes Resort income because a hands-on owner can replace some management pay, but only if they can truly run the property. In a 140-room Resort, the work is not light: front desk, housekeeping, food and beverage, spa, maintenance, sales, security, and systems all need active oversight. If the model already includes a General Manager at $180k per year, an absentee owner still has to watch performance, capital projects, cash controls, debt capacity, and reserves, so the income is not passive.

Hands-on owner

Can replace some labor cost

Must run daily operations well

Can tighten cash control

Must fund reserves and projects

Hired management

Includes a GM at $180k

Needs owner oversight anyway

Still requires capital spending review

Needs debt and cash checks

Key Takeaways

Occupancy lifts sold nights from 29,638 to 41,902.

ADR rises from $779 to $889, lifting RevPAR.

Ancillary revenue grows from $275k to $515k.

Labor, debt, and capex can erase profit.

Compare low, base, and high resort owner income scenarios

Owner income scenarios

Owner income moves with occupancy, ADR, ancillaries, labor, debt service, and reserves, so the three cases show how much cash stays after the operating load.

A simple view of downside, modeled, and upside cash to owner.

Scenario

Low CaseDownside

Base CaseModeled

High CaseUpside

Launch model

Lower occupancy and slower ADR growth keep owner cash tight.

The modeled run rate supports steady owner income as occupancy and pricing improve.

Stronger occupancy and better direct bookings lift owner income above the base case.

Typical setup

The resort runs below the modeled 58% start, ADR rises slowly, commissions stay higher, and reserves absorb more cash before owner payout.

The resort follows the 140-room plan with 58% to 82% occupancy, steady ADR gains, and growing ancillary income before debt, taxes, and reserves.

The resort fills more rooms, grows spa, F&B, and events, and keeps labor tight enough to protect cash after debt service and reserves.

Cost drivers

Lower occupancy

slower ADR growth

higher commissions

heavier reserves

weaker ancillary spend

Modeled occupancy

steady ADR growth

mix of room types

normal commissions

disciplined labor

Higher occupancy

better direct bookings

stronger ancillary spend

disciplined labor

lower commissions

Owner income rangeBefore owner reserves

$18.7M - $22.2MThin cash

$22.2M - $29.5MMid-cycle cash

$29.5M - $32.4MPeak cash

Best fit

Use this to test a softer opening year or a weak booking market.

Use this for board planning and lender talks around the modeled run rate.

Use this to stress-test upside from strong demand and tight cost control.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Resort Core Six Income Drivers

Occupancy And Seasonality

Occupancy And Seasonality

Occupancy is the share of available room nights you sell, and it drives lodging revenue and cash timing. With 140 rooms, annual capacity is 51,100 room nights; at the model’s 58% to 82% range, sold nights move from about 29,638 to 41,902. That gap is the difference between covering fixed costs and getting squeezed.

Do not treat demand as flat. Peak, shoulder, and low seasons change how much payroll, utilities, and debt service the resort can carry, and weak off-season occupancy can turn a decent year into a cash-tight one.

Track by Season

Measure occupancy by month, day of week, and season, then match staffing to the low-season base. Input room count, open days, seasonal booking pace, and group blocks so the forecast shows when cash lands, not just the annual average.

Use weak months to test packages, minimum-stay rules, and event dates that fill shoulder periods. One extra sold night adds revenue and spreads payroll, housekeeping, and utilities across more rooms.

Room Count And Unit Capacity

Room Count And Unit Capacity

The room mix sets the revenue ceiling. With 140 total rooms and 51,100 annual room nights of capacity, every occupied night has value; every empty night is lost revenue. The mix of 80 Deluxe King, 40 Ocean Suites, 15 Grand Villas, and 5 Penthouses also shapes pricing power, since higher-end units can lift room revenue if demand supports them.

Scale helps absorb fixed costs when occupancy holds, but more keys also add housekeeping, front desk, F&B, maintenance, utilities, furnishings, and capital refresh needs. One point of occupancy equals about 511 room nights a year, so small demand changes can move owner cash fast. If rooms sit empty, the extra capacity becomes cost, not profit.

Track capacity by room type

Measure sold room nights, not just total occupancy. Split results by room type, because the 5 Penthouses and 15 Grand Villas need different rate and service economics than standard rooms. Here’s the quick math: 140 x 365 = 51,100 available room nights, so the owner should watch how many of those nights turn into paid stays and whether the added labor still leaves margin.

Track occupancy by room type.

Track cost per occupied room.

Track housekeeping turns per day.

Track maintenance spend per key.

Use those numbers to test whether growth is earning its keep. If added rooms raise payroll, utilities, or refresh costs faster than room revenue, take-home profit falls even when the property looks bigger. The goal is simple: fill enough keys to spread fixed costs, but keep the cost to serve each occupied room under control.

