Owner income$120k to $6.4M

Owner income$120k to $6.4MHow Much TV Advertising Agency Owners Make: $120K–$645M

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k to $6.4M  Net margin-4% to 75%

Net margin-4% to 75% Revenue for target pay$1.38M

Revenue for target pay$1.38M Business difficultyHard

Business difficultyHard

You’re trying to separate agency revenue from what the owner can actually take home In this five-year planning model, the owner salary is $120,000 per year, while EBITDA moves from -$22,000 in Year 1 to $6326 million in Year 5 before taxes, debt service, reserves, or distributions

Owner income$120k to $6.4MNet margin-4% to 75%Revenue for target pay$1.38MBusiness difficultyHardWant to test your owner pay scenario?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment.

Want to check owner income in the TV Advertising Agency model?

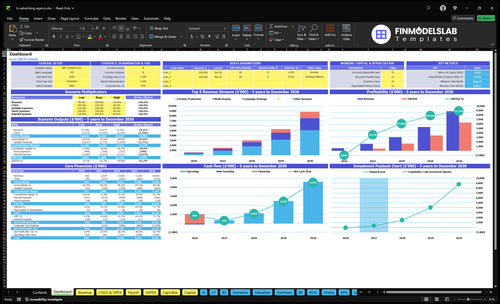

The TV Advertising Agency Financial Model Template dashboard shows revenue streams, EBITDA, cash, payback, breakeven, and owner income; assumptions and scenarios built in. Open it now.

Owner-income model highlights

- Owner income output included

- Mix, hours, rates, costs

- Payroll, overhead, marketing, capex

- Lean, base, high cases

- Month 8 breakeven

- $820k minimum cash need

- 19-month payback

- EBITDA: -$22k to $6.326M

How much revenue does a TV advertising agency need to pay the owner?

If the TV Advertising Agency pays the owner $120,000, Year 1 payroll is $310,000 and fixed overhead is $78,000, so it needs about $413,000 of Year 1 payroll, overhead, and marketing covered before profit. With a 290% variable and direct cost load, that means roughly $582,000 of revenue, and the model hits breakeven in Month 8.

Cost base

- $120,000 owner salary

- $310,000 Year 1 payroll

- $78,000 fixed overhead

- $413,000 cost coverage need

Revenue target

- 290% direct cost load

- About $0.71 left per $100

- Needs about $582,000 revenue

- Breakeven lands in Month 8

Can a small TV advertising agency owner make good money?

Yes — a small TV Advertising Agency can make good money, but only if it keeps staffing tight and lands recurring clients. The model is not ultra-lean: $6,500 in monthly fixed overhead, $310,000 in Year 1 payroll, and $81,000 in launch capex still leave Year 1 EBITDA at -$22,000 even with a $120,000 owner salary. Profitability improves sharply after Month 8, so pricing strategy and production well matters more than adding headcount early.

Money math

- $6,500 monthly fixed overhead

- $310,000 Year 1 payroll

- $81,000 launch capex

- Year 1 EBITDA: -$22,000

What makes it work

- Keep staffing tight early

- Retain recurring clients

- Price strategy and production well

- Avoid overstaffing before repeat work

TV advertising agency profit margin

Your TV Advertising Agency margin comes from retained fees, not from the size of station spend. If you want the startup cost side, see What Is The Estimated Cost To Open And Launch Your TV Advertising Agency?—because high media billings can look big while owner income stays thin.

Creative margin

- Year 1 production cost: 120% of revenue

- Year 5 production cost: 80% of revenue

- Direct costs shrink as process tightens

- Margin improves only if fees rise

Media buy margin

- Software and data: 50% to 30%

- Freelance support: 70% to 40%

- Project tools: 50% to 25%

- Station spend is passed through

Want the six drivers that move owner income most?

1

$6.3MManaged Spend

Bigger billed media spend plus commission, markup, and retainers drive the fastest jump in owner take-home as the model scales.

2

$507KClient Retention

Keeping accounts longer lifts repeat fees and helps move from Year 1 EBITDA of -$22K to Year 2 EBITDA of $507K.

3

80%-95%Production Margin

Creative production stays mostly billable at 80% to 95%, so wasted revision time cuts profit fast.

4

70%-90%Media Buying

Media buying work runs at 70% to 90% allocation, so tighter routing and fewer handoffs protect margin.

5

$310K-$585KPayroll Load

Payroll grows from about $310K in Year 1 to $585K in Year 5, so staffing mistakes quickly cut cash left for the owner.

6

$78K/yrOwner Load

Fixed overhead is about $78K a year, but if the founder stays the bottleneck, revenue growth stalls.

TV Advertising Agency Core Six Income Drivers

TV media spend under management

Managed TV Media Spend

When you manage more TV spend, agency revenue can rise through commissions, markups, planning fees, or buying fees. The key inputs are managed gross spend, the fee model, and billable media buying hours. In the model, media buying rate starts at $150 and rises to $170 by Year 5, while billable hours rise from 250 to 350.

