Owner income$120k base

Owner income$120k baseHow Much Can a Wholesale Business Owner Make With $120K Pay?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k base  Net margin24.5%

Net margin24.5% Revenue for target pay$490k

Revenue for target pay$490k Business difficultyHard

Business difficultyHard

In the researched model, wholesale business owner income starts with a $120,000 annual founder salary Distribution capacity is limited in Year 1 because EBITDA is -$305k, the model needs $464k minimum cash, and break-even arrives in Month 14 By Year 2, EBITDA reaches $884k, but actual owner take-home still depends on taxes, debt service, inventory buys, receivables, and reinvestment The modeled average order value rises from about $390 in Year 1 to about $1,304 in Year 5

Owner income$120k baseNet margin24.5%Revenue for target pay$490kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full owner-income model?

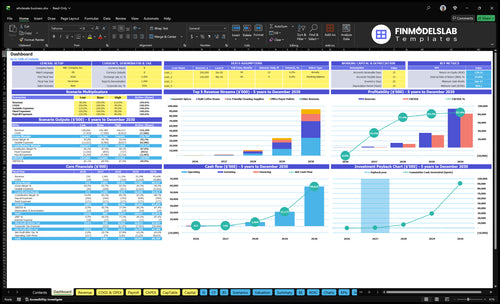

See the Wholesale Business Financial Model Template dashboard for revenue, EBITDA, cash, break-even, payback, and owner pay—open the model.

Owner-income model highlights

- Owner pay outputs included

- Year 1 to Year 2

- Scenario tabs for assumptions

How much revenue does a wholesale business need to pay the owner?

Wholesale Business has no single revenue number for owner pay; it depends on gross margin and how much cost sits below the sale. In Year 1, you already have $14,250 a month in fixed expenses, plus $120,000 founder salary, $265,000 total wages, and $20,000 marketing, all before product COGS. So the sales target has to cover freight, fulfillment, payment fees, warehouse costs, staff, and the $464k cash need.

Cost base

- $14,250 monthly fixed costs

- $171,000 yearly fixed costs

- $120,000 founder salary in Year 1

- $265,000 total wages in Year 1

Revenue drivers

- Higher gross margin lowers needed sales

- Freight can shrink owner pay fast

- Slow receivables tie up cash

- Inventory turns change the answer fast

How do wholesale gross margin and markup affect owner income?

In a Wholesale Business, owner income comes from margin after landed cost, not headline markup; if you want the startup cost side, see How Much Does It Cost To Open A Wholesale Business?. With Year 1 adders at 50% inbound freight and customs, 30% receiving labor, 60% shipping and fulfillment, and 25% payment fees, you’re already at 165% of revenue before product purchase cost, payroll, rent, and marketing. A 1-point margin loss on high-volume sales can wipe owner distributions, and discounts, returns, freight spikes, and supplier price increases hit take-home first.

Margin pressure

- Track landed cost, not markup.

- Inbound freight and customs: 50%.

- Receiving labor: 30%.

- Shipping and fulfillment: 60%.

Owner cash risk

- Payment fees take 25%.

- Total adders reach 165%.

- Discounts cut take-home first.

- Returns and freight spikes hurt fast.

How much can a wholesale business owner make?

A Wholesale Business owner can model $120,000 per year in founder pay from launch, but What Is The Primary Goal Of Your Wholesale Business? matters because distributions depend on cash, not just profit. Year 1 EBITDA (earnings before interest, taxes, depreciation, and amortization) is -$305,000, so take-home beyond salary isn’t supported until reserves recover.

Owner Pay

- Modeled salary: $120,000/year

- Year 1 EBITDA: -$305,000

- No safe Year 1 distributions

- Protect cash before taking profits

Upside Case

- Year 2 EBITDA: $884,000

- Salary already expensed

- Distributions depend on inventory cash

- Cap take-home for reinvestment

What drives wholesale owner income most?

1

84%-89%Gross Margin

Freight, stocking, shipping, and payment fees leave about 84% to 89% before overhead, so this sets owner take-home.

2

$390→$1.3KOrder Volume

Year 1 average order value is $390 and Year 5 reaches $1,304, so bigger orders drive revenue and profit fast.

3

$14.25K/moCost Structure

Fixed overhead runs $14,250 a month, or $171K a year, so every dollar saved here drops straight into owner income.

4

$464KSupplier Terms

The model needs $464K minimum cash at the low point, so better supplier terms reduce working capital pressure and protect distributions.

5

Month 14Customer Terms

Break-even lands in Month 14, so faster customer cash collection helps the business fund itself sooner.

6

50→150Inventory Turns

Units per order rise from 50 to 150, so faster stock movement lifts throughput and keeps cash from sitting on shelves.