Ancillary Guest Spend

Ancillary Guest Spend

Ancillary revenue is guest spend beyond rooms: food and beverage, spa services, event bookings, retail, and activity fees. In this model, it rises from $275k to $515k, adding $240k in annual top-line income. That only helps owner pay if the added sales cover the extra labor, supplies, and setup tied to each outlet.

Here’s the quick math: F&B grows from $150k to $270k, spa from $40k to $80k, events from $60k to $120k, retail from $15k to $27k, and activities from $10k to $18k. The risk is mix. Dining, spa, and events can boost revenue but still drag profit if staffing, timing, and waste control are loose.

Protect Add-On Margin

Track each stream on its own: guest count, attach rate (share buying an add-on), average ticket, labor hours, and gross margin. If a dinner package or spa add-on sells well but uses too many staff hours, owner cash falls even when revenue rises. Forecast ancillary sales by outlet before the month starts, then compare actual labor and supply spend to plan.

Use pre-booking, timed service slots, and a tight event calendar to keep labor in line. Retail and activity fees usually carry better margin, so push them through check-in offers and bundles. If dining covers or spa bookings jump without staffing control, overtime and waste can erase the gain fast. Review it weekly, not after month-end.

Labor And Staffing Efficiency

Labor Efficiency

Labor is a margin driver, not a line to slash blindly. In this model, wages rise from $149M in Year 1 to $237M in Year 5, a $88M increase as front desk, housekeeping, food and beverage, and maintenance staff scale with demand.

Key salaries like the $180k General Manager, $120k Head Chef, $90k Spa Director, and $100k Sales & Marketing Manager affect profit and owner draw. If staffing grows faster than sold room nights and ancillary sales, cash flow tightens fast.

Track Labor Per Sold Night

Measure labor against sold room nights, not just headcount. The clean metric is labor cost ÷ occupied room nights, then split it by department so housekeeping, F&B, and front desk can be managed separately. Here’s the quick math: if staffing hours rise before occupancy does, owner income gets squeezed before revenue shows up.

Track overtime by department.

Schedule to seasonal demand.

Cross-train for peak periods.

Set service standards per role.

Review labor weekly, not monthly.

Use staffing plans tied to booking pace and event volume, then test whether service quality holds. If labor cuts lead to slower check-ins, missed housekeeping turns, or weaker dining service, ADR and repeat stays can drop, and the owner loses more than the labor savings.

Debt, Maintenance, And Reserves

Debt, Maintenance, And Reserves

Accounting profit is not the same as owner cash. After operating profit, the resort still pays debt service, maintenance, repairs, renovations, and reserve funding, so a strong profit and loss statement can still produce thin distributions. Fixed property costs are $15k + $25k + $10k = $50k/month.

The model also includes $855M of initial capex across renovation, furnishings, outdoor amenities, kitchen equipment, and spa improvements. If financing is heavy or maintenance is deferred, cash available to owners falls fast. One rule: profit on paper does not fund owner pay unless cash stays after reserves.

Track Cash After Repairs

Track cash available for distributions each month: operating profit minus debt service, maintenance, and reserve funding. Measure reserve spend per occupied room night, plus big-ticket items like room refreshes, kitchen gear, and spa equipment. If the reserve plan is unfunded, future capex hits current cash and cuts owner draws.

Debt service by month

Repair and reserve budget

Capex timing by asset

Fixed property costs

Use a simple test: if fixed property costs are $50k/month before debt, each extra dollar of financing or repair spend comes straight off owner income. Build a rolling 12-month cash forecast and approve repairs early, so deferred maintenance does not create a cash squeeze when occupancy softens.

ADR And RevPAR

ADR and RevPAR

ADR (average daily rate) and RevPAR (revenue per available room) set room revenue, which is the main cash engine here. Using the room mix and midweek/weekend rates, weighted ADR is about $779 in Year 1 and $889 in Year 5. That rate lift increases income without adding rooms, but only if booking pace and reviews support it.

RevPAR blends price and occupancy, so it shows whether the resort is selling the right rooms at the right rate. It rises from about $452 to $729 as occupancy and rates improve. If ADR rises while demand softens, cash flow can stall, so rate changes need to protect occupied nights and owner draw.

Track Rate Power by Room Mix

Measure ADR, RevPAR, room mix, booking pace, and review scores by day type. Test rate moves on midweek versus weekend stays, since the weighted ADR already assumes different rates across those periods. Here’s the quick math: higher rates lift room revenue on every sold night, while RevPAR shows the full effect across all available rooms.

Track midweek and weekend ADR.

Watch booking pace weekly.

Check review scores after changes.

Test room mix by category.

Manage the inputs that support rate power: better amenities, cleaner rooms, faster service, and stronger guest reviews. If booking pace weakens after a rate hike, roll it back fast. What this estimate hides is fee pressure and labor cost, so watch contribution margin, not just top-line room revenue.