Can a personal training studio owner income scale?

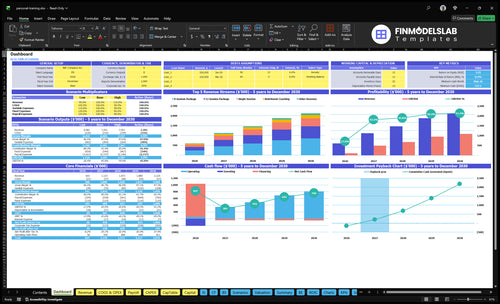

Yes—Personal Training owner income can scale past solo hourly capacity, but only if utilization, retention, pricing, and staffing move together. In the model, volume rises from 25 visits per day to 60 visits per day over five years, while EBITDA grows from $102K to $1,089M as the team expands. Group training, add-on coaching, and retail can lift revenue per hour, but payroll, churn, rent, and fixed-cost risk can eat the gain.

Growth drivers

25 to 60 visits daily

2 trainers to 6 trainers

Manager, lead trainer, front desk

Add coaching and retail sales

Risk points

Payroll can outpace sales

Churn can slow repeat visits

Rent can crush margins

Fixed costs can absorb gains

How many personal training clients to make $100K?

For Personal Training, the quick math says 7,500 annual visits at 25 visits/day over 300 operating days equals about 144 paid visits/week. Client count depends on how many sessions each client buys per week, so divide weekly sessions needed by average sessions per client per week. Also, $100K owner pay is not the same as $100K EBITDA, because taxes, debt, reserves, and reinvestment still come out of cash.

Visit math

25 visits/day × 300 days = 7,500

7,500 ÷ 52 weeks ≈ 144 visits/week

Clients = weekly sessions needed ÷ sessions per client

Package price changes client count fast

Cash reality

Model reaches $102K Year 1 EBITDA

$100K EBITDA is not $100K pay

Reserves reduce cash available to owner

Taxes and debt service cut take-home

How much can a solo personal trainer make?

A solo Personal Training owner can gross about $98,800/year before costs at 20 paid sessions/week and $148,200/year before costs at 30 paid sessions/week, using the $95 8-session package rate. That’s revenue, not take-home pay, so track paid sessions, cancellations, and client growth with What Is The Most Important Indicator Of Growth For Your Personal Training Business?.

Solo math

20 sessions/week × $95 × 52 = $98,800

30 sessions/week × $95 × 52 = $148,200

$90 rate applies to 12-session packages

$125 applies to single sessions

Real caps

Limit comes from paid weekly sessions

Cancellations cut billable hours fast

Admin and programming time are unpaid

Travel reduces sellable training slots

Personal Training Financial Model

5-Year Financial Projections

100% Editable

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Accounting Or Financial Knowledge

Want the six income drivers?

1

Billable Capacity

25-60/day

More booked sessions spread the $9.15K monthly fixed load, so utilization moves owner cash fastest.

2

Pricing Mix

$90-$135

Higher package and session pricing lifts revenue per visit, and that drops straight to owner take-home after fixed costs.

3

Payroll Load

2-6 FTE

Trainer headcount climbs from 2 to 6 FTE, so payroll can swallow the gain if sales lag.

4

Client Retention

30%-40%

A bigger 12-session mix means clients stay prepaid longer, which steadies cash and trims churn risk.

5

Add-On Sales

10%-18%

More add-on coaching and assessment sales raise average spend without needing as many extra visits.

6

Marketing Cost

4%-3%

Client acquisition marketing falls from 4.0% to 3.0% of revenue, so each sale leaves more margin.

Personal Training Core Six Income Drivers

Billable Session Capacity

Billable Session Capacity

Paid sessions are the revenue engine here. Moving from 25 average visits/day in Year 1 to 60 in Year 5 lifts annual paid sessions from 7,500 to 18,600. That only helps owner income if those are billable training slots, not consults, admin, travel, cleaning, programming, or no-shows. More empty slots means rent and payroll stay fixed while profit drops.

One line: fill more booked hours, or EBITDA slips fast. The key test is whether the trainer calendar is full enough to cover fixed overhead and still leave room for owner pay. If cancellations rise or trainer burnout shows up, the business can look busy but still fail to turn sessions into cash.

Improve Booked-Session Rate

Track paid sessions, not just appointments. Measure booked-session rate, cancellation rate, and no-show rate by trainer and by week. Compare scheduled slots to completed paid visits so you can see where revenue leaks. A calendar that looks full but has weak attendance still leaves payroll and rent at the same level, so it does not protect owner take-home.

One line: every empty slot should be visible the same day. Use forecasting to match staffing to demand, then cap burnout before service quality falls. If cancellations or trainer fatigue climb, the business loses both revenue and repeat clients, which weakens EBITDA, or operating cash profit, even when headline traffic looks strong.

1

Pricing And Package Mix

Pricing And Package Mix

This driver is the blended revenue per paid visit. Year 1 pricing is $95 for an 8-session package, $90 for a 12-session package, $125 for a single session, $75 for nutritional coaching, $60 for a specialized assessment, and $7 retail per visit. By Year 5, those move to $105, $100, $135, $85, $70, and $10.

The mix matters as much as the price. If 12-session packages rise from 30% to 40% and single sessions fall from 15% to 7%, cash flow gets steadier, but the average ticket can get pulled down if the discount is too deep. Higher blended pricing lifts the cash left for owner pay after fixed overhead.

Track Blended Ticket, Not Just List Price

Use average revenue per paid visit as the control metric. Here’s the quick math: session price + coaching attach rate + assessment sales + retail per visit. Track it by trainer, package type, and month, so you can see whether more renewals are really creating more cash or just more low-price visits.

Watch blended revenue per paid visit.

Split singles, 8s, and 12s.

Track add-on attach rate.

Measure retail dollars per visit.

Test discounts against renewal rate.

The risk is simple: discounting can improve retention, but if singles fall fast and package discounts deepen, take-home income drops even when visit count holds. What this estimate hides is mix quality, so price changes should be tested against renewal, not just lead volume.

2

Client Retention And Recurring Revenue

Client Retention And Recurring Revenue

Client retention lifts owner income because repeat packages turn training into steadier cash flow. When the mix shifts from 40% 8-session and 30% 12-session packages in Year 1 to 30% and 40% in Year 5, more revenue comes from longer commitments, so fewer new leads are needed to keep the schedule full.

Here’s the quick math: prepaid or committed sessions help cover $9,150 in monthly fixed overhead before the month ends, which lowers stress on payroll and rent. If cancellations or non-renewals rise, the owner has to spend more on marketing to refill the pipeline, and take-home pay gets squeezed fast.

Track Renewal Rate And Package Length

Measure renewal rate, package mix, and prepaid session volume each month. Track how many clients renew after an 8-session or 12-session block, because that tells you how much revenue is truly recurring and how much depends on fresh sales.

Also watch cancellations, non-renewals, and marketing spend per booked client. If longer packages grow but close rates fall, the cash benefit can disappear. A simple target is to keep more revenue tied to committed sessions so owner pay is less exposed to weak lead flow.

Track renewal after each package

Watch prepaid sessions by month

Compare churn to marketing spend

Protect cash before payroll hits

3

Service Model And Leverage

Service Model Leverage

One-on-one training is simple, but it caps income because each paid session uses one trainer hour. Semi-private and group formats can raise revenue per hour, and online add-ons can add sales without the same room-time limit. In the source model, add-on services rise from 10% to 18% of mix, while retail stays at 5%.

The catch is cost. More formats add scheduling, quality control, and churn risk, so the owner only wins if extra revenue covers payroll, software, and management time. One clean rule: if the new format does not lift margin faster than it adds overhead, owner take-home gets worse, not better.

Measure Revenue per Trainer Hour

Track each format separately: one-on-one, semi-private, group, and online add-ons. Measure booked hours, revenue per trainer hour, no-show rate, and renewal rate. If group sessions fill dead time but push churn higher, the gain can disappear fast. The goal is simple: keep service quality high while lifting hourly yield.

Watch add-on attach rate monthly.

Compare margin by format.

Cut low-yield time slots.

Limit formats you cannot staff.

4

Client Acquisition Efficiency

Client Acquisition Efficiency

For personal training, this driver is the share of revenue spent to win new clients. The model assumes marketing runs at 40% of revenue in Year 1, then improves to 30% by Year 5. That matters because marketing is paid before owner pay, so every point you save here lifts cash available for payroll, debt service, and the owner draw.

The real inputs are leads, trial sessions, consult close rate, package mix, and retention. Vanity leads do not help if they do not buy packages. Paid ads can fill calendars, but if close rates or renewals stay weak, the extra spend can cut EBITDA margin instead of growing it.

Track Close Rate, Not Just Lead Volume

Use a simple funnel: lead, trial, consult, package sale, renewal. If revenue is $100,000, Year 1 marketing is about $40,000; at Year 5, it falls to $30,000. Here’s the quick math: lower marketing as a share of sales means more gross profit stays in the business, so owner income improves even if total revenue grows slowly.

Track cost per booked consult.

Track consult-to-package close rate.

Track renewal rate by package.

Cut channels that do not sell.

Favor referrals and local search.

Best channels here are referrals, local partnerships, local search, social media, trial sessions, and consult conversion. If acquisition costs rise faster than close rates, marketing eats the owner’s take-home. If the funnel tightens, the same revenue base can support a stronger EBITDA margin and steadier cash flow.

5

Overhead And Staffing Structure

Overhead and Staffing Load

Overhead and staffing set the floor on owner pay here. The model carries $9,150/month in fixed costs plus $285K in Year 1 payroll before owner distributions, so rent and labor must stay tightly matched to booked sessions. If utilization slips, profit gets squeezed fast even when revenue looks healthy.

By Year 5, staffing expands to six personal trainers plus a manager, lead trainer, front desk, and marketing coordinator. The inputs that matter are booked sessions, trainer hours, payroll, and fixed occupancy cost. One clean rule: if payroll rises faster than paid session volume, owner take-home falls.

Track Payroll Against Booked Sessions

Measure payroll per booked session, not just total payroll. Split fixed costs from labor, then compare both to paid hours, cancellations, and no-shows. The goal is simple: every added staff role should lift utilization enough to pay for itself, not just add coverage.

Use a staffing plan tied to demand. Keep trainer count, front-desk coverage, and management hours aligned with booked volume. If sessions lag, slow hiring or trim nonessential hours first. That protects cash flow because the biggest drain here is fixed or semi-fixed cost, not variable supply.

$9,150 fixed cost floor

$285K Year 1 payroll

6 trainers by Year 5

Watch cancellations and no-shows

6

Personal Training Business Plan

30+ Business Plan Pages

Investor/Bank Ready

Pre-Written Business Plan

Customizable in Minutes

Immediate Access

Personal training income scenario objective

Owner income scenarios

Owner income swings with visit volume, package mix, and payroll. Year 1 is the ramp case, Year 3 is the base case, and Year 5 is the mature case.

Compare low, base, and high owner income cases for a personal training studio.

Scenario

Low CaseRamp case

Base CaseBase case

High CaseUpside case

Launch model

This is the lean ramp case: 25 visits a day, 300 operating days, Month 5 breakeven, about $102k EBITDA, and roughly $727k minimum cash need.

This is the modeled middle case: 45 visits a day, 305 operating days, and about $671k EBITDA in Year 3.

This is the stronger Year 5 case: 60 visits a day, 310 operating days, six personal trainers, and about $1.089M EBITDA.

Typical setup

Modeled revenue proxy is about $706.9k, EBITDA margin is about 14%, fixed costs are $109.8k a year, and payroll is about $285k with 2 trainers, a manager, a lead trainer, and front desk support.

Modeled revenue proxy is about $1.32M, EBITDA margin is about 51%, fixed costs stay at $109.8k, and payroll is about $457.5k with 4 trainers, 1.5 front desk FTE, and a marketing coordinator.

Modeled revenue proxy is about $1.86M, EBITDA margin is about 59%, fixed costs stay at $109.8k, and payroll is about $585k with 6 trainers, 2 front desk staff, and a full-time marketing coordinator.

Cost drivers

25 visits/day

300 operating days

2 trainers

$109.8k fixed costs

Month 5 breakeven

45 visits/day

305 operating days

4 trainers

1.5 front desk FTE

$671k EBITDA

60 visits/day

310 operating days

6 trainers

40% 12-session mix

$1.089M EBITDA

Owner income rangeBefore owner reserves

About $102k EBITDARamp income

About $671k EBITDABase income

About $1.089M EBITDAUpside income

Best fit

Use this to stress-test the launch period if bookings are slow or fill takes longer than planned.

Use this as the planning case for a steady studio with growing repeat demand and a larger staff.

Use this to test a mature studio with fuller capacity, stronger add-on sales, and a bigger payroll load.

!

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

The source model is driven by visits, not active-client count It starts at 25 visits per day for 300 days, then reaches 60 visits per day for 310 days by Year 5 Prices range from $90 to $125 in Year 1 and $100 to $135 by Year 5 for the main training offers

This model reaches breakeven in Month 5 and has an 18-month payback period That assumes the owner funds a staffed studio with $213K of listed startup capex and enough cash to cover the $727K minimum cash need A lean solo setup would have a different breakeven path

You need trainers only if you want to move beyond the owner’s billable-hour cap This model hires two personal trainers in Year 1 and grows to six by Year 5 That supports higher volume, from 25 to 60 visits per day, but payroll also rises, so utilization must stay strong

The biggest factors are booked sessions, package pricing, renewals, payroll, rent, and marketing efficiency In this model, fixed overhead is $9,150 per month, Year 1 payroll is $285K, and client acquisition marketing starts at 40% of revenue Owner take-home falls if those costs rise faster than paid visits

The best model is the one that fills paid capacity without adding too much fixed cost One-on-one training is simple but capped by hours A staffed studio can scale to $1089M Year 5 EBITDA in this model, but it needs strong utilization, 60 visits per day, and disciplined payroll management

About the author

Ava Mitchell

Business Plan Writer

Ava Mitchell is a business plan writer at Financial Models Lab who helps early-stage founders choose realistic business ideas with founder-friendly numbers. She explains startup planning in plain English, with a focus on operating expense planning and on breaking down revenue, expenses, and profit so founders can make practical real-world decisions.

Choosing a selection results in a full page refresh.