Wholesale Business Core Six Income Drivers

Gross Margin And Landed Cost

Gross Margin And Landed Cost

Gross margin is the cash left after landed cost, not just the supplier invoice. In this wholesale model, landed cost includes supplier price plus inbound freight, customs, receiving labor, shrinkage, returns, and discounts, so every margin point hits gross profit before overhead.

The model flags 50% inbound freight and customs and 30% receiving labor as Year 1 adders. If those costs rise, EBITDA, cash reserves, and owner distributions fall even if sales volume holds, because gross profit must still cover $14,250 monthly fixed overhead and $265,000 Year 1 wages.

Track Landed Cost Per SKU

Measure landed cost by SKU and update it when freight, customs, or labor changes. Here’s the quick math: landed cost = supplier price + inbound freight + customs + receiving labor + shrinkage + returns + discounts. Price off gross margin, not markup alone, or owner pay gets squeezed.

Track gross margin dollars, not just margin percent. A sale with a bad discount or a return can lift revenue and still lower cash available for reinvestment and draws. Tight receiving checks and cleaner vendor terms protect the spread that funds overhead and owner income.

- Supplier price per SKU

- Inbound freight and customs

- Receiving labor time and rate

- Shrinkage, returns, discounts

- Gross margin dollars

1

Sales Volume, Order Size, And Repeat Customers

Repeat Orders And Larger Baskets

More active accounts paying for larger repeat orders can move owner income fast. In this model, units per order rise from 50 in Year 1 to 150 in Year 5, while weighted AOV climbs from about $390 to about $1,304. Repeat order frequency also rises from 10 to 17 monthly orders, so revenue can cover fixed costs faster and leave more room for owner pay.

What this estimate hides is capacity risk. If fulfillment slips, returns rise, or margin gets squeezed, higher volume can raise cash pressure instead of profit. The model’s repeat customer share is shown rising from 300% to 750%, so the real test is not just selling more; it’s keeping gross margin intact while order size and order count grow.

Track Order Size And Repeat Rate

Measure units per order, weighted AOV, repeat order frequency, and repeat customer share by month. Here’s the quick math: more orders and bigger baskets lift gross profit dollars, but only if shipping, labor, and error rates stay controlled. If fulfillment cost rises faster than AOV, owner draw gets tighter even when sales grow.

Set a reorder cadence by account, then test bundle pricing and minimum order rules. Use a simple forecast with order count × AOV × gross margin, and compare it to fixed costs before taking cash out. If onboarding takes too long or stockouts hit key accounts, repeat buying slows and the income gain fades.

2

Supplier Pricing, Terms, And Minimum Order Quantity

Supplier Pricing, Terms, and MOQ

Better supplier pricing lowers landed cost, so gross margin rises before overhead. That matters because every saved dollar can flow to profit and owner draw, but only if inbound freight, customs, and receiving cost don’t eat the discount. Track supplier cost per SKU, not just the quote on the purchase order.

Better payment terms reduce cash pressure. A lower minimum order quantity can improve unit cost, but a high MOQ ties cash into stock and can create dead inventory. The best deal is the one that sells through fast enough to protect margin and keep cash free for payroll, freight, and the owner’s take-home pay.

Track margin and cash timing

Build the model around supplier price, inbound freight, customs, payment timing, and reorder levels. That separates a real margin gain from a cash strain. If a discount only works with heavy upfront cash, it can still reduce owner income.

- Measure landed cost per SKU.

- Compare MOQ to sell-through speed.

- Test terms before bigger buys.

When discounts do not create dead stock or shortages, they lift gross profit and support a higher owner draw. If the buy is too large for demand, the margin looks better on paper but cash stays trapped on the shelf.

3

Inventory Turnover And Dead Stock

Inventory Turnover

If inventory turns slowly, cash gets stuck on shelves even when sales and EBITDA look fine. Track turnover days, reorder point, stockout risk, markdowns, shrinkage, and carrying cost. The model’s $464k minimum cash need shows why timing matters for owner pay and restocks.

Here’s the quick math: faster turns release cash, and dead stock traps it. Slow movers raise storage and markdown risk, which cuts gross margin and free cash. That can force emergency buying later and reduce the money left for payroll, inventory, and safer owner distributions.

Track Dead Stock Early

Measure each SKU by age and sales pace, then cut reorder sizes for items that linger. Buy from actual sell-through, not guesswork. If a product needs repeated markdowns or shows shrinkage, it is draining cash and lowering the owner’s take-home income.

Before each purchase, check whether projected cash stays above $464k. If not, slow the order or split it into smaller buys. That protects liquidity, lowers emergency purchases, and makes owner pay safer when demand swings.