The trap is simple: gross TV billings are not revenue if station spend just passes through. Higher spend only helps owner income when fee capture is clear. If the agency sells strategy plus placement, more managed spend can lift profit and cash flow; if it only passes media dollars through, the extra volume adds work without much margin.

Track Fee Capture, Not Just Spend

Measure managed spend, effective fee rate, and billable hours on every account. A simple test is: how much fee revenue do you keep per $1 of TV spend, and how many hours did the team spend to earn it? That tells you whether growth is adding income or just adding traffic through the books.

- Separate pass-through spend from fee revenue

- Price planning and buying separately

- Watch hours per account monthly

- Raise rates as buying complexity grows

If spend is up but fees are flat, owner pay will usually stall. The fix is tighter scope and cleaner pricing: define what the agency earns on planning, placement, and buying before the media dollars start moving.

1

TV advertising agency commission rate and retainer pricing

Commission and Retainer Pricing

Commission-only pricing ties owner income to media volume, so cash rises and falls with TV spend. A hybrid model that blends planning, placement, and project fees usually keeps more revenue in-house and makes owner pay steadier. If the agency only passes station spend through, gross billings are not real revenue.

Here’s the quick math: campaign strategy pricing starts at $200 and rises to $220, while strategy adoption moves from 400% to 700% in the model. That helps because clients pay for planning, not just airtime. Retainers smooth cash flow, and one-off project fees fit launch campaigns or short TV tests.

Price Planning, Not Just Placement

Track media spend under management, strategy fees collected, and retained clients on monthly plans. Use separate pricing for strategy, media buying, and creative work, then test where clients accept a retainer plus project fee instead of a pure commission. If buying control is weak, keep markups tight and don’t count pass-through spend as revenue.

- Track retained revenue by client.

- Split planning from placement fees.

- Measure renewal rate each quarter.

- Watch cash gaps before payroll.

Owner income improves when recurring fees cover fixed costs and reduce the need to chase new TV budgets every month. If clients only buy placement, pricing power stays thin; if they buy strategy too, the agency can raise fees without waiting for larger media volume. That’s what turns a busy book into usable profit.

2

TV commercial production margin

TV Commercial Production Margin

Production margin is the spread between what the client pays for scripting, creative direction, filming, editing, audio, voiceover, and finished spot delivery and what the shoot actually costs. Here’s the quick math: at a $175 creative production rate, direct costs at 120% of revenue mean a -20% gross margin; at 80%, margin turns to 20%. That swing is what decides whether owner pay gets funded or gets squeezed.

The danger is vendor-heavy work. If talent, equipment, and locations are not tightly scoped, the job can lose money even when adoption rises from 800% to 950% and the rate moves to $195. More volume does not fix bad unit economics. The owner’s take-home improves only when revisions are limited and every shoot is priced to cover labor, vendors, and rework.

Control the shoot economics

Track three things on every job: fee, direct cost, and revision count. A simple formula works: gross profit equals production revenue minus talent, crew, gear, and location costs. If direct costs are above 80% of revenue, the owner is barely earning anything after overhead. If they hit 120%, the job is destroying cash.

Price for scope, not hope. Lock the brief, cap revisions, and pre-approve vendor spend before filming starts. Use separate line items for talent, equipment, and locations so a one-day shoot does not turn into an unplanned margin leak. That discipline protects gross margin and makes owner draws more predictable.

3

TV advertising agency client retention

Client retention

Recurring TV advertising clients cut sales pressure and steady cash flow. In the model, customer acquisition cost drops from $2,500 in Year 1 to $1,500 in Year 5, a 40% drop. That matters because every lost account has to be replaced with cash, time, and staff effort before profit reaches the owner.

Retention ties directly to take-home pay. If renewal rates slip, more of the $25,000 to $110,000 marketing budget gets spent chasing new logos instead of serving current clients. One line says it all: kept clients pay twice — once in revenue now, and again by lowering future selling cost.

Renew on results, not on habit

Track renewal by campaign results, media performance, and production refresh needs. Tie review dates to the end of a flight, a rating or response readout, and the point when the spot needs a new cut. That gives you a clean reason to keep the client active and reduces surprise churn.

- Measure repeat client rate monthly

- Track CAC by client cohort

- Log churn reasons in writing

- Flag refresh dates before expiry

Recurring revenue is useful, but not guaranteed. If onboarding takes too long or results are weak, clients will leave and the owner pays for it in re-selling time and weaker cash flow.

4

TV advertising agency staffing costs and freelancer utilization

Staffing Mix and Freelancer Load

When TV agency work moves from the owner to employees or freelancers, owner pay changes fast. Payroll climbs from $310,000 in Year 1 to $445,000 in Year 2, then $530,000 in Years 3 and 4, and $585,000 in Year 5. Early lean economics can lift take-home, but they also cap capacity.