4

Warehouse, Freight, Labor, And Fulfillment Costs

Warehouse, Freight, Labor, Fulfillment

This cost stack hits income fast because wholesale needs space, people, systems, and outbound shipping. The fixed base is $14,250 per month for lease, rent, software, cloud, utilities, insurance, accounting, and legal, plus $265,000 in Year 1 wages, or about $22,083 per month. That’s before any variable shipping or picking cost.

Here’s the quick math: if shipping and fulfillment start at 60% of sales, then every $100 sold leaves only $40 before the fixed overhead above. Errors and returns cut that further, so owner pay depends on tight order handling, low damage, and fast, accurate picks.

Track Cost per Order

Measure fulfillment cost as a % of sales, plus labor per order, return rate, and error rate. If order size rises but labor and shipping stay flat per order, margin improves. If returns climb, cash gets stuck in reshipments and write-offs, and the owner’s draw shrinks.

Track these inputs each week: sales, orders, pick lines, freight spend, wages, and returns. A simple control is cost per shipped order. If that number rises while sales are flat, the business is paying more to serve each customer, and that extra cost comes straight out of profit.

5

Receivables, Payment Terms, And Working Capital

Receivables And Payment Terms

Accounts receivable are invoices customers owe but have not paid. In wholesale, net 30 can push cash in by weeks while payroll, rent, freight, and inventory bills still go out, so owner pay can drop even when sales look strong.

The key inputs are receivable days, collection rate, supplier payment timing, and reserve percentage. The model’s $464k minimum cash need shows why timing matters. If cash lands after a big restock, distributions should stay tight until the cycle clears.

Shorten The Cash Gap

Track how long invoices stay open, then compare that to when suppliers, freight, and payroll are due. If collections lag restocking, cash gets trapped and owner draw gets risky. One clean rule: collect before you buy the next big batch.

- Review aging every week.

- Flag slow payers fast.

- Match terms to cash cycle.

- Hold a cash reserve.

Use a simple forecast that shows money in, money out, and the gap between them. If collection rate falls or supplier payment timing tightens, lower draws first. That protects payroll, keeps stock moving, and avoids forced borrowing.

6

Compare low, base, and high wholesale owner income cases

Owner income scenarios

Owner income swings with volume, wage load, and cash tied up in inventory and receivables. Year 1 is cash-stressed, Year 2 turns positive, and later years only work if reserves hold.

| Scenario | Low CaseDownside case | Base CaseModeled case | High CaseExpansion case |

|---|---|---|---|

| Launch model | This is the stressed launch case where the founder is paid, but there is no safe distribution. | This is the modeled operating case where the business clears EBITDA and can support owner pay after reserves. | This is the expansion-stage upside case, not a forecast, where later-year scale lifts owner income. |

| Typical setup | Year 1 carries $20k marketing, about $265k wages, and -$305k EBITDA, while cash is still trapped in stock and receivables. | Year 2 shows $884k EBITDA, $50k marketing, $90 CAC, and 45% repeat customers, but stock and receivables still need working capital. | Later-year scale lifts EBITDA to $81.852M as repeat customers reach 75%, lifetime extends to 36 months, and orders per repeat customer hit 1.7. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $120k salary onlyNo safe draw | $120k salary plus upsideReserve-backed pay | $120k+ expansion upsideExpansion-stage upside |

| Best fit | Use this to test survival if sales start slowly or collections slip. | Use this as the planning base if collections stay tight and working capital is funded. | Use this only to test upside if the model scales and cash conversion stays strong. |

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; taxes, debt service, inventory swings, and receivable timing can change owner take-home fast.

Related Products

- Wholesale Business Porter's Five Forces Analysis

- Wholesale Business BCG Matrix

- Wholesale Business Business Model Canvas

- Critical KPIs to Measure Your Wholesale Business Growth

- Wholesale Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Wholesale Business Profitability and Efficiency

- How Much Does It Cost To Run A Wholesale Business Monthly?

- Wholesale Business Startup Costs: $190K CAPEX Plus Cash Runway

- Wholesale Business Financial Model Template in Excel

- How to Start a Wholesale Business and Be Order-Ready by Month 1

- How to Write a Wholesale Business Plan: 7 Steps to Financial Clarity

- Wholesale Business Marketing Mix

- Wholesale Business Marketing Plan

- Wholesale Business Business Proposal

- Wholesale Business PESTEL Analysis

- Wholesale Business Pitch Deck Example Editable PPTX

- Wholesale Business Business SWOT Analysis

- Wholesale Business Value Proposition Canvas

Frequently Asked Questions

In this model, the founder salary is $120,000 per year Year 1 EBITDA is -$305k, so extra draws are not supported before reserves Year 2 EBITDA reaches $884k, but distributions still depend on taxes, debt service, inventory buys, receivables, and the $464k minimum cash need