Freelance support starts at 70% of revenue and falls to 40%. That mix drives gross margin, cash flow, and the owner’s draw. If staffing grows faster than billable work, breakeven rises and the business needs more retained revenue just to keep owner income steady.

Track Labor Against Billable Work

Measure payroll, freelance spend, and billable hours together. The key inputs are revenue, the share of work done by staff versus freelancers, and the amount of production or media buying work each person can sell. Here’s the clean test: if labor cost grows while revenue quality stays flat, owner pay gets squeezed.

Set a monthly labor plan by client and by role. Keep freelancer use flexible for peak shoots and campaign launches, and move fixed payroll only when repeat work can cover it. Watch for one warning sign: if payroll is already at $445,000 in Year 2 but revenue is still choppy, cash gets tight fast.

5

TV advertising agency overhead and cash reserves

Agency Overhead and Cash Reserves

Fixed overhead is $6,500 per month before any production labor or media spend. That means EBITDA can look healthy, but distributable cash still gets squeezed by rent, software, insurance, legal, and hosting. The owner’s take-home depends on whether collections arrive on time and whether cash stays inside the business for slow client payments, disputes, and overruns.

By Month 8, the model shows a minimum cash need of $820,000. Here’s the quick math: cash reserves have to cover fixed burn plus working capital timing gaps. If the owner pulls cash out too early, the business can’t absorb a delayed payment or a project overrun without cutting pay or delaying vendors.

Track burn, not just EBITDA

Measure fixed overhead, days sales outstanding, and reserve months every month. The key inputs are rent, utilities and internet, software, insurance, accounting and legal, supplies, hosting, and the timing of client collections. If overhead stays at $6,500/month, the real question is whether cash cover is enough to keep owner draws safe.

- Track cash by project.

- Separate pass-through media spend.

- Hold back on owner draws.

- Flag disputed invoices fast.

- Refresh the reserve forecast monthly.

Owner role matters too: if the owner is still signing deals, managing production, and covering client fire drills, cash tends to stay in the company longer. If the business relies on the owner for approvals or sales, keep a tighter reserve because collections and delivery delays can hit the same month.

6

Compare lean, base, and high TV advertising agency owner income scenarios

Owner income scenarios

Owner income is tight in launch year, improves in the modeled base year, and has the most room in the mature year as EBITDA rises and the cost load falls.

| Scenario | Low CaseLaunch risk | Base CaseScaling | High CaseMature profit |

|---|---|---|---|

| Launch model | This is the launch-risk case, with income held to salary while the agency absorbs early losses. | This is the modeled case, with EBITDA turning positive and some room for owner distributions after reserves. | This is the stronger earnings path, with mature-year profit supporting larger owner payouts after reserves. |

| Typical setup | Year 1 carries a $120,000 owner salary, -$22,000 EBITDA, about $310,000 payroll, $78,000 fixed overhead, and a 290% variable and direct cost load, so there is no clean distribution base case. | Year 2 shows $507,000 EBITDA, about $445,000 payroll, and a 255% cost load, so the owner keeps salary intact and can start small distributions after reserves. | Year 5 reaches $6.326 million EBITDA, about $585,000 payroll, and a 175% cost load, so the owner has the most room for distributions after reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $120,000 salary onlySalary only | Salary plus limited distributionLimited draw | Salary plus larger distributionLarger draw |

| Best fit | Use this to stress-test launch cash and whether the owner can live on salary alone. | Use this as the planning case for a growing agency that can pay the owner and still build cash. | Use this to test mature-year upside, reserve policy, and safe payout capacity. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution outcomes.

Related Products

- TV Advertising Agency Porter's Five Forces Analysis

- TV Advertising Agency BCG Matrix

- TV Advertising Agency Business Model Canvas

- 7 Critical KPIs for a TV Advertising Agency

- TV Advertising Agency Business Plan Template in Pre-Written Word

- 7 Strategies to Increase TV Advertising Agency Profitability

- Running Costs for a TV Advertising Agency: Monthly Budget Breakdown

- TV Advertising Agency Startup Costs: $81K CAPEX And $820K Funding

- TV Advertising Agency Financial Model Template in Excel

- How To Start A TV Advertising Agency In 8 To 16 Weeks

- How to Write a TV Advertising Agency Business Plan in 7 Steps

- TV Advertising Agency Marketing Mix

- TV Advertising Agency Marketing Plan

- TV Advertising Agency Business Proposal

- TV Advertising Agency PESTEL Analysis

- TV Advertising Agency Pitch Deck Example Editable PPTX

- TV Advertising Agency Business SWOT Analysis

- TV Advertising Agency Value Proposition Canvas

Frequently Asked Questions

Not all profit becomes owner income The model includes a $120,000 owner salary, then shows EBITDA of -$22,000 in Year 1 and $507,000 in Year 2 Distributions should come only after taxes, reserves, debt service, and reinvestment are